ディスプレイ包装の市場機会、成長促進要因、産業動向分析、2025~2034年予測

Display Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日

- 商品コード

- 1755258

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

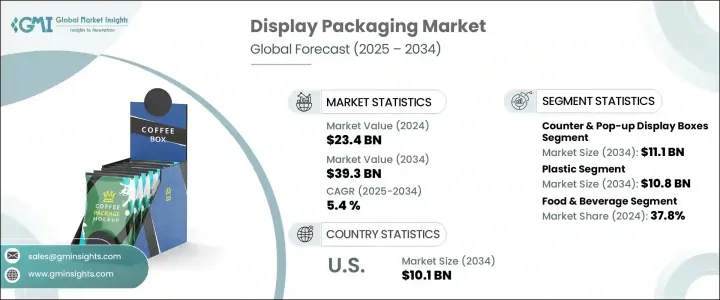

世界のディスプレイ包装市場は、2024年には234億米ドルとなり、CAGR 5.4%で成長し、2034年には393億米ドルに達すると推定されています。

eコマースの急速な成長により、製品の視認性を高め、消費者の関与を促す視覚に訴える包装が引き続き求められています。オンライン購入を選択する買い物客が増えるにつれ、創造的でブランド化されたディスプレイ包装の魅力が重要な販売促進要因となっています。ソーシャルメディアの動向、特にアンボックスコンテンツは、美的包装の重要性を高めています。

しかし、世界の貿易摩擦や関税、特にトランプ政権下で始まった関税は、板紙やプラスチックなどの原料のコストを上昇させ、サプライチェーンを混乱させています。こうした混乱は生産の遅れにつながり、メーカーやサプライヤーに影響を及ぼしています。カスタマイズは、ブランドの差別化と消費者との感情的な結びつきを助けるため、ディスプレイ包装の成功の中心であり続けています。市場の進化は持続可能性と密接に結びついており、リサイクル可能な材料やエコフレンドリーデザインへの関心が高まっています。企業がよりエコフレンドリーソリューションへとシフトする中、消費者の嗜好の変化や環境規制への対応として、ディスプレイ包装のイノベーションが生まれ続けています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 234億米ドル |

| 予測金額 | 393億米ドル |

| CAGR | 5.4% |

ディスプレイ包装産業は、製品のプレゼンテーションを強化し、消費者の関心を高めるようにデザインされたフォーマットを網羅しています。これには、エンドキャップディスプレイ、パレットディスプレイ、透明包装、フロアスタンドディスプレイ、カウンター&ポップアップディスプレイボックスなどが含まれます。カウンター&ポップアップディスプレイボックスセグメントは、2034年までに111億米ドルに達すると予測されており、最もインパクトがあり商業的に成功したフォーマットの1つとして浮上しています。これらのディスプレイは、視覚的な魅力と機能的な汎用性を併せ持つことが原動力となっています。ブランドは、鮮やかなグラフィック、独創的な形態、戦略的な配置が購入の意思決定に大きな影響を与える、これらのユニットを店頭で好んで使用しています。

材料の用途別では、プラスチックセグメントが依然として産業をリードする選択肢であり、2034年までに108億米ドルの市場規模を達成すると予想されています。透明包装への嗜好の高まりが、この成長の要因となっています。この透明性は信頼を築き、棚へのアピールを高めています。同時に、産業はよりエコフレンドリープラスチック代替品への移行を進めています。各ブランドは、環境基準の強化やサステイナブル包装を求める消費者の要望に応えるため、リサイクル可能なプラスチックや生分解性プラスチックを採用しています。

ドイツのディスプレイ包装2034年のCAGRは4.9%と予測されます。ドイツのエンジニアリングと製造業における深い専門知識は、包装ソリューション、特に軽量でありながら耐久性のある段ボール材料の技術革新に拍車をかけています。ドイツ企業は、過剰な床面積を占めることなく最大限の視認性を実現するコンパクトな陳列デザインに注力しています。オートメーションとデジタル印刷技術を統合することで、迅速なカスタマイズと拡大可能な生産が可能になり、欧州の情勢におけるリーダーとしてのドイツの地位はさらに強固なものとなっています。

競合情勢を形成している主要企業は、Smurfit Kappa、Mondi Group、DS Smith、International Paper、WestRock Companyなどです。市場での存在感を確固たるものにするため、主要企業は技術革新、戦略的パートナーシップ、持続可能性に焦点を当てた戦略を実施しています。これらの企業は、世界の環境基準に沿ったエコフレンドリー包装ソリューションを開発するために研究開発に投資しています。小売業者やブランドオーナーとのコラボレーションにより、進化する消費者の嗜好に合わせたデザインが可能になります。各社はまた、買収や施設のアップグレードを通じて世界のフットプリントを拡大し、生産効率と地理的リーチを強化しています。スマート包装や自動化された生産ラインなどのデジタル技術の導入も、変化の激しい小売産業において、拡大性と対応力を高めるための中核的な動きです。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 産業考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 産業への影響

- 供給側の影響(原料)

- 価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原料)

- 影響を受ける主要企業

- 戦略的な産業対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 施策関与

- 展望と今後の検討事項

- 貿易への影響

- 産業への影響要因

- 促進要因

- eコマース小売業の成長

- 製品の視認性向上に対する消費者の需要の高まり

- サステイナブル包装材料への移行

- 消費者は利便性と使いやすい包装を好む

- 包装ソリューションにおける技術的進歩

- 産業の潜在的リスク・課題

- カスタマイズとイノベーションにかかるコストが高め

- デザインの複雑さと消費者の期待

- 促進要因

- 成長可能性分析

- 規制情勢

- 技術

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推定・予測:包装形態別、2021~2034年

- 主要動向

- カウンター&ポップアップディスプレイボックス

- フロアスタンドディスプレイ

- パレットディスプレイ

- エンドキャップディスプレイ

- 透明包装

第6章 市場推定・予測:材料別、2021~2034年

- 主要動向

- プラスチック

- 紙と板紙

- ガラス

- 金属

- その他

- 軟質

第7章 市場推定・予測:最終用途産業別、2021~2034年

- 主要動向

- 飲食品

- 化粧品・パーソナルケア

- 医薬品

- 電子機器・民生用電子機器製品

- その他

第8章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- alphaglobalpackaging

- Amcor plc

- CustomBoxline

- DS Smith

- Graphic Packaging International, LLC

- Ibex Packaging

- International Paper

- Mondi Group

- Orora Visual

- Packaging Corporation of America

- PakFactory

- Rengo Co.

- Salazar Packaging

- Smurfit Kappa

- Stora Enso

- WestRock Company

目次

The Global Display Packaging Market was valued at USD 23.4 billion in 2024 and is estimated to grow at a CAGR of 5.4% to reach USD 39.3 billion by 2034, driven by the rapid growth in e-commerce continues to demand visually appealing packaging that enhances product visibility and encourages consumer engagement. As more shoppers opt for online purchases, the appeal of creative and branded display packaging becomes a key sales driver. Social media trends, particularly unboxing content, have amplified the importance of aesthetic packaging.

However, global trade tensions and tariffs-especially those initiated during the Trump administration-have disrupted supply chains by increasing the cost of raw materials like paperboard and plastic. These disruptions have resulted in production delays, impacting manufacturers and suppliers alike. Customization remains central to the success of display packaging as it helps brands differentiate and connect emotionally with consumers. The market's evolution is closely tied to sustainability, with rising interest in recyclable materials and eco-friendly design. As companies shift toward greener solutions, innovations in display packaging continue to emerge in response to changing consumer preferences and environmental regulations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $23.4 Billion |

| Forecast Value | $39.3 Billion |

| CAGR | 5.4% |

The display packaging industry encompasses formats designed to enhance product presentation and drive consumer engagement. These include endcap displays, pallet displays, transparent packaging, floor stand displays, and counter & pop-up display boxes. Each type serves a distinct purpose within the retail environment, The counter & pop-up display boxes segment is projected to reach USD 11.1 billion by 2034, emerging as one of the most impactful and commercially successful formats. These displays are driven by their ability to combine visual appeal with functional versatility. Brands favor these units for point-of-sale locations, where vibrant graphics, creative shapes, and strategic placement significantly influence purchase decisions.

Based on material usage, the plastic segment remains a leading choice across the industry and is expected to achieve a market value of USD 10.8 billion by 2034. The growing preference for transparent packaging has been instrumental in this growth, as consumers are more inclined to purchase items when the product is visible. This transparency builds trust and enhances shelf appeal. Simultaneously, the industry is undergoing a transition toward more eco-friendly plastic alternatives. Brands adopt recyclable and biodegradable plastics to meet tightening environmental standards and consumer demand for sustainable packaging.

Germany Display Packaging Market is forecasted to grow at a CAGR of 4.9% through 2034. The country's deep-rooted expertise in engineering and manufacturing is fueling innovation in packaging solutions, especially in lightweight yet durable cardboard materials. German companies focus on compact display designs that deliver maximum visibility without occupying excessive floor space. Integrating automation and digital printing technologies allows for rapid customization and scalable production, further solidifying Germany's position as a leader in the European display packaging landscape.

Key players shaping the competitive landscape include Smurfit Kappa, Mondi Group, DS Smith, International Paper, and WestRock Company. To solidify their market presence, leading display packaging companies are implementing strategies focused on innovation, strategic partnerships, and sustainable practices. They invest in R&D to develop eco-friendly packaging solutions that align with global environmental standards. Collaboration with retailers and brand owners allows for tailored designs that meet evolving consumer preferences. Companies are also expanding their global footprint through acquisitions and facility upgrades, enhancing production efficiency and geographic reach. Embracing digital technologies, such as smart packaging and automated production lines, is another core move to boost scalability and responsiveness in the fast-changing retail landscape.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw material)

- 3.2.2.1.1 Price volatility

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw material)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Growth of e-commerce retailing

- 3.3.1.2 Rising consumer demand for enhanced product visibility

- 3.3.1.3 Shift towards sustainable packaging materials

- 3.3.1.4 Consumer preference for convenience and easy-to-use packaging

- 3.3.1.5 Technological advancements in packaging solutions

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 High cost of customization and innovation

- 3.3.2.2 Design complexity and consumer expectations

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates & Forecast, By Packaging Type, 2021-2034 (USD Billion & Kilo Tons)

- 5.1 Key trends

- 5.2 Counter & pop-up display boxes

- 5.3 Floor stand displays

- 5.4 Pallet displays

- 5.5 Endcap displays

- 5.6 Transparent packaging

Chapter 6 Market Estimates & Forecast, By Material Type, 2021-2034 (USD Billion & Kilo Tons)

- 6.1 Key trends

- 6.2 Plastic

- 6.3 Paper & paperboard

- 6.4 Glass

- 6.5 Metal

- 6.6 Others

- 6.7 Flexible

Chapter 7 Market Estimates & Forecast, By End Use Industry, 2021-2034 (USD Billion & Kilo Tons)

- 7.1 Key trends

- 7.2 Food & beverage

- 7.3 Cosmetics & personal care

- 7.4 Pharmaceuticals

- 7.5 Electronics & appliances

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Bn & Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 alphaglobalpackaging

- 9.2 Amcor plc

- 9.3 CustomBoxline

- 9.4 DS Smith

- 9.5 Graphic Packaging International, LLC

- 9.6 Ibex Packaging

- 9.7 International Paper

- 9.8 Mondi Group

- 9.9 Orora Visual

- 9.10 Packaging Corporation of America

- 9.11 PakFactory

- 9.12 Rengo Co.

- 9.13 Salazar Packaging

- 9.14 Smurfit Kappa

- 9.15 Stora Enso

- 9.16 WestRock Company

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日