|

市場調査レポート

商品コード

1666951

据置型鉛蓄電池の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Stationary Lead Acid Battery Storage Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 据置型鉛蓄電池の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2024年12月23日

発行: Global Market Insights Inc.

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

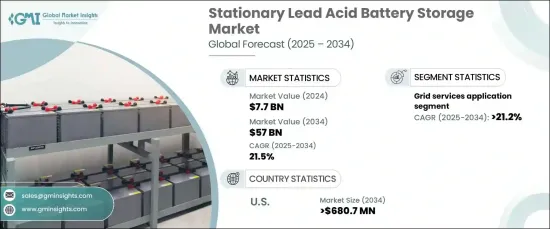

据置型鉛蓄電池の世界市場は、2024年に77億米ドルとなり、2025年から2034年にかけて21.5%のCAGRで成長する見込みです。

さまざまな分野で信頼性の高いエネルギー貯蔵ソリューションへの需要が高まっていることが、この成長を後押ししています。これらの電池は、費用対効果が高く、信頼性が高く長持ちするエネルギー貯蔵を提供する能力が特に評価されています。汎用性があるため、商業、工業、住宅用途で好まれています。技術の進歩により、性能、効率、耐久性が大幅に改善され、代替エネルギー貯蔵技術の出現にもかかわらず、その関連性が確保されています。これらの電池は一貫したエネルギー要件を満たすのに適しているため、重要な部門全体で中断のない電力供給の必要性が高まっており、需要を牽引し続けています。

据置型鉛蓄電池は、一貫した電力需要がある産業におけるバックアップ電源のニーズをサポートする上で極めて重要です。放電率が高く、寿命が長いため、大規模なエネルギー貯蔵システムにとって信頼性が高いです。これらの電池はまた、費用対効果が高く、リサイクルが比較的容易であるため、持続可能なソリューションを提供します。新興市場では、その手頃な価格と確立されたリサイクルインフラにより、鉛蓄電池システムの採用が増加しています。しかし、リチウムイオンバッテリーのような新しい技術は競合となり、大容量アプリケーションで信頼性の高い性能を発揮できる鉛蓄電池が依然として支持されています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 77億米ドル |

| 予測金額 | 570億米ドル |

| CAGR | 21.5% |

グリッドサービスにおける鉛蓄電池システムの利用は、予測期間中にCAGR21.2%と大きく成長すると予測されます。鉛蓄電池は信頼性とコスト面で優れているため、ピーク負荷管理や非常用電源の供給など、グリッドに不可欠な運用に適しています。電力会社は、送電網を安定させ、再生可能エネルギー源を統合し、大規模なエネルギー需要を効率的に満たすことができるバッテリーを高く評価しています。このセグメントにおける力強い成長の可能性は、世界のエネルギー貯蔵状況における鉛蓄電池の継続的な重要性を浮き彫りにしています。

米国の据置型鉛蓄電池市場は、2034年までに6億8,070万米ドルを超えると予想されています。産業および商業環境における信頼性の高いバックアップ電源の需要が主要な成長促進要因です。これらの電池はまた、グリッド負荷を管理し、再生可能エネルギー貯蔵を統合することにより、公益事業者をサポートしています。設計の革新により安全性が向上し、ライフサイクル性能が延長され、採用がさらに進んでいます。鉛の取り扱いと廃棄をめぐる規制の強化は課題ですが、電池のリサイクル技術の進歩を促し、電池の持続可能性に貢献しています。

目次

第1章 調査手法と調査範囲

- 市場の定義

- 基本推定と計算

- 予測計算

- データソース

- 一次

- 二次

- 有償

- 公的

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム分析

- 規制状況

- 業界への影響要因

- 成長促進要因

- 業界の潜在的リスク・課題

- 成長可能性分析

- ポーター分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- PESTEL分析

第4章 競合情勢

- 戦略ダッシュボード

- イノベーションと持続可能性の展望

第5章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- グリッドサービス

- Behind the meter

- オフグリッド

第6章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- フランス

- ドイツ

- イタリア

- ロシア

- スペイン

- アジア太平洋

- 中国

- オーストラリア

- インド

- 日本

- 韓国

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- トルコ

- 南アフリカ

- エジプト

- ラテンアメリカ

- ブラジル

- アルゼンチン

第7章 企業プロファイル

- CD Technologies

- Duracell

- Enersys

- Exide Industries

- Furukawa Battery

- GS Yuasa

- Johnson Controls

- Lockheed Martin

- Narada

- Panasonic

- Ritar

- Siemens

The Global Stationary Lead Acid Battery Storage Market, valued at USD 7.7 billion in 2024, is expected to grow at a CAGR of 21.5% from 2025 to 2034. The increasing demand for reliable energy storage solutions across various sectors is fueling this growth. These batteries are particularly valued for their cost-effectiveness and ability to provide dependable, long-lasting energy storage. Their versatility makes them a preferred choice in commercial, industrial, and residential applications. Technological advancements have significantly improved their performance, efficiency, and durability, ensuring their relevance despite the emergence of alternative energy storage technologies. The rising need for uninterrupted power supply across critical sectors continues to drive demand, as these batteries are well-suited to meet consistent energy requirements.

Stationary lead-acid batteries are crucial in supporting backup power needs in industries with consistent power demands. Their high discharge rates and extended lifespan make them highly dependable for large-scale energy storage systems. These batteries also offer a sustainable solution, as they are cost-effective and relatively easy to recycle. Emerging markets increasingly adopt lead-acid battery systems due to their affordability and established recycling infrastructure. However, newer technologies such as lithium-ion batteries present competition, and lead-acid batteries remain favored for their ability to deliver reliable performance for high-capacity applications.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.7 Billion |

| Forecast Value | $57 Billion |

| CAGR | 21.5% |

The use of lead-acid battery systems in grid services is projected to grow significantly over the forecast period, with a CAGR of 21.2%. Their reliability and cost advantages make them suitable for essential grid operations such as peak load management and emergency power supply. Utilities value these batteries for their capacity to stabilize grids, integrate renewable energy sources, and meet large-scale energy demands efficiently. The strong growth potential in this segment highlights their continued importance in the global energy storage landscape.

The stationary lead-acid battery storage market in the United States is anticipated to surpass USD 680.7 million by 2034. The demand for dependable backup power in industrial and commercial settings is a key growth driver. These batteries also support utilities by managing grid loads and integrating renewable energy storage. Innovations in design have improved safety and extended lifecycle performance, further enhancing their adoption. While stricter regulations surrounding lead handling and disposal present challenges, they also incentivize advancements in battery recycling technologies, contributing to their sustainability.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 – 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's Analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL Analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Strategic dashboard

- 4.2 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Application, 2021 – 2034 (USD Million & MW)

- 5.1 Key trends

- 5.2 Grid services

- 5.3 Behind the meter

- 5.4 Off grid

Chapter 6 Market Size and Forecast, By Region, 2021 – 2034 (USD Million & MW)

- 6.1 Key trends

- 6.2 North America

- 6.2.1 U.S.

- 6.2.2 Canada

- 6.2.3 Mexico

- 6.3 Europe

- 6.3.1 UK

- 6.3.2 France

- 6.3.3 Germany

- 6.3.4 Italy

- 6.3.5 Russia

- 6.3.6 Spain

- 6.4 Asia Pacific

- 6.4.1 China

- 6.4.2 Australia

- 6.4.3 India

- 6.4.4 Japan

- 6.4.5 South Korea

- 6.5 Middle East & Africa

- 6.5.1 Saudi Arabia

- 6.5.2 UAE

- 6.5.3 Turkey

- 6.5.4 South Africa

- 6.5.5 Egypt

- 6.6 Latin America

- 6.6.1 Brazil

- 6.6.2 Argentina

Chapter 7 Company Profiles

- 7.1 CD Technologies

- 7.2 Duracell

- 7.3 Enersys

- 7.4 Exide Industries

- 7.5 Furukawa Battery

- 7.6 GS Yuasa

- 7.7 Johnson Controls

- 7.8 Lockheed Martin

- 7.9 Narada

- 7.10 Panasonic

- 7.11 Ritar

- 7.12 Siemens