|

市場調査レポート

商品コード

1666688

自動車用ロボット市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Automotive Robotics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 自動車用ロボット市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2024年12月30日

発行: Global Market Insights Inc.

ページ情報: 英文 203 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

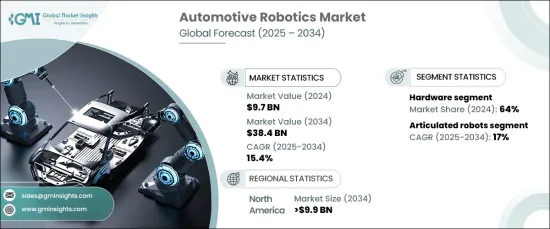

自動車用ロボットの世界市場は、2024年には97億米ドルとなり、2025年から2034年にかけてCAGR15.4%で拡大する見込みです。

この急成長の背景には、自動車製造の合理化、効率化、生産品質の向上を目的とした自動化への依存の高まりがあります。ロボット工学の業界への統合により、一貫性が確保され、エラーが減少し、生産性が向上し、自動化は組立、溶接、マテリアルハンドリングなどの主要な作業で不可欠になっています。

自動車用ロボットの需要を促進している主な要因の1つは、製造の精度と効率を向上させる必要性です。最新の車両設計、特に電気自動車やハイブリッド車の設計では、より高い精度が要求されます。溶接、塗装、組み立てなどの作業を、手作業を凌駕する精度で行うには、ロボットが欠かせないです。繰り返し作業の自動化により、生産時間が短縮され、処理能力が向上し、品質基準が維持されます。さらに、インダストリー4.0技術によって実現されるIoTやスマート・マニュファクチャリングとロボティクスの統合は、生産ワークフローを最適化し、運用コストを削減します。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 97億米ドル |

| 予測金額 | 384億米ドル |

| CAGR | 15.4% |

自動車用ロボット市場は、ハードウェア、ソフトウェア、サービスの3つの主要セグメントに分けられます。このうち、ハードウェア分野が最大のシェアを占め、2024年には市場の約64%を占めています。このセグメントには、ロボットアーム、センサー、アクチュエーター、コントローラーなどのコンポーネントが含まれ、これらはロボットシステムの精度、スピード、耐久性を高めるために極めて重要です。より高度で軽量かつ精密なハードウェアへの需要が高まる中、自動車生産における複雑な要求に応えるため、メーカーは最先端技術への投資を続けています。

ロボットの種類に関しては、多関節ロボットがその汎用性と精度の高さから市場を独占しています。溶接、塗装、マテリアルハンドリングなどの作業で特に威力を発揮します。多軸動作やリアルタイム調整など、多関節ロボットの高度な機能は、自動車製造における普及に貢献しています。その柔軟性により、大量生産とカスタマイズされた製造ニーズの両方に対応することができ、自動車セクターの自動化戦略には欠かせないものとなっています。

北米では、米国の自動車用ロボット市場は2034年までに99億米ドルを超えると予想されています。この分野での同国の成長は、高度な製造技術、スマート工場の採用、電気自動車(EV)の台頭が原動力となっています。AIと協働ロボット(cobot)の統合を含む柔軟な自動化システムへの注目は、市場の将来形成において重要な役割を果たすと予想されます。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

- 1次データ

- 2次データ

- 有料情報源

- 公的情報源

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- 破壊

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュース

- 規制状況

- 影響要因

- 促進要因

- 自動化需要の増加

- 電気自動車と自律走行車の需要急増

- 安全性と労働者の福利厚生への注目

- 協働ロボット(コボット)の台頭

- ロボット工学の継続的な技術進歩

- 業界の潜在的リスク&課題

- 高額な初期投資

- ロボット操作のための熟練労働者不足

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- ハードウェア

- コントローラー

- ロボットアーム

- エンドエフェクター

- センサー

- 視覚センサー

- フォース/トルクセンサ

- その他

- その他

- ソフトウェア

- サービス

第6章 市場推計・予測:ロボットタイプ別、2021年~2034年

- 主要動向

- 多関節ロボット

- 4軸ロボット

- 6軸ロボット

- その他

- スカラロボット

- 直交ロボット

- 円筒型ロボット

- その他

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- マテリアルハンドリング

- 溶接

- スポット溶接

- アーク溶接

- 組立/分解

- 検査

- 切断・加工

- 物流・倉庫自動化

- その他

第8章 市場推計・予測:ペイロード容量別、2021年~2034年

- 主要動向

- 16kgまで

- 16~60キロ

- 60~225キロ

- 225kg以上

第9章 市場推計・予測:展開タイプ別、2021年~2034年

- 主要動向

- 固定型ロボット

- 移動ロボット

- 無人搬送車(AGV)

- 自律移動ロボット(AMR)

第10章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- 機械学習と人工知能

- 3Dビジョンシステム

- IoT統合

- クラウドロボティクス

第11章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- その他ラテンアメリカ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- その他中東・アフリカ

第12章 企業プロファイル

- ABB

- Comau SpA

- Denso Wave

- Dürr AG

- Fanuc Corporation

- Harmonic Drive System

- Kawasaki Heavy Industries

- KUKA Robotics

- Nachi-Fujikoshi Corp

- Omron Corporation

- Panasonic Welding Systems Co. Ltd.

- Reis Gmbh &Co.

- Rockwell Automation

- Seiko Epson Corporation

- Stäubli

- Universal Robots

- Yamaha Robotics

- Yaskawa Electric Corporation

The Global Automotive Robotics Market, valued at USD 9.7 billion in 2024, is expected to expand at a CAGR of 15.4% from 2025 to 2034. This surge is driven by the increasing reliance on automation to streamline automotive manufacturing, improve efficiency, and enhance production quality. The integration of robotics into the industry ensures greater consistency, reduces errors, and boosts productivity, with automation becoming essential in key operations such as assembly, welding, and material handling.

One of the primary factors fueling the demand for automotive robotics is the need for improved manufacturing precision and efficiency. Modern vehicle designs, especially those involving electric or hybrid models, demand a higher level of accuracy. Robots are critical in performing tasks like welding, painting, and assembly, all with a level of precision that surpasses manual labor. The automation of repetitive tasks reduces production times, increases throughput, and maintains high-quality standards. Additionally, the integration of robotics with IoT and smart manufacturing, enabled by Industry 4.0 technologies, optimizes production workflows and lowers operational costs.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.7 Billion |

| Forecast Value | $38.4 Billion |

| CAGR | 15.4% |

The automotive robotics market is divided into three key segments: hardware, software, and services. Among these, the hardware segment holds the largest share, accounting for approximately 64% of the market in 2024. This segment includes components like robotic arms, sensors, actuators, and controllers, which are crucial for enhancing the accuracy, speed, and durability of robotic systems. As the demand for more advanced, lightweight, and precise hardware increases, manufacturers continue to invest in cutting-edge technology to meet the complex demands of automotive production.

When it comes to robot types, articulated robots dominate the market due to their versatility and precision. They are particularly effective in performing tasks such as welding, painting, and material handling. The advanced capabilities of articulated robots, including multi-axis movement and real-time adjustments, contribute to their widespread use in automotive manufacturing. Their flexibility allows them to cater to both mass production and customized manufacturing needs, making them an essential part of the automotive sector's automation strategy.

In North America, the U.S. automotive robotics market is expected to exceed USD 9.9 billion by 2034. The country's growth in this sector is driven by advanced manufacturing technologies, the adoption of smart factories, and the rise of electric vehicles (EVs). The focus on flexible automation systems, including the integration of AI and collaborative robots (cobots), is expected to play a key role in shaping the market's future.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.7 Growth drivers

- 3.7.1 Increased demand for automation

- 3.7.2 Surge in demand for electric and autonomous vehicles

- 3.7.3 Focus on safety and worker well-being

- 3.7.4 Rise of collaborative robots (cobots)

- 3.7.5 Ongoing technological advancements in robotics

- 3.8 Industry pitfalls & challenges

- 3.8.1 High Initial Investment

- 3.8.2 Skilled labor shortages for robotics operation

- 3.9 Growth potential analysis

- 3.10 Porter’s analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2023

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021-2034 (USD billion)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Controller

- 5.2.2 Robot arm

- 5.2.3 End-effector

- 5.2.4 Sensors

- 5.2.4.1 Vision sensors

- 5.2.4.2 Force/torque sensors

- 5.2.4.3 Others

- 5.2.5 Others

- 5.3 Software

- 5.4 Service

Chapter 6 Market Estimates & Forecast, By Robot Type, 2021-2034 (USD billion)

- 6.1 Key trends

- 6.2 Articulated robots

- 6.2.1 4-axis robots

- 6.2.2 6-axis robots

- 6.2.3 Others

- 6.3 Scara robots

- 6.4 Cartesian robots

- 6.5 Cylindrical robots

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD billion)

- 7.1 Key trends

- 7.2 Material handling

- 7.3 Welding

- 7.3.1 Spot welding

- 7.3.2 Arc welding

- 7.4 Assembly/disassembly

- 7.5 Inspection

- 7.6 Cutting and processing

- 7.7 Logistics and warehouse automation

- 7.8 Others

Chapter 8 Market Estimates & Forecast, By Payload Capacity, 2021-2034 (USD billion)

- 8.1 Key trends

- 8.2 Up to 16 kg

- 8.3 16–60 kg

- 8.4 60–225 kg

- 8.5 More than 225 kg

Chapter 9 Market Estimates & Forecast, By Deployment Type, 2021-2034 (USD billion)

- 9.1 Key trends

- 9.2 Fixed robots

- 9.3 Mobile robots

- 9.3.1 Automated Guided Vehicles (AGVs)

- 9.3.2 Autonomous Mobile Robots (AMRs)

Chapter 10 Market Estimates & Forecast, By Technology, 2021-2034 (USD billion)

- 10.1 Key trends

- 10.2 Machine learning and artificial intelligence

- 10.3 3D vision systems

- 10.4 IoT integration

- 10.5 Cloud robotics

Chapter 11 Market Estimates & Forecast, By Region, 2021-2034 (USD billion)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.4.6 Rest of Asia Pacific

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Rest of Latin America

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

- 11.6.4 Rest of MEA

Chapter 12 Company Profiles

- 12.1 ABB

- 12.2 Comau SpA

- 12.3 Denso Wave

- 12.4 Dürr AG

- 12.5 Fanuc Corporation

- 12.6 Harmonic Drive System

- 12.7 Kawasaki Heavy Industries

- 12.8 KUKA Robotics

- 12.9 Nachi-Fujikoshi Corp

- 12.10 Omron Corporation

- 12.11 Panasonic Welding Systems Co. Ltd.

- 12.12 Reis Gmbh & Co.

- 12.13 Rockwell Automation

- 12.14 Seiko Epson Corporation

- 12.15 Stäubli

- 12.16 Universal Robots

- 12.17 Yamaha Robotics

- 12.18 Yaskawa Electric Corporation