軍用電気光学/赤外線システム市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Military Electro-optics/Infrared (EO/IR) Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日

- 商品コード

- 1666663

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

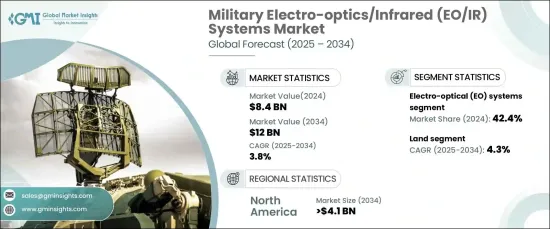

世界の軍用電気光学/赤外線(EO/IR)システム市場は、2024年に84億米ドルと評価され、2025年から2034年にかけてCAGR 3.8%で成長すると予測されています。

この成長は、高度な監視システム、特に情報、監視、偵察(ISR)に焦点を当てたシステムに対する需要の増加が原動力となっています。現代の軍隊は、広大な領土を監視し、新たな脅威を特定し、重要なインテリジェンスを収集するためにEO/IR技術に大きく依存しています。これらのシステムは、作戦の成功を確保しながら軍人の安全を守る上で重要な役割を果たしています。リアルタイムの脅威検知の必要性が高まるにつれ、軍隊は状況認識、戦略計画、戦術的意思決定の強化に不可欠な先進的EO/IRソリューションの開発と統合を優先しています。

EO/IRシステムは、夜間や悪天候などの悪条件下でも、軍人が比類ない精度で目標を追跡し、脅威を評価することを可能にします。リアルタイムの画像とデータ分析を提供するその能力は、現代の軍事作戦に不可欠であり、複雑な戦闘環境において技術的優位性を提供します。人工知能の統合や画像技術の向上など、これらのシステムの継続的な進歩に伴い、EO/IRソリューションは陸上、空中、艦艇の各プラットフォームの多様なニーズを満たすように進化しています。この動向は、急速に変化する戦闘状況において作戦上の優位性を維持するために、これらのシステムの重要性が高まっていることを反映しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 84億米ドル |

| 予測金額 | 120億米ドル |

| CAGR | 3.8% |

電気光学(EO)システム分野が圧倒的な市場シェアを占め、2024年の寄与率は42.4%です。これらのシステムは軍事用途に不可欠であり、偵察、目標識別、監視のための高解像度イメージング機能を提供します。EOシステムは可視光と近赤外光の両方を取り込み、低照度条件下でも鮮明な画像を提供するため、さまざまな軍事作戦で貴重な存在となっています。EO技術の開発は、解像度、射程距離、処理速度の向上に焦点を当て続けており、将来の進歩には、意思決定能力を強化した、より自律的なシステムが含まれる可能性が高いです。

陸上プラットフォーム上のEO/IRシステム市場は、予測期間中のCAGRが4.3%と、最も速い速度で成長すると予想されます。これらのシステムは、戦車や装甲兵員輸送車などの軍用車両に搭載され、地上監視と作戦効果を高めています。EO/IR技術により、軍隊は長距離かつ多様な環境で脅威を検知できるようになり、戦場の認識と安全性が向上します。陸上EO/IRシステムの進化は、より軽量な設計、より優れた耐久性、AI主導の分析に重点を置き、より迅速で正確な脅威の検知と対応を可能にしています。

北米は市場をリードし、2034年までに41億米ドル以上に達すると予測されています。同地域の高度防衛・監視技術に対する旺盛な需要は、特に米国における軍事近代化計画への多額の投資によって煽られています。人工知能の導入、状況認識の向上、共同作戦用のマルチプラットフォームシステムの開発に重点が置かれています。サイバーセキュリティ対策の強化と既存のプラットフォームのアップグレードも、新たな脅威に対する軍の即応性を確保するための重要な優先事項です。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

- 1次データ

- 2次データ

- 有料情報源

- 公的情報源

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- 破壊

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュースと取り組み

- 規制状況

- 影響要因

- 促進要因

- 情報・監視・偵察(ISR)のニーズの高まり

- 高度な状況認識に対する需要の高まり

- 先端技術の開発

- 無人航空機(UAV)またはドローンの利用拡大

- 軍備の近代化

- 業界の潜在的リスク&課題

- EO/IRシステムと幅広いプラットフォームとの統合に伴う複雑さ

- 高い開発・製造コスト

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:冷却技術別、2021年~2034年

- 主要動向

- 冷却

- 非冷却

第6章 市場推計・予測:センサー技術別、2021年~2034年

- 主要動向

- 凝視型センサー

- スキャニングセンサー

第7章 市場推計・予測:イメージング技術別、2021年~2034年

- 主要動向

- 電気光学(EO)システム

- 赤外線(IR)システム

- ハイパースペクトルおよびマルチスペクトルシステム

第8章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- ハンドヘルドシステム

- EO/IRペイロード

第9章 市場推計・予測:プラットフォーム別、2021年~2034年

- 主要動向

- 陸上

- 車両搭載型

- 戦闘車両

- 無人地上車両(UGV)

- 兵士システム

- 空挺

- 攻撃ヘリコプター

- 軍用機

- 戦闘機

- 輸送機

- 特殊任務機

- 無人航空機(UAV)

- 海軍

- 戦闘艦艇

- 無人水上機(USV)

第10章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 情報・監視・偵察(ISR)

- ターゲティング

- 状況認識

- ナビゲーション

- その他

第11章 市場推計・予測:POS別、2021年~2034年

- 主要動向

- OEM

- アフターマーケット

第12章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第13章 企業プロファイル

- Aselsan A.S.

- BAE Systems plc

- CONTROP Precision Technologies Ltd.

- Elbit Systems Ltd.

- Excelitas Technologies Corp.

- Hensoldt AG

- Indra Sistemas, S.A.

- Israel Aerospace Industries

- L3Harris Technologies, Inc.

- Leonardo S.p.A.

- Lockheed Martin Corporation

- Northrop Grumman

- Rafael Advanced Defense Systems Ltd.

- Rheinmetall AG

- Safran SA

- Teledyne FLIR LLC

- Textron Systems

- Thales Group

- Ultra Electronics Holdings plc

目次

The Global Military Electro-Optics/Infrared (EO/IR) Systems Market was valued at USD 8.4 billion in 2024 and is anticipated to grow at a CAGR of 3.8% from 2025 to 2034. This growth is driven by increasing demand for advanced surveillance systems, particularly those focused on Intelligence, Surveillance, and Reconnaissance (ISR). Modern armed forces rely heavily on EO/IR technologies to monitor large territories, identify emerging threats, and gather critical intelligence. These systems play a vital role in safeguarding military personnel while ensuring operational success. As the need for real-time threat detection escalates, military forces are prioritizing the development and integration of advanced EO/IR solutions, which are crucial for enhancing situational awareness, strategic planning, and tactical decision-making.

EO/IR systems enable military personnel to track targets and assess threats with unparalleled precision, even in adverse conditions such as nighttime or bad weather. Their ability to offer real-time imaging and data analysis is integral to modern military operations, providing a technological edge in complex combat environments. With ongoing advancements in these systems, including artificial intelligence integration and improved imaging technologies, EO/IR solutions are evolving to meet the diverse needs of land, airborne, and naval platforms. This trend reflects the growing importance of these systems for maintaining operational superiority in rapidly changing combat situations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.4 Billion |

| Forecast Value | $12 Billion |

| CAGR | 3.8% |

The electro-optical (EO) systems segment holds a dominant market share, contributing 42.4% in 2024. These systems are critical for military applications, offering high-definition imaging capabilities for reconnaissance, target identification, and surveillance. EO systems capture both visible and near-infrared light to provide clear images even in low-light conditions, making them invaluable for various military operations. The development of EO technology continues to focus on improving resolution, range, and processing speeds, with future advancements likely to include more autonomous systems equipped with enhanced decision-making capabilities.

The market for EO/IR systems on land platforms is expected to grow at the fastest rate, with a CAGR of 4.3% during the forecast period. These systems are installed on military vehicles, such as tanks and armored personnel carriers, to enhance ground surveillance and operational effectiveness. EO/IR technology enables military forces to detect threats over long distances and in diverse environments, improving battlefield awareness and safety. The ongoing evolution of land-based EO/IR systems emphasizes lighter designs, better durability, and AI-driven analysis, ensuring faster and more accurate threat detection and response.

North America is predicted to lead the market, reaching over USD 4.1 billion by 2034. The region's strong demand for advanced defense and surveillance technologies is fueled by significant investments in military modernization programs, particularly in the United States. The focus is on incorporating artificial intelligence, improving situational awareness, and developing multi-platform systems for joint operations. Enhancing cybersecurity measures and upgrading existing platforms are also key priorities to ensure military readiness against emerging threats.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Growing need for Intelligence, Surveillance, and Reconnaissance (ISR)

- 3.6.1.2 Increasing demand for advanced situational awareness

- 3.6.1.3 Development of advanced technologies

- 3.6.1.4 Growing use of unmanned aerial vehicles (UAVs) or drones

- 3.6.1.5 Modernization of military forces

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Complexity involved in integration of EO/IR System with wide range of platforms

- 3.6.2.2 High development and production costs

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Cooling Technology, 2021-2034 (USD Million)

- 5.1 Key trends

- 5.2 Cooled

- 5.3 Uncooled

Chapter 6 Market Estimates & Forecast, By Sensor Technology, 2021-2034 (USD Million)

- 6.1 Key trends

- 6.2 Staring sensor

- 6.3 Scanning sensor

Chapter 7 Market Estimates & Forecast, By Imaging Technology, 2021-2034 (USD Million)

- 7.1 Key trends

- 7.2 Electro-optical (EO) systems

- 7.3 Infrared (IR) systems

- 7.4 Hyper-spectral and multi-spectral systems

Chapter 8 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Million)

- 8.1 Key trends

- 8.2 Handheld system

- 8.3 EO/IR payload

Chapter 9 Market Estimates & Forecast, By Platform, 2021-2034 (USD Million)

- 9.1 Key trends

- 9.2 Land

- 9.2.1 Vehicle-mounted

- 9.2.2 Combat vehicles

- 9.2.3 Unmanned Ground Vehicles (UGVs)

- 9.2.4 Soldier system

- 9.3 Airborne

- 9.3.1 Attack helicopters

- 9.3.2 Military aircrafts

- 9.3.3 Fighter aircraft

- 9.3.4 Transport aircraft

- 9.3.5 Special mission aircraft

- 9.3.6 Unmanned Aerial Vehicles (UAVs)

- 9.4 Naval

- 9.4.1 Combat ships

- 9.4.2 Unmanned Surface Vehicles (USVs)

Chapter 10 Market Estimates & Forecast, By Application, 2021-2034 (USD Million)

- 10.1 Key trends

- 10.2 Intelligence, Surveillance, and Reconnaissance (ISR)

- 10.3 Targeting

- 10.4 Situational awareness

- 10.5 Navigation

- 10.6 Others

Chapter 11 Market Estimates & Forecast, By Point of Sale, 2021-2034 (USD Million)

- 11.1 Key trends

- 11.2 OEM

- 11.3 Aftermarket

Chapter 12 Market Estimates & Forecast, By Region, 2021-2034 (USD Million)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 UK

- 12.3.2 Germany

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Russia

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 South Korea

- 12.4.5 Australia

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.6 MEA

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 Aselsan A.S.

- 13.2 BAE Systems plc

- 13.3 CONTROP Precision Technologies Ltd.

- 13.4 Elbit Systems Ltd.

- 13.5 Excelitas Technologies Corp.

- 13.6 Hensoldt AG

- 13.7 Indra Sistemas, S.A.

- 13.8 Israel Aerospace Industries

- 13.9 L3Harris Technologies, Inc.

- 13.10 Leonardo S.p.A.

- 13.11 Lockheed Martin Corporation

- 13.12 Northrop Grumman

- 13.13 Rafael Advanced Defense Systems Ltd.

- 13.14 Rheinmetall AG

- 13.15 Safran SA

- 13.16 Teledyne FLIR LLC

- 13.17 Textron Systems

- 13.18 Thales Group

- 13.19 Ultra Electronics Holdings plc

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日