軍用電気光学・赤外線システム- 市場シェア分析、産業動向、成長予測(2025年~2030年)

Military Electro-optical And Infrared Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日

- 商品コード

- 1687049

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

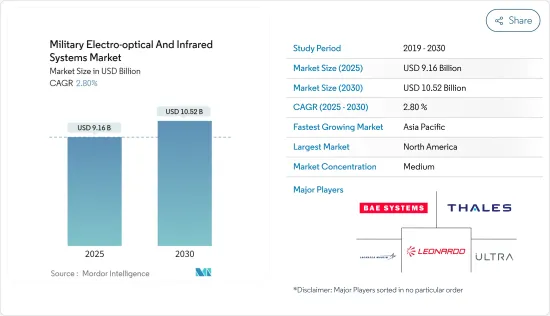

軍用電気光学・赤外線システム市場規模は、2025年に91億6,000万米ドルと推定され、予測期間(2025年~2030年)のCAGRは2.8%で、2030年には105億2,000万米ドルに達すると予測されます。

主なハイライト

- COVID-19パンデミックの発生とその後の操業停止は、防衛製造部門と数カ国の軍事研究開発活動のペースに影響を与えました。パンデミックの悪影響は、いくつかのプログラムが部品サプライヤーの独自の世界ネットワークに依存していたため、世界の防衛サプライチェーンに現れました。

- 様々な有人・無人システムのISR能力強化に対する需要の高まりにより、予測期間の後半には、調査対象市場は安定的に成長すると思われます。これらのシステムは電気光学/赤外線(EO/IR)センサーを利用します。各国は状況認識を向上させるため、これらのシステムを徐々に採用しています。

- しかし、様々な設計課題、技術的制約、サプライチェーンリスク、世界的危機の進展、前例のない要因が、予測期間中の市場成長を抑制すると予測されています。

軍用電気光学・赤外線システム市場動向

予測期間中、海上ベースセグメントが最も高い成長が見込まれる

- 市場の海上ベースセグメントは予測期間中に最も高いCAGRで推移すると予測されます。領土紛争や国境問題の増加により、軍の海上資産のリスクが高まり、海上での監視、脅威検出、標的識別が重視されるようになりました。近代的な戦闘ではこれらの能力が重視されるため、軍隊は洗練された高度なセンサー・システムを艦艇に組み込み、統合することに重点を置いています。

- 海軍の艦艇は、電気光学/赤外線(EO/IR)センサーから運動画像を取得する必要があり、昼夜を問わず長距離にわたってターゲットを監視し、ターゲットを識別する能力を向上させ、脅威評価を実行し、交戦規則によって意図を評価し、視線を通じて自動追跡と射撃統制ソリューションを通じて武器の交戦をサポートします。このように、海上での状況認識を向上させるために、海上パトロール用の信頼性が高く正確な、より優れたセンサーシステムの必要性が高まっています。

- さらに、艦艇は地形から隔離されているため、差し迫った脅威から長期間生き残るためには、高度な脅威検知・対策システムを保有することが重要になります。このことが、現在これらの海上ベースEO/IRセンサーの研究開発の成長を促進しています。いくつかの国は、海軍EO/IRセンサーシステムをアップグレードしています。例えば

- 2022年3月、海上自衛隊は新型ステルス・フリゲートを就役させました。特筆すべきは、三菱重工業が開発した先進的な統合戦闘情報センターです。このシステムは、オペレーターがすべての航行、推進、追跡、火器管制データを見ることができる大きな円形のスクリーンを備えています。同システムはカメラを通して乗組員に360度の視界を提供し、死角なく艦の周辺を見渡すことができます。残りの重要なシステムには、APY-2アクティブ電子スキャンアレイ(AESA)Xバンドレーダー、固定式および曳航式ソナー、OAX-3 EO/IRセンサーが含まれます。三菱電機はレーダーとEO/IRセンサーを供給しました。

- 米国海軍は2022年6月、L3ハリス・テクノロジーズ(L3Harris Technologies)率いるチームを選定し、艦隊防護強化のための艦上パノラマ光学/赤外線(SPEIR)システムを納入します。初期契約額は2億500万米ドルで、2031年3月まですべてのオプションが行使された場合の上限額は5億9,300万米ドルとなります。

- SPEIRプログラムは、360度電気光学および赤外線(EO/IR)画像と状況認識、さらに改良されたEO/IRセンサー(武器支援センサーから完全なパッシブ・ミッション・ソリューション能力へ)の使用における世代的飛躍を意味します。このような開発は、将来的に海上ベースのセグメントの見通しを強化すると予想されます。

北米が市場で上位を占める

- 北米が最大のシェアを占めたのは、主にEO/IRシステムに対する米国軍からの高い需要によるものです。戦場における敵の能力強化により、米国は技術的に進んだ兵器システムへの投資を増やさざるを得ませんでした。さらに、さまざまな世界的紛争への米軍の関与の高まりが、軍の状況認識を強化する先進的なISRやその他のシステムの調達増に大きく貢献しました。

- 2022年7月、米国下院は、2023年10月1日に始まる来年度の国防予算8,400億米ドルを承認しました。これにより国防総省の予算は370億米ドル増加し、ウクライナ軍への資金提供、中国との競争、アフガニスタン軍撤退問題への対応に重点が置かれます。一方、2022年4月、米下院は、戦火の絶えないウクライナや他の東欧諸国との防衛装備品貸与協定の基準を緩和する法案を承認し、米国製兵器がより多くこの地域に入る道を開いた。

- 2022年2月、米国陸軍は次世代レーザー標的探知機の計画を発表しました。国防ブログのウェブサイトは、陸軍の取得機関のブランチが、更新された性能要件を満たす自己完結型レーザーターゲットロケータモジュールIII(LTLM III)を生産し、提供するベンダーの能力を決定するために、業界に手を差し伸べていると報告しました。競合SPTDは、2023会計年度の第1四半期に競争発注契約を検討しており、記載されたタイムライン内で新しいロケータモジュールの要件を満たす実証された能力について、関心のある企業からの情報を求めています。

- 2021年8月、L3Harris Technologiesは、米国特殊作戦司令部からWESCAM MX電気光学、赤外線、レーザーデジグネーターセンサースイートとサービスを調達するための5年間、9,600万米ドルのIDIQ契約を獲得したと発表しました。このセンサーシステムは、米国陸軍特殊作戦航空部隊のインベントリ内の様々な航空機にマルチスペクトル画像と指定機能を提供することが期待されています。新しい電気光学センサに対する同様の受注と、先進的なEO/IRセンサによる様々な軍用システムのアップグレードが、予測期間中にこの地域の市場成長を促進すると予測されています。

軍用EO/IRシステム産業概要

軍用電気光学・赤外線システム市場は、半固有の性質を持っており、少数の企業が市場で大きなシェアを占めています。市場の著名な企業は、Leonardo S.p.A、BAE Systems plc、THALES、Ultra Electronics Holding、Lockheed Martin Corporationなどです。著名な市場企業は、多面的な製品ポートフォリオを有しています。さらに、継続的な研究開発を通じて現在の能力を修正・強化し、付加価値の高い電気光学/赤外線(EO/IR)ソリューションをエンドユーザーに提供するために洗練された機能を導入しようとしています。これはまた、差別化の低い製品を競争力のある価格で導入することにも役立っています。

ほとんどの統合プログラムは長期的なものであるため、エンドユーザーの仕様に沿った高度なEO/IRセンサーの設計変更と生産を意味するIDIQ契約が現在いくつか進行中です。エンドユーザーの要求は多様であるため、市場関係者間の戦略的協力が促進されます。

新たな統合プラットフォームの開発は、高度なEO/IRセンサーとシステムの統合に対する需要を促進し、その結果、予測期間中の市場には明るい見通しが生まれる可能性があります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- プラットフォーム

- 航空ベース

- 陸上型

- 海上ベース

- 地域

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- ラテンアメリカ

- メキシコ

- ブラジル

- その他のラテンアメリカ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- BAE Systems plc

- Elbit Systems Ltd.

- Teledyne FLIR LLC

- Israel Aerospace Industries Ltd.

- L3Harris Technologies Inc.

- Leonardo S.p.A

- Lockheed Martin Corporation

- Raytheon Technologies Corporation

- Rheinmetall AG

- Saab AB

- THALES

- Ultra Electronics Holdings

- Other Players

- Danbury Mission Technologies

- System Controls

- Zygo Corporation

- Navitar

- Optikos

第7章 市場機会と今後の動向

目次

The Military Electro-optical And Infrared Systems Market size is estimated at USD 9.16 billion in 2025, and is expected to reach USD 10.52 billion by 2030, at a CAGR of 2.8% during the forecast period (2025-2030).

Key Highlights

- The outbreak of the COVID-19 pandemic and the subsequent shutdowns affected the defense manufacturing sector and the pace of military R&D activities in several countries. The negative impacts of the pandemic were visible in the global defense supply chains, as several programs relied upon a unique global network of part suppliers.

- The market studied is likely to grow steadily during the latter half of the forecast period due to the growing demand for enhanced ISR capabilities for various manned and unmanned systems. These systems make use of electro-optical/infrared (EO/IR) sensors. Countries are progressively adopting these systems to increase their situational awareness.

- However, various design challenges, technological constraints, supply chain risks, the evolving global crisis, and unprecedented factors are projected to restrain the market growth during the forecast period.

Military Electro-optical and Infrared Systems Market Trends

The Sea-based Segment is Expected to Experience the Highest Growth During the Forecast Period

- The sea-based segment of the market is anticipated to register the highest CAGR during the forecast period. The growth of territorial conflicts and border issues increased the risk for maritime assets of militaries, which led to increasing emphasis on surveillance, threat detection, and target identification at sea. As modern combats emphasize these capabilities, armed forces mostly focus on incorporating and integrating sophisticated and advanced sensor systems into their naval vessels.

- Navy vessels need to obtain motion imagery from electro-optical/infrared (EO/IR) sensors that provide day-night and long-range eyes on the target, which improves their ability to identify targets, perform threat assessment, assess intent by the rules of engagement, and support weapon engagement through automatic tracking and fire control solutions through line-of-sight. Thus, the need for better sensor systems that are highly reliable and accurate for maritime patrol to improve sea-based situational awareness has increased.

- In addition, as the naval vessels are isolated from the terrain, it becomes important for them to possess advanced threat detection and countermeasure systems for their long-time survival from impending threats. This is driving the growth of research and development in these sea-based EO/IR sensors currently. Several nations are upgrading their naval EO/IR sensor systems. For instance,

- In March 2022, the Japan Maritime Self-Defense Force (JMSDF) commissioned a new stealth frigate into service. One notable feature is an advanced integrated combat information center developed by Mitsubishi Heavy Industries. This system has a large circular screen where operators may view all navigation, propulsion, tracking, and fire control data. The same system provides the crew 360 degrees of visibility through cameras, enabling them to see the areas around the ship without any blind spots. The remaining essential systems include an APY-2 active electronically scanned array (AESA) X-band radar, fixed and towed sonars, and an OAX-3 EO/IR sensor. Mitsubishi Electric supplied the radar and the EO/IR sensor.

- In June 2022, US Navy selected a team led by L3Harris Technologies to deliver a Shipboard Panoramic Electro-Optic/Infrared (SPEIR) system for enhancing fleet protection. The initial value of the contract is USD 205 million, with a ceiling value of USD 593 million if all the options are exercised until March 2031.

- The SPEIR program marks a generational leap in using 360-degree electro-optic and infrared (EO/IR) imagery and situational awareness, as well as improved EO/IR sensors - from a weapon support sensor to a completely passive mission solution capability. Such developments are expected to bolster the sea-based segment prospects in the future.

North America Held Highest Shares in the Market

- North America held the largest share, primarily due to high demand from the US armed forces for EO/IR systems. The enhanced capabilities of adversaries on the battlefield forced the US to increase its investment in technologically advanced weapon systems. Furthermore, the growing involvement of the US armed forces in various global conflicts significantly contributed to the increased procurement of advanced ISR and other systems that enhance the situational awareness of the military.

- In July 2022, the US House of Representatives recently approved the nation's USD 840 billion defense budget for the next fiscal year, which begins on October 1, 2023, for enhancing the mission readiness of various armed forces of the country. This will increase the Pentagon budget by USD 37 billion, focusing on providing funds to Ukraine's military, competing with China, and addressing the issues of Afghanistan's military withdrawal. Meanwhile, in April 2022, the US House of Representatives approved legislation that loosened the criteria for defense equipment lend-lease agreements with war-torn Ukraine and other countries in Eastern Europe, paving the path for more US weapons to enter the region.

- In February 2022, the US Army announced its plans for a next-generation laser target locator. The Defence Blog website reported that a branch of the Army's acquisition agency is reaching out to the industry to determine vendors' ability to produce and deliver a self-contained Laser Target Locator Module III (LTLM III) that meets updated performance requirements. The PdM SPTD is considering a competitively awarded contract in the first quarter of the fiscal year 2023 and is seeking information from interested companies on their demonstrated ability to meet the requirements for the new locator module within the stated timeline.

- In August 2021, L3Harris Technologies announced that it had received a five-year, USD 96 million IDIQ contract from the US Special Operations Command to procure WESCAM MX electro-optical, infrared, and laser designator sensor suites and services. The sensor systems are expected to provide multi-spectral imaging and designation capabilities for various aircraft within the US Army Special Operations Aviation Command inventory. Similar orders for new electro-optical sensors and the upgrading of various military systems with advanced EO/IR sensors are anticipated to propel the market growth in the region during the forecast period.

Military Electro-optical and Infrared Systems Industry Overview

The military electro-optical & infrared systems market is semi-consolidated in nature, with the presence of few players holding significant shares in the market. Some prominent players in the market are Leonardo S.p.A, BAE Systems plc, THALES, Ultra Electronics Holding, and Lockheed Martin Corporation. Prominent market players have multifaceted product portfolios. Additionally, they try to modify and enhance their current capabilities through continuous research and development and introduce sophisticated features to deliver value-added electro-optical/infrared (EO/IR) solutions to end users. This also helps them introduce low-differentiated products at competitive pricing.

Most of the integration programs are long-term; hence, several IDIQ contracts are currently underway, signifying design modification and production of sophisticated EO/IR sensors per end-user specifications. Since the end-user requirements are diverse, it encourages strategic collaboration between market players.

The development of new integration platforms drives the demand for the integration of sophisticated EO/IR sensors and systems, which, in turn, may create a positive outlook for the market during the forecast period.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Platform

- 5.1.1 Air-based

- 5.1.2 Land-based

- 5.1.3 Sea-based

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 United Kingdom

- 5.2.2.3 France

- 5.2.2.4 Italy

- 5.2.2.5 Spain

- 5.2.2.6 Russia

- 5.2.2.7 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 Japan

- 5.2.3.3 India

- 5.2.3.4 Australia

- 5.2.3.5 South Korea

- 5.2.3.6 Rest of Asia-Pacific

- 5.2.4 Latin America

- 5.2.4.1 Mexico

- 5.2.4.2 Brazil

- 5.2.4.3 Rest of Latin America

- 5.2.5 Middle East and Africa

- 5.2.5.1 United Arab Emirates

- 5.2.5.2 Saudi Arabia

- 5.2.5.3 South Africa

- 5.2.5.4 Rest of Middle East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 BAE Systems plc

- 6.2.2 Elbit Systems Ltd.

- 6.2.3 Teledyne FLIR LLC

- 6.2.4 Israel Aerospace Industries Ltd.

- 6.2.5 L3Harris Technologies Inc.

- 6.2.6 Leonardo S.p.A

- 6.2.7 Lockheed Martin Corporation

- 6.2.8 Raytheon Technologies Corporation

- 6.2.9 Rheinmetall AG

- 6.2.10 Saab AB

- 6.2.11 THALES

- 6.2.12 Ultra Electronics Holdings

- 6.3 Other Players

- 6.3.1 Danbury Mission Technologies

- 6.3.2 System Controls

- 6.3.3 Zygo Corporation

- 6.3.4 Navitar

- 6.3.5 Optikos

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日