|

市場調査レポート

商品コード

1850957

眼科用レーザー:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Ophthalmic Lasers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 眼科用レーザー:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月26日

発行: Mordor Intelligence

ページ情報: 英文 115 Pages

納期: 2~3営業日

|

概要

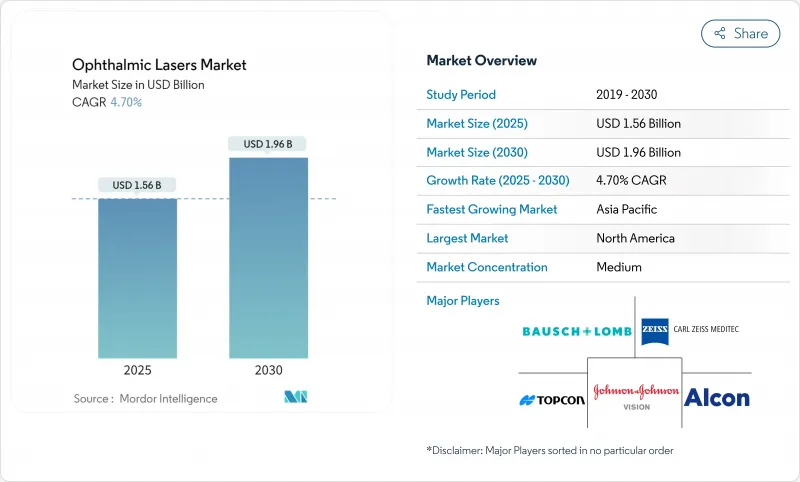

眼科用レーザー市場は、2025年に15億6,000万米ドルと評価され、2030年には19億6,000万米ドルに達し、CAGR 4.7%で進展すると予測されています。

フェムトセカンド・プラットフォームは、組織精度を維持しながら新たなスピード・ベンチマークを設定しています。北米は、高い手術件数と早期の規制承認によって需要を支えているが、アジア太平洋は、近視率の上昇と人口動態の高齢化が収束するにつれて、最も急な成長曲線を描いています。外来手術センター(ASC)とオフィスベースの手術室への持続的なシフトは、ポータブルで統合されたプラットフォームへの資本設備の嗜好を再構築しています。競合は現在、治療時間の短縮、治療結果の予測可能性の向上、臨床ワークフローの合理化を実現し、コスト抑制圧力下でも割高な価格設定を可能にするAI対応システムに軸足を置いています。

世界の眼科用レーザー市場の動向と洞察

眼科疾患の高い有病率

白内障はすでに2,050万人以上の米国人が罹患しており、増加の一途をたどっています。アジア太平洋では、視力障害の有病率が1990年から2015年にかけて17.9%上昇したため、さらなるプレッシャーが加わっています。これは主に都市部の近視と糖尿病に関連した網膜症が原因です。これらの重複する病態では、1回のセッションで光凝固、被膜切開、海綿体形成が可能な多目的レーザープラットフォームが必要とされることが多く、プロバイダは幅広いスペクトルのシステムを購入するよう促しています。人口動態の波はサービス契約収入も支えており、機器の利用率が高ければ予測可能なメンテナンスが必要となります。したがって、白内障、屈折矯正、網膜の各適応症にまたがる複合的な需要を取り込むには、完全なポートフォリオを持つメーカーが有利な立場にあります。

規制当局の承認と認可の増加

規制当局が真のイノベーションを受け入れるようになり、市場投入までの時間が短縮されています。FDAは2024年にボシュロムのTeneoエキシマープラットフォームを承認したが、これは20年ぶりのことです。ルミセラのValedaシステムは、ドライ型AMDに対する初の光バイオモジュレーション療法として認可され、治療のフロンティアが広がりました。欧州では、ViaLaseがフェムト秒緑内障治療でCEマークを取得し、Espansione Groupが光バイオモジュレーション装置の承認を取得しました。それぞれの承認取得により、対応可能な患者層が拡大し、臨床的な先例が確立されるため、将来の承認申請が容易になり、差別化された製品の健全なパイプラインがサポートされます。

高いシステム購入費とメンテナンス費

先進的なレーザー装置は50万米ドルから150万米ドルの間であり、年間サービス契約はその8-12%を吸収するため、小規模な診療所にはストレスとなります。新興国は、25~40%の輸入マークアップと通貨関連の変動に直面し、投資回収期間が長期化します。リースやシェアード・ユース・モデルは、キャッシュフローの障壁を軽減するもの、多くの場合、毎月の注射や処置に上限があるため、収益の上振れ幅が制限されます。その結果、グループ購買や複数施設の医療ネットワークでは、予測可能な料金でフリート全体のサービスをバンドルするベンダーが好まれ、市場は少数のスケール効率の良いサプライヤーへと向かっています。

セグメント分析

光凝固システムは2024年の眼科用レーザー市場シェアで38.3%を占めたが、これは網膜医療における役割が定着していることの証左です。しかし、フェムトセカンド・プラットフォームは2030年までCAGR 8.8%で推移し、超高速パルスレートが椅子にかかる時間と不快感を軽減します。VisuMax 800の2,000 kHzの速度は、スループットを向上させるだけでなく、角膜バイオメカニクスを維持するSMILE処置をサポートします。対照的に、エキシマ装置は、Teneoの1,740Hzのアイトラッキングのような漸進的な利得に依存しており、表面切除におけるその地位を強化しています。Nd:YAGディスラプターは引き続き被膜切開と硝子体溶解を支え、選択的レーザー海綿体形成術(SLT)システムは緑内障治療の選択肢を広げています。光凝固とフェムトセカンドまたはNd:YAGモジュールを統合した多目的コンソールは、資本効率の点でますます支持されています。

フェムト秒の急増は、熱から光による破壊的精度への移行を明確に示しています。AI主導のプランニングと人間工学的な改善を統合したベンダーは、プレミアムプレースメントを獲得しています。その結果、クロスプラットフォームエコシステムに投資するセグメントプレーヤーは、特にオールインワン機器を求める大量生産ASCにおいて、ニッチな専門家を凌駕することになります。金額ベースでは、フェムトセカンド装置の市場規模は2030年までに5億9,000万米ドルを獲得すると予測され、これは早期採用者の間での持続的な買い替え需要を反映しています。

白内障向けレーザは2024年に34.1%のシェアを確保したが、屈折異常矯正は2030年までのCAGRが9.4%と最も早い引き上げが期待されています。フェムト秒アシストLASIKとSMILEは現在、光学ゾーンの安定性とドライアイ発症率の低下で競合しており、小切開レンチクル挿入術では87%の視力維持率が報告されています。

サブスレッショルド・マイクロパルス・モダリティは、副次的損傷を制限することで網膜疾患管理を進歩させ、アルコンのVoyager DSLTのようなSLTイノベーションは、ゴニオレンズの取り扱いをなくし、緑内障ワークフローを簡素化します。屈折矯正アプリケーションの眼科用レーザー市場規模は、2025年の4億6,000万米ドルから2030年には7億1,000万米ドルに拡大すると予測されています。白内障破砕術、角膜再形成術、トラベキュロプラスティーを切り替え可能な統合コンソールは、混合症例にアピールし、従来の単一適応症の境界をさらに曖昧にします。

地域別分析

北米は2024年の売上高37.4%で眼科用レーザー市場をリードし、2030年まで1桁台半ばの成長が見込まれます。機器の普及率の高さ、有利な償還制度、FDAの早期認可がこの地域の優位性を維持しているが、外科医不足の問題が上向きに歯止めをかけています。予測では、2035年までに眼科医が30%不足し、地方へのアクセスは最も低下します。ASCへの移行と価値に基づく支払いは、合併症を減らすレーザーに報酬を与えるが、資本コストの上昇により、一部の診療所はリース・コンソーシアムやシェアード・サービス・モデルに移行しています。

アジア太平洋地域はCAGR 6.3%と最も急速に成長している地域です。近視の進行は、都市部の若年層では80%を超えており、高齢化と相まって白内障と屈折矯正の仕事量が増加しています。しかし、外科医の偏在と価格に敏感な調達は、メンテナンスの手間を省いた設計を支持しています。中国の数量ベースの調達は利幅を圧迫し、メーカーにバリュークラスのSKUを提供するよう促す一方、インドや東南アジアでは、アウトリーチキャンプに適したポータブルハンドヘルドユニットが重宝されています。根底にある疾病の蔓延を持続可能な機器導入に変えるには、強固な臨床研修提携と慈善プログラムが極めて重要です。

欧州は、CEマークの整合性と普遍的な保険適用により、着実な拡大を示しています。フェムトセカンド緑内障治療器と光バイオモジュレーション治療器のCE承認は2024年であり、規制当局の機敏性を示しています。しかし、国レベルの償還のニュアンスは市場の分断を生み、ベンダーは支払者ごとに価値提出書類を調整する必要があります。西欧では臨床結果データが重視される一方、東欧ではアフォーダビリティが重視され、同大陸内で需要の流れが二分されています。中東・アフリカと南米では、満たされていない手術ニーズが大きいが、サプライチェーンのギャップと為替リスクに悩まされています。寄付プログラム、移動手術キャラバン、政府による自己負担スキームにより、潜在的な可能性が徐々に開花する可能性があるが、短期的な成長はまだ緩やかです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 眼疾患の有病率の高さ

- 規制当局の承認と認可の増加

- フェムト秒およびエキシマ技術の継続的なアップグレード

- 検眼医の業務範囲拡大に関する法律

- ポータブル低エネルギー「テーブルトップ」レーザーで設備投資を削減

- AI駆動型パーソナライズアブレーションプロファイル

- 市場抑制要因

- システム購入と保守コストが高め

- レーザー訓練を受けた眼科医の不足

- EMにおけるFLACSコードの償還に関する不確実性

- 競合するプレミアムIOLと医薬品パイプラインが需要を抑制

- サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 製品別

- フェムト秒レーザー

- エキシマレーザー

- Nd:YAG光破壊レーザー

- 光凝固術/ダイオードおよびアルゴンレーザー

- 選択的レーザー線維柱帯形成術(SLT)レーザー

- パターンスキャン型光凝固装置

- 複合多目的プラットフォーム

- 用途別

- 白内障手術(FLACS、嚢切開術)

- 屈折異常矯正(LASIK、SMILE、PRK)

- 緑内障(SLT、緑内障光凝固術)

- 糖尿病網膜症とDME

- 加齢黄斑変性症

- 小児およびその他の網膜疾患

- エンドユーザー別

- 病院

- 専門眼科クリニック&チェーン

- 外来手術センター(ASC)

- 学術調査機関

- テクノロジー統合による

- スタンドアロンレーザーシステム

- 統合型超音波検査レーザーワークステーション

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 市場集中度

- 市場シェア分析

- 企業プロファイル

- Alcon

- Johnson & Johnson Vision

- Carl Zeiss Meditec

- Bausch+Lomb

- Topcon Corp

- IRIDEX Corp

- Lumenis

- Lumibird(Quantel Medical)

- NIDEK Co., Ltd.

- Ellex Medical Lasers

- Coherent Inc.

- Ziemer Ophthalmic Systems

- SCHWIND eye-tech-solutions

- LENSAR

- Lightmed

- Quantel Laser USA

- iVIS Technologies

- ViaLase

- ForSight Robotics

- WaveLight GmbH

- Haag-Streit Surgical