|

市場調査レポート

商品コード

1913320

無人交通管理市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測Unmanned Traffic Management Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 無人交通管理市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2026年01月05日

発行: Global Market Insights Inc.

ページ情報: 英文 235 Pages

納期: 2~3営業日

|

概要

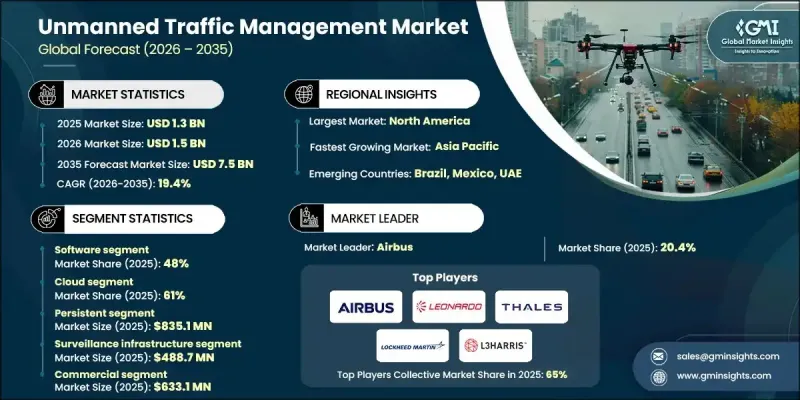

世界の無人交通管理市場は、2025年に13億米ドルと評価され、2035年までにCAGR 19.4%で成長し、75億米ドルに達すると予測されています。

市場成長は、商業・政府機関によるドローン運用の急増、安全な低高度空域管理への需要の高まり、ドローン交通を規制する枠組みの進化によって推進されています。組織や当局が無人航空機(UAV)を共有空域に安全に統合することに注力する中、タイムリーで安全かつ追跡可能なドローン運用を実現するためには、高度なUTMソリューションが不可欠となっています。市場の拡大は、ドローンの監視、飛行計画、運用効率を向上させる技術への投資増加によっても支えられています。業界を横断する利害関係者は、リアルタイムの状況認識を提供し、空域の競合を減らし、拡張性のある長期的な航空交通管理戦略を支援する、エンドツーエンドのデータ駆動型システムを優先しています。こうした進展により、UTMソリューションは世界中で安全かつ効率的なUAV運用の重要な基盤技術としての地位を確立しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 13億米ドル |

| 予測金額 | 75億米ドル |

| CAGR | 19.4% |

AIおよび機械学習による飛行経路最適化、IoTを活用したリアルタイム追跡、GPSおよびADS-B監視、クラウドベースのUTMプラットフォーム、自動ドローン調整システムなどの技術革新により、従来の空域管理は変革を遂げております。これらのツールは、ミッション計画やリアルタイム監視から衝突検知、規制順守に至るまで、UAV運用に対する完全な可視性と制御を提供します。統合デジタルプラットフォーム、自動化、分析技術の進化により、効率性向上、リスク低減、運用安全性の強化が進み、市場は発展を続けております。

ソフトウェア分野は48%のシェアを占め、2035年までCAGR20.1%で成長すると予測されています。ソフトウェアが優位を占める背景には、リアルタイムドローン追跡、空域監視、飛行経路最適化、包括的な交通管理における中核的役割があります。クラウドベースのUTMプラットフォーム、AIを活用した分析、IoT監視、モバイル対応アプリケーションは、オペレーター、規制当局、商業ユーザーがUAV運用を効率的に調整し、空域の安全性を維持し、パフォーマンスを最適化するのに役立ちます。

クラウドセグメントは2025年に61%のシェアを占め、2035年までCAGR18.8%で成長すると予想されています。クラウドソリューションが主流となっている背景には、拡張性、リアルタイムデータアクセス、導入コストの低さがあります。これにより、オペレーターや規制当局はドローンの交通状況を監視し、飛行経路を最適化し、潜在的な衝突を検知し、複数地域にわたる空域を管理することが可能となります。その柔軟性と統合能力により、クラウドプラットフォームは大規模なUAV運用に最適です。

米国の無人交通管理市場は78%のシェアを占め、2025年には3億6,710万米ドルを生み出しました。北米は、成熟したドローンエコシステム、先進的な空域インフラ、デジタル航空交通管理技術の早期導入により、世界市場をリードしています。この地域は、クラウドベースのプラットフォーム、AIを利用した分析、IoTを利用した追跡、リアルタイムのモニタリングが広く導入されているというメリットがあります。

世界の無人交通管理市場の主要企業には、レオナルド、L3ハリス、ロッキード・マーティン、エアバス、アルティチュード・エンジェル、プレシジョンホーク、フレクエンティス、タレス、ユニフライなどがあります。世界の無人交通管理市場の企業は、リアルタイムの空域監視と自動化された衝突解決を強化するソフトウェアおよびクラウドベースのソリューションに多額の投資を行い、その存在感を強化しています。ドローン事業者、規制当局、テクノロジープロバイダーと戦略的パートナーシップを構築し、エンドツーエンドのUAV管理のための統合プラットフォームを構築しています。AI、機械学習、IoT対応システムにおける継続的な研究開発は、企業が飛行経路の最適化、状況認識、予測分析の改善に役立っています。また、複数の企業が成長著しい地域へのサービス提供を目的に世界の展開を拡大し、拡張性、規制順守、顧客エンゲージメントの強化を図っております。柔軟性、相互運用性、データ駆動型ソリューションに注力することで、企業は長期的な競争優位性を構築し、より大きな市場シェアを獲得することが可能となります。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 商用ドローン運用の急速な拡大

- 規制要件と安全基準

- 技術的進歩

- 都市型航空モビリティ(UAM)と視界外飛行(BVLOS)の拡大

- 業界の潜在的リスク&課題

- 分断された世界の規制

- 初期費用の高さ

- 市場機会

- スマートシティ及びIoTネットワークとの統合

- 新興市場への展開

- 政府・防衛分野における無人航空機(UAV)の導入

- 高度な分析とAI駆動型最適化

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 米国連邦航空局(FAA)リモートID規則

- 米国国家空域システム(NAS)ガイドライン

- 欧州

- ドイツ連邦交通・デジタル化省(BMVI)及びドイツ連邦航空局(DFS)の規制

- フランスDGAC(民間航空総局)及びANAF(国家税務庁)ガイドライン

- 英国民間航空局(CAA)及び無人航空機システム(UAS)規制

- イタリアENACガイドライン

- アジア太平洋地域

- 中国民用航空局(CAAC)及び無人航空機システム(UAS)規制

- 日本JCABドローンガイドライン

- 韓国国土交通省(MOLIT)及びドローン規制

- インドDGCAドローン規則及びUINシステム

- ラテンアメリカ

- ブラジルANAC及びDECEAガイドライン

- メキシコDGAC無人航空機規制

- 中東・アフリカ

- UAE GCAAドローン規制

- サウジアラビアGACAドローンガイドライン

- 北米

- ポーター分析

- PESTEL分析

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- コスト内訳分析

- 特許分析

- 持続可能性と環境面

- 持続可能な実践

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に配慮した取り組み

- カーボンフットプリントに関する考慮事項

- 使用事例シナリオ

- UTMシステムアーキテクチャと空域モデル

- 集中型と分散型のUTMアーキテクチャ

- 戦術的衝突回避と戦略的衝突回避

- 有人航空交通管理システムとの統合

- 相互運用性と標準化フレームワーク

- UTMビジネスモデルと収益化モデル

- 利害関係者のエコシステムとガバナンスモデル

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 事業拡大計画と資金調達

第5章 市場推計・予測:コンポーネント別、2022-2035

- ソフトウェア

- ハードウェア

- サービス

第6章 市場推計・予測:タイプ別、2022-2035

- 持続的

- 非持続性

第7章 市場推計・予測:導入モデル別、2022-2035

- オンプレミス

- クラウド

第8章 市場推計・予測:用途別、2022-2035

- 監視インフラストラクチャ

- 通信インフラ

- 航行支援インフラ

- その他

第9章 市場推計・予測:最終用途別、2022-2035

- 商業用

- 政府

- 非公開

第10章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ベルギー

- オランダ

- スウェーデン

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- シンガポール

- 韓国

- ベトナム

- インドネシア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ地域

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第11章 企業プロファイル

- Global Player

- Airbus

- Altitude Angel

- Frequentis

- Honeywell International

- L3 Harris

- Leonardo

- Lockheed Martin

- PrecisionHawk

- Thales

- Unifly

- Regional Player

- AirMap

- Airspace Link

- ANRA Technologies

- Dedrone

- DroneDeploy

- Flytrex

- Kittyhawk

- SkyGrid

- Terra Drone

- uAvionix

- 新興企業

- Airborne Robotics

- Drone Harmony

- Simulyze

- UAV Navigation

Volocopter UT