|

市場調査レポート

商品コード

1666543

ツルマメ種子エキスの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Glycine Soja (Soybean) Seed Extract Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| ツルマメ種子エキスの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2024年12月27日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

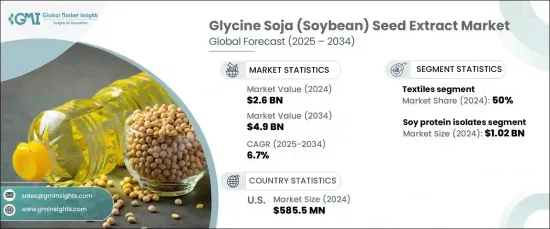

ツルマメ(大豆)種子エキスの世界市場は、2024年に26億米ドルの推定値を記録し、2025年から2034年にかけてCAGR6.7%の力強い成長率を遂げる見込みです。

大豆に由来するツルマメ種子エキスは、スキンケアおよび化粧品業界の強力な成分であり、肌に潤いを与え、抗酸化保護を提供する能力で珍重されています。世界の産業界が持続可能で高性能なソリューションを優先し続ける中、大豆由来エキスの市場はこうした需要に応えるべく進化しています。天然で環境に優しい製品を求める消費者の選好を受け、各社は厳しい環境規制を遵守しながら、より効率的な製剤を革新的に開発しています。このような進歩により、ツルマメ種子エキス市場は、競合が激しく、急速に変化する世界情勢の中で長期的な成功を収めています。

市場は、大豆イソフラボン、分離大豆タンパク質、大豆レシチン、サポニン、大豆リン脂質など製品タイプ別に区分されます。2024年には、分離大豆タンパク質が主導権を握り、10億2,000万米ドルの大幅な市場シェアを獲得します。これらの大豆ベースの製品に対する需要は近年急増しており、その主な理由は複数の産業にわたる多目的な用途によるものです。大豆レシチンは、その卓越した乳化特性により、食品製造や医薬品に広く使用されています。一方、大豆リン脂質は、その多機能性が評価され、化粧品製剤や栄養補助食品での使用が増加しており、市場の成長をさらに促進しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 26億米ドル |

| 予測金額 | 49億米ドル |

| CAGR | 6.7% |

用途別では、ツルマメ(大豆)種子エキス市場は、化粧品・パーソナルケア、食品・飲料、栄養補助食品、医薬品、飼料などの主要分野に分けられます。2023年に50%のシェアを占めた繊維産業は、依然として市場の支配的プレイヤーです。健康とウェルネスに対する消費者の関心の高まりが、栄養補助食品、栄養補助食品、パーソナルケアアイテムにおける大豆由来製品の採用を加速させています。タンパク質、オメガ3脂肪酸、イソフラボンのような主要大豆成分は、その多くの健康上の利点から人気が高まっており、これらの分野での拡大を牽引しています。

米国のツルマメ種子エキス市場は特に好調で、2024年には5億8,550万米ドルを生み出しました。この国の市場成長は、健康志向の消費者がよりクリーンで透明性の高い選択肢を求めるようになり、自然で持続可能な製品に対する需要が高まっていることが背景にあります。大豆は食品、化粧品、医薬品を含む様々な分野に適応できるため、市場での継続的な関連性が保証され、米国が世界市場で主導的な地位をさらに強固なものにしています。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

- 一次

- 二次

- 有料ソース

- 公的ソース

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- 変革

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュース

- 規制状況

- 影響要因

- 成長促進要因

- 機能性食品・飲料の需要の高まり

- 医薬品・栄養補助食品用途の拡大

- 化粧品・パーソナルケア市場の拡大

- 業界の潜在的リスク・課題

- 消費者の認識と大豆アレルギー

- 成長促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業市場シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場規模・予測:製品別、2021年~2034年

- 主要動向

- 大豆たんぱく分離物(SPI)

- 大豆レシチン

- 大豆リン脂質

- 大豆イソフラボン

- サポニン

第6章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- 食品・飲料

- 栄養補助食品・栄養補助食品

- 化粧品・パーソナルケア

- 動物飼料

- 医薬品

第7章 市場規模・予測:流通チャネル別、2021年~2034年

- 主要動向

- 直販

- 成分販売業者

- オンライン小売業者

第8章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Archer Daniels Midland Company

- BASF SE

- Bellatorra Skin Care

- Bio-alternatives

- Cargill

- Global Essence

- Grau Aromatics

- Ingredion Incorporated

- JF Natural Ingredients

- Lucas Meyer Cosmetics

- Natural Solution

- Symrise

- The Organic Pharmacy

- Wanrun Bio-Technology

The Global Glycine Soja (Soybean) Seed Extract Market, with an estimated value of USD 2.6 billion in 2024, is set to experience a robust growth rate of 6.7% CAGR from 2025 to 2034. Derived from soybeans, glycine soja seed extract is a powerhouse ingredient in the skincare and cosmetics industries, prized for its ability to hydrate the skin and provide antioxidant protection. As global industries continue to prioritize sustainable and high-performance solutions, the market for soybean-based extracts is evolving to meet these demands. In response to consumer preferences for natural and eco-friendly products, companies are innovating and developing more efficient formulations while adhering to strict environmental regulations. These advancements position the glycine soja seed extract market for long-term success in a competitive, rapidly changing global landscape.

The market is segmented by product type, including soy isoflavones, soy protein isolates, soy lecithin, saponins, and soybean phospholipids. In 2024, soy protein isolates lead the charge, capturing a substantial market share worth USD 1.02 billion. The demand for these soy-based products has surged in recent years, largely due to their versatile applications across multiple industries. Soy lecithin is widely used in food production and pharmaceuticals due to its exceptional emulsifying properties while soybean phospholipids, valued for their multifunctionality, have seen increased use in cosmetic formulations and dietary supplements, further fueling market growth.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.6 Billion |

| Forecast Value | $4.9 Billion |

| CAGR | 6.7% |

In terms of application, the glycine soja (soybean) seed extract market is divided into key sectors such as cosmetics and personal care, food and beverages, nutraceuticals and dietary supplements, pharmaceuticals, and animal feed. The textiles industry, which held a 50% share in 2023, remains a dominant player in the market. Consumers' growing interest in health and wellness has accelerated the adoption of soy-derived products in nutraceuticals, dietary supplements, and personal care items. Key soy ingredients like protein, omega-3 fatty acids, and isoflavones are becoming more popular for their numerous health benefits, driving expansion across these sectors.

The U.S. glycine soja seed extract market is particularly strong, generating USD 585.5 million in 2024. The nation's market growth is fueled by the increasing demand for natural, sustainable products as health-conscious consumers seek cleaner, more transparent options. Soy's adaptability across various sectors, including food, cosmetics, and pharmaceuticals, ensures its continued relevance in the market, further solidifying the U.S.'s leading position in the global market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Rising demand for functional food and beverages

- 3.6.1.2 Growing pharmaceutical and nutraceutical applications

- 3.6.1.3 Expanding cosmetics and personal care market

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Consumer perception and soy allergies

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Size and Forecast, By Product, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Soy Protein Isolates (SPIs)

- 5.3 Soy lecithin

- 5.4 Soybean phospholipids

- 5.5 Soy isoflavones

- 5.6 Saponins

Chapter 6 Market Size and Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Food & beverages

- 6.3 Nutraceuticals & dietary supplements

- 6.4 Cosmetics & personal care

- 6.5 Animal feed

- 6.6 Pharmaceuticals

Chapter 7 Market Size and Forecast, By Distribution channel, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Direct sales

- 7.3 Ingredient distributors

- 7.4 Online retailers

Chapter 8 Market Size and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Archer Daniels Midland Company

- 9.2 BASF SE

- 9.3 Bellatorra Skin Care

- 9.4 Bio-alternatives

- 9.5 Cargill

- 9.6 Global Essence

- 9.7 Grau Aromatics

- 9.8 Ingredion Incorporated

- 9.9 JF Natural Ingredients

- 9.10 Lucas Meyer Cosmetics

- 9.11 Natural Solution

- 9.12 Symrise

- 9.13 The Organic Pharmacy

- 9.14 Wanrun Bio-Technology