|

市場調査レポート

商品コード

1665328

シードドリルとブロードキャストシーダーの市場機会と促進要因、産業動向分析、2025年~2034年予測Seed Drill and Broadcast Seeder Machinery Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| シードドリルとブロードキャストシーダーの市場機会と促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2024年12月23日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

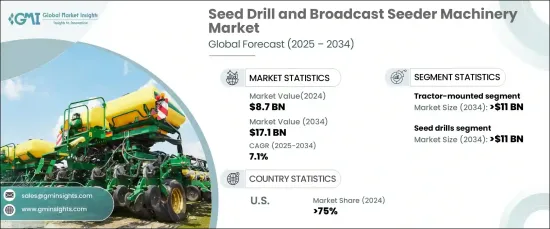

世界のシードドリルとブロードキャストシーダー機械市場は、2024年に87億米ドルに達し、2025~2034年にかけて7.1%のCAGRで堅調に成長すると予測されています。

2050年までに97億人に達すると予想される世界人口の増加が、農業生産性の向上に対する需要に拍車をかけています。シードドリルとブロードキャストシーダーは、この需要を満たすために不可欠なツールであり、作付け効率の向上、コストの削減、作物収量の最適化によって食糧安全保障を大幅に強化し、増大する食糧需要を満たします。

2024年には、シードドリルが市場の65%以上のシェアを占め、市場を独占しています。このセグメントは2034年までに110億米ドルに達すると予想されています。精密農業技術の急速な進歩がシードドリル市場に革命をもたらしています。可変率播種、GPSガイダンス、リアルタイムデータシステムなどの機能は、シード配置の改善を促進し、土壌条件に応じて播種率を最適化し、最終的に作物収量を高めています。AIを搭載したセンサは、深さ制御、間隔、養分分配をさらに強化し、よりスマートで正確な植え付けソリューションを記載しています。さらに、スマート接続性は、リアルタイムのモニタリング、フィールドマッピング、データ主導の意思決定を可能にし、より効率的でサステイナブル農業アプローチを生み出します。持続可能性の推進が強化され続ける中、先進的で資源効率の高いシードドリルに対する需要は増加の一途をたどっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 87億米ドル |

| 予測金額 | 171億米ドル |

| CAGR | 7.1% |

市場は推進力タイプによっても区分され、トラクター搭載型、手動/手押し式、自走式などの選択肢があります。このうちトラクター搭載型は、2034年までに110億米ドルの売上が見込まれています。メーカーは、カーボンフットプリントの削減、燃料効率の改善、土壌への影響の最小化を特徴とするシードドリルの開発により、持続可能性を優先しています。これらのトラクター搭載型システムは、不耕起や減耕起農法などの保全型農業に適しており、土壌の健全性を保ち、浸食を減らすのに役立ちます。このセグメントにおける革新は、軽量材料、エネルギー効率の高い設計、電気トラクターやハイブリッドトラクターとの互換性に重点を置き、規制基準に適合させ、サステイナブル農業技術を促進します。

米国では、シードドリルとブロードキャストシーダー市場が2024年に75%の圧倒的シェアを占めます。同国では、自律型とロボット型シードドリル技術の採用が急増しています。人工知能(AI)、コンピューター・ビジョン、精密GPSと統合された新しい電気式と水素駆動モデルが、植え付けプロセスの大幅な改善を推進しています。これらの先進的機械は、播種中のリアルタイム調整を可能にし、播種効率を最適化します。機械学習技術は、多様な圃場条件への適応性をさらに高め、労働力不足に対処し、作業コストを削減し、生産性を向上させています。最先端の農業機器への継続的な投資が市場の成長を促し、このセグメントの技術革新に拍車をかけています。

報告書の内容

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 産業洞察

- エコシステム分析

- サプライヤーの状況

- 機器メーカー

- 販売業者

- 技術プロバイダー

- システムインテグレーター

- エンドユーザー

- 利益率分析

- 差別化技術

- GPSとGNSSガイダンスシステム

- 可変速度播種(VRS)

- 自律型播種機

- リアルタイムデータモニタリング

- その他

- コスト内訳分析

- 製造コスト

- 原料

- 人件費

- 研究開発費

- マーケティング・流通コスト

- アフターサービス費用

- その他

- 製造コスト

- 主要ニュースと取り組み

- 特許分析

- 規制状況

- 影響要因

- 促進要因

- 食糧安全保障に対する世界的需要

- 精密農業技術の採用増加

- 農業機器の経済効率に対する需要の高まり

- サステイナブル農業への嗜好の変化

- 産業の潜在的リスク・課題

- 土壌適合性の制約

- 高い初期投資コスト

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推定・予測:機器別、2021~2034年

- 主要動向

- シードドリル

- シングルディスク

- ダブルディスク

- エアシード

- 肥料シード

- ブロードキャストシーダー

- マウント型ブロードキャスト

- 牽引式

- 自走式

第6章 市場推定・予測:推進力別、2021~2034年

- 主要動向

- 手動/手押し式

- トラクター搭載

- 自走式

第7章 市場推定・予測:用途別、2021~2034年

- 主要動向

- 穀類

- 豆類

- 油糧種子

- 牧草

- 被覆作物

第8章 市場推定・予測:最終用途別、2021~2034年

- 主要動向

- 個人農業従事者

- 農業請負業者

- 政府/研究機関

第9章 市場推定・予測:流通チャネル別、2021~2034年

- 主要動向

- オンライン

- オフライン

第10章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第11章 企業プロファイル

- AGCO

- Amazonen Werke

- Bourgault Industries

- BUPL(FieldKing)

- Claas

- CNH Industrial

- Great Plains

- Horsch

- John Deere

- Kubota

- Kuhn

- Kverneland Group

- Landforce

- Lemken

- Mahindra &Mahindra

- Morris Equipment

- National Agro Industries

- Pottinger

- Tume

- Vaderstad

- Yanmar

- Zoomlion

The Global Seed Drill And Broadcast Seeder Machinery Market reached USD 8.7 billion in 2024 and is projected to grow at a robust CAGR of 7.1% from 2025 to 2034. The increasing global population, expected to hit 9.7 billion by 2050, is fueling the demand for greater agricultural productivity. Seed drills and broadcast seeders are essential tools in meeting this demand, significantly enhancing food security by improving planting efficiency, lowering costs, and optimizing crop yields to satisfy growing food requirements.

In 2024, seed drills dominated the market, capturing over 65% of the share. This segment is anticipated to reach USD 11 billion by 2034. The rapid advancements in precision agriculture technologies are revolutionizing the seed drill market. Features like variable rate seeding, GPS guidance, and real-time data systems are driving improvements in seed placement, optimizing seeding rates according to soil conditions, and ultimately boosting crop yields. AI-powered sensors further enhance depth control, spacing, and nutrient distribution, offering smarter, more precise planting solutions. Additionally, smart connectivity enables real-time monitoring, field mapping, and data-driven decision-making, creating a more efficient and sustainable farming approach. As the push for sustainability continues to intensify, the demand for advanced, resource-efficient seed drills remains on the rise.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.7 billion |

| Forecast Value | $17.1 billion |

| CAGR | 7.1% |

The market is also segmented by propulsion type, with options including tractor-mounted, manual/hand-operated, and self-propelled systems. Among these, the tractor-mounted segment is expected to generate USD 11 billion by 2034. Manufacturers are prioritizing sustainability by developing seed drills that feature reduced carbon footprints, improved fuel efficiency, and minimized soil impact. These tractor-mounted systems are well-suited for conservation agriculture practices such as no-till and reduced-till farming, helping to preserve soil health and reduce erosion. Innovations in this space focus on lightweight materials, energy-efficient designs, and compatibility with electric and hybrid tractors, aligning with regulatory standards and promoting sustainable farming techniques.

In the U.S., the seed drill and broadcast seeder machinery market held a dominant 75% share in 2024. The country is witnessing a surge in the adoption of autonomous and robotic seed drill technologies. New electric and hydrogen-powered models, integrated with artificial intelligence (AI), computer vision, and precision GPS, are driving significant improvements in the planting process. These advanced machines enable real-time adjustments during seeding, optimizing planting efficiency. Machine learning technologies are further enhancing adaptability to diverse field conditions, addressing labor shortages, reducing operational costs, and increasing productivity. Continued investments in cutting-edge agricultural equipment are fueling market growth and spurring innovation in the sector.

Report Content

Chapter 1 Methodology and Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Equipment manufacturers

- 3.2.2 Distributors

- 3.2.3 Technology providers

- 3.2.4 System integrators

- 3.2.5 End users

- 3.3 Profit margin analysis

- 3.4 Technology differentiators

- 3.4.1 GPS and GNSS guidance systems

- 3.4.2 Variable rate seeding (VRS)

- 3.4.3 Autonomous seeding machines

- 3.4.4 Real-time data monitoring

- 3.4.5 Others

- 3.5 Cost breakdown analysis

- 3.5.1 Manufacturing costs

- 3.5.1.1 Raw materials

- 3.5.1.2 Labor costs

- 3.5.2 R & D costs

- 3.5.3 Marketing and distribution costs

- 3.5.4 After-sales service costs

- 3.5.5 Others

- 3.5.1 Manufacturing costs

- 3.6 Key news and initiatives

- 3.7 Patent analysis

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Global demand for food security

- 3.9.1.2 Increasing adoption of precision agriculture technologies

- 3.9.1.3 Growing demand for economic efficiency for agriculture equipment

- 3.9.1.4 Changing preferences towards sustainable agriculture

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Soil compatibility constraints

- 3.9.2.2 High initial investment costs

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Equipment, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Seed drills

- 5.2.1 Single-disc

- 5.2.2 Double-disc

- 5.2.3 Air seed

- 5.2.4 Fertilizer seed

- 5.3 Broadcast seeders

- 5.3.1 Mounted-broadcast

- 5.3.2 Tow-behind

- 5.3.3 Self-propelled

Chapter 6 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Manual/hand operated

- 6.3 Tractor-mounted

- 6.4 Self-propelled

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Cereals

- 7.3 Legumes

- 7.4 Oil seeds

- 7.5 Grasses

- 7.6 Cover crops

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Individual farmers

- 8.3 Agricultural contractors

- 8.4 Government/research institutes

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Online

- 9.3 Offline

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 AGCO

- 11.2 Amazonen Werke

- 11.3 Bourgault Industries

- 11.4 BUPL (FieldKing)

- 11.5 Claas

- 11.6 CNH Industrial

- 11.7 Great Plains

- 11.8 Horsch

- 11.9 John Deere

- 11.10 Kubota

- 11.11 Kuhn

- 11.12 Kverneland Group

- 11.13 Landforce

- 11.14 Lemken

- 11.15 Mahindra & Mahindra

- 11.16 Morris Equipment

- 11.17 National Agro Industries

- 11.18 Pottinger

- 11.19 Tume

- 11.20 Väderstad

- 11.21 Yanmar

- 11.22 Zoomlion