|

市場調査レポート

商品コード

1665035

自動車用バッテリーディスコネクトユニット市場の機会、成長促進要因、産業動向分析、2025~2034年の予測Automotive Battery Disconnect Unit (BDU) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 自動車用バッテリーディスコネクトユニット市場の機会、成長促進要因、産業動向分析、2025~2034年の予測 |

|

出版日: 2024年12月09日

発行: Global Market Insights Inc.

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

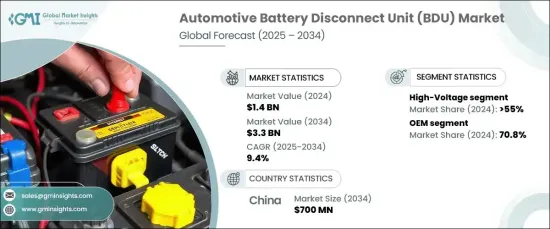

自動車用バッテリーディスコネクトユニットの世界市場規模は、2024年に14億米ドルとなり、2025年から2034年にかけてCAGR 9.4%の著しい成長が予測されています。

この成長を後押ししているのは、BDU技術の進歩、特にスマートモニタリングシステムの統合です。最新のBDUには最先端のセンサーとモノのインターネット(IoT)機能が搭載され、電圧、電流、温度のリアルタイム監視が可能となっています。こうした技術革新は車両の安全性と性能を大幅に向上させ、BDUを現代の自動車システムに不可欠なコンポーネントにしています。

新興市場における電気自動車(EV)の急速な普及は、高度なBDUの需要増加の主な促進要因となっています。各国が電動モビリティへの移行を加速させる中、費用対効果が高く、拡張性があり、気候変動に強いBDUのニーズが高まっています。世界各国の政府は、EV奨励策や充電インフラの急速な拡大など、支援政策によってこの勢いに拍車をかけています。このシフトは、多様な条件や環境で確実に動作するように設計されたBDUの需要をさらに際立たせています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 14億米ドル |

| 予測金額 | 33億米ドル |

| CAGR | 9.4% |

電圧別にセグメント化すると、市場は高電圧BDUと低電圧BDUで構成されます。高電圧BDUは、電気自動車とハイブリッド車における極めて重要な役割を反映し、2024年の市場シェアの55%を占めました。これらのBDUは、短絡などの電気的危険を防止して安全性を確保しながら、EVバッテリーシステムでエネルギーを管理・貯蔵するために重要です。安全規制が強化され、乗用車と商用車の両方で高性能バッテリーシステムへの注目が高まっていることから、高電圧BDUの需要は今後数年間で大幅な成長が見込まれています。

同市場はまた、流通チャネル別に相手先商標製品メーカー(OEM)とアフターマーケットに分類されます。2024年には、OEMが70.8%の市場シェアを占め、新車にBDUが標準部品として組み込まれていることがその要因となっています。OEMは、規模の経済を活用して高品質のBDUを競争力のある価格で提供し、高度な安全性と自動化技術に対する需要の高まりに対応しています。継続的な技術革新とサプライヤーとの戦略的提携により、BDU技術はさらに強化され、進化する規制基準や消費者の嗜好に沿ったものとなっています。

中国は自動車用BDU市場の強国として台頭しており、2034年までに7億米ドルに達すると予測されています。自動車製造の世界的リーダーである中国は、自動車メーカーがEV製品において安全性、エネルギー効率、性能を優先しているため、BDUの需要が急増しています。この地域の急速な都市化は、可処分所得の増加と相まって、自動車販売と先進的な自動車技術の採用を促進しており、BDU市場の今後の成長における重要なプレーヤーとしての中国の地位を確固たるものにしています。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 1次調査と検証

- 一次情報

- データマイニングソース

- 市場定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- OEMメーカー

- 部品サプライヤー

- 技術プロバイダー

- サービスプロバイダー

- エンドユーザー

- 利益率分析

- バッテリーディスコネクトユニット(BDU)の価格分析

- 特許分析

- 技術とイノベーションの展望

- 主要ニュースと取り組み

- 規制状況

- 影響要因

- 促進要因

- 新興国におけるEV市場の拡大

- スマートBDU技術の進歩

- ソリッドステートリレーの採用増加

- バッテリー管理システム(BMS)やエネルギー貯蔵ソリューションとBDUの統合

- 業界の潜在的リスク&課題

- 先進BDUの高コスト

- 設計と統合の複雑さ

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:電圧別、2021年~2034年

- 主要動向

- 高電圧

- 低電圧

第6章 市場推計・予測:車種別、2021年~2034年

- 主要動向

- 乗用車

- ハッチバック

- セダン

- SUV車

- 商用車

- 小型商用車(LCV)

- 大型商用車(HCV)

第7章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- OEM

- アフターマーケット

第8章 市場推計・予測:推進力別、2021年~2034年

- 主要動向

- ICE

- 電気自動車

- バッテリー電気自動車(BEV)

- プラグインハイブリッド車(PHEV)

- ハイブリッド電気自動車(HEV)

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- Aptiv

- Automotive Grade Linux

- Bosch

- Continental

- Denso

- Eaton

- Honeywell

- Johnson Controls

- Kyocera

- Lear

- Littelfuse

- Mitsubishi Electric

- Panasonic

- Schaeffler

- Sensata Technologies

- Siemens

- STMicroelectronics

- Valeo

- Vitesco Technologies

- ZF Friedrichshafen

The Global Automotive Battery Disconnect Unit Market was valued at USD 1.4 billion in 2024 and is forecasted to grow at a remarkable CAGR of 9.4% between 2025 and 2034. This growth is propelled by advancements in BDU technology, particularly the integration of smart monitoring systems. Modern BDUs are now equipped with cutting-edge sensors and Internet of Things (IoT) capabilities, enabling real-time monitoring of voltage, current, and temperature. These innovations significantly enhance vehicle safety and performance, making BDUs an indispensable component of modern automotive systems.

The surging adoption of electric vehicles (EVs) in emerging markets is a key driver behind the increasing demand for advanced BDUs. As nations accelerate their transition to electric mobility, the need for cost-effective, scalable, and climate-resilient BDUs is on the rise. Governments worldwide are fueling this momentum with supportive policies, including EV incentives and the rapid expansion of charging infrastructure. This shift further underscores the demand for BDUs engineered to operate reliably across diverse conditions and environments.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.4 Billion |

| Forecast Value | $3.3 Billion |

| CAGR | 9.4% |

Segmented by voltage, the market comprises high-voltage and low-voltage BDUs. High-voltage BDUs accounted for 55% of the market share in 2024, reflecting their pivotal role in electric and hybrid vehicles. These BDUs are critical for managing and storing energy in EV battery systems while ensuring safety by preventing electrical hazards such as short circuits. With stricter safety regulations and a growing focus on high-performance battery systems for both passenger and commercial vehicles, the demand for high-voltage BDUs is expected to witness substantial growth in the coming years.

The market is also categorized by distribution channel into original equipment manufacturers (OEMs) and the aftermarket. In 2024, OEMs dominated with a 70.8% market share, driven by the incorporation of BDUs as standard components in new vehicles. OEMs leverage economies of scale to deliver high-quality BDUs at competitive prices, meeting the rising demand for advanced safety and automation technologies. Continuous innovation and strategic collaborations with suppliers further enhance BDU technology, ensuring it aligns with evolving regulatory standards and consumer preferences.

China is emerging as a powerhouse in the automotive BDU market, projected to reach USD 700 million by 2034. As a global leader in automotive manufacturing, China is experiencing a surge in demand for BDUs as automakers prioritize safety, energy efficiency, and performance in their EV offerings. The region's rapid urbanization, coupled with increasing disposable incomes, is driving vehicle sales and the adoption of advanced automotive technologies, solidifying China's position as a key player in the BDU market's future growth.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 OEMs

- 3.2.2 Component suppliers

- 3.2.3 Technology providers

- 3.2.4 Service providers

- 3.2.5 End users

- 3.3 Profit margin analysis

- 3.4 Price analysis of Battery Disconnect Unit (BDU)

- 3.5 Patent analysis

- 3.6 Technology & innovation landscape

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Expansion of EV markets in emerging economies

- 3.9.1.2 Advances in smart BDU technologies

- 3.9.1.3 Rising adoption of solid-state relays

- 3.9.1.4 Integration of BDUs with battery management systems (BMS) and energy storage solutions.

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High costs of advanced BDUs

- 3.9.2.2 Complexity in design and integration

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Voltage, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 High voltage

- 5.3 Low voltage

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger vehicles

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 Light Commercial Vehicles (LCV)

- 6.3.2 Heavy Commercial Vehicles (HCV)

Chapter 7 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 OEM

- 7.3 Aftermarket

Chapter 8 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 ICE

- 8.3 Electric vehicles

- 8.3.1 Battery Electric Vehicles (BEVs)

- 8.3.2 Plug-in Hybrid Electric Vehicles (PHEVs)

- 8.3.3 Hybrid Electric Vehicles (HEVs)

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Aptiv

- 10.2 Automotive Grade Linux

- 10.3 Bosch

- 10.4 Continental

- 10.5 Denso

- 10.6 Eaton

- 10.7 Honeywell

- 10.8 Johnson Controls

- 10.9 Kyocera

- 10.10 Lear

- 10.11 Littelfuse

- 10.12 Mitsubishi Electric

- 10.13 Panasonic

- 10.14 Schaeffler

- 10.15 Sensata Technologies

- 10.16 Siemens

- 10.17 STMicroelectronics

- 10.18 Valeo

- 10.19 Vitesco Technologies

- 10.20 ZF Friedrichshafen