|

市場調査レポート

商品コード

1665034

自動車用フロント・リアファイジタルシールド市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Automotive Front and Rear Phygital Shield Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 自動車用フロント・リアファイジタルシールド市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2024年12月09日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

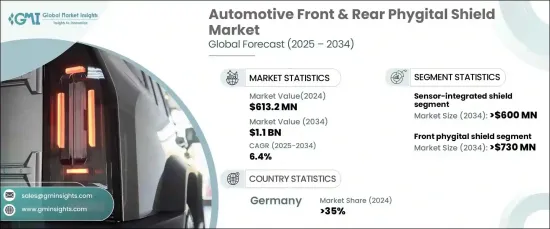

世界の自動車用フロント・リアファイジタルシールド市場は、2024年に6億1,320万米ドルと評価され、2025年から2034年にかけて6.4%のCAGRで堅調に成長すると予測されています。

ファイジタルシールドは、LiDAR、レーダー、カメラなどの最先端のセンサーシステムを統合する上で重要なコンポーネントとして浮上しており、自律走行車やコネクテッドカーのナビゲーション、通信、安全性にとって極めて重要です。これらのシールドは、車両の美観を維持しながらこれらの先端技術を組み込むために綿密に設計されており、機能的およびスタイル的な要求を満たしています。

市場は、製品タイプ別にフロントフィジタルシールドとリアフィジタルシールドに分類されます。2024年には、フロントフィジタルシールドが市場の65%を占め、大きなシェアを占めています。この分野は、電気自動車や高級車におけるLEDおよびディスプレイ対応フロントシールドの採用拡大により、2034年には7億3,000万米ドルに達すると予測されています。これらの先進的なシールドには、アダプティブ・ライティング・システムやデジタル・ディスプレイなどの機能が組み込まれており、動的なブランディング、シグナリング、コミュニケーション機能の強化などを実現します。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 6億1,320万米ドル |

| 予測金額 | 11億米ドル |

| CAGR | 6.4% |

技術面では、市場はセンサー一体型シールド、LED/ディスプレイシールド、空力シールドに分類されます。センサー一体型シールドは、2034年までに6億米ドルを創出すると予測されており、スマートシールド技術の急速な進歩を示しています。これらのシールドは現在、車両の中央システムに到達する前にセンサーデータを処理する前処理機能を備えています。分散処理を可能にすることで、待ち時間を大幅に短縮し、自律走行機能のリアルタイム意思決定を強化します。さらに、OTA(Over-the-Air)アップデートをサポートする機能は、エッジ・コンピューティングの重視の高まりに沿うもので、自動車メーカーがセンサー・アルゴリズムをリモートで改良し、継続的な性能向上を確保することを可能にします。

ドイツは、2024年の世界需要の35%を占め、大きなシェアを占めています。自動車技術革新の主要拠点であるドイツは、数多くの高級自動車メーカーの本拠地であり、先進的なファイジタル・シールドの採用を促進しています。これらのシールドは、車線維持支援、衝突回避、歩行者検知などの機能を提供するADAS(先進運転支援システム)に不可欠なセンサーやカメラを搭載する上で不可欠な役割を果たしています。自動車セクターにおける自動車の安全性と自律性への注目の高まりは、こうした技術的に洗練されたシールドの需要に引き続き拍車をかけています。

報告書の内容

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 1次調査と検証

- 一次情報

- データマイニングソース

- 市場定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- 部品メーカー

- ティア1サプライヤー

- 自動車OEM

- テクノロジー・インテグレーター

- エンドユーザー

- 利益率分析

- 技術差別化要因

- センサー統合

- LED照明およびディスプレイ・システム

- 空力設計の強化

- その他

- 主なニュースと取り組み

- 特許分析

- 規制状況

- 影響要因

- 促進要因

- 電気自動車の普及

- 自律走行車とコネクテッドカーの成長

- 自動車のパーソナライゼーションに対する消費者の需要の高まり

- 車体のエアロダイナミクスへの注目の高まり

- 業界の潜在的リスク&課題

- 高い開発コスト

- 複雑な製造プロセス

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- フロントフィジタルシールド

- リアフィジタルシールド

第6章 市場推計・予測:車両別、2021年~2034年

- 主要動向

- 乗用車

- ハッチバック

- セダン

- SUV車

- 商用車

- 小型商用車(LCV)

- 大型商用車(HCV)

第7章 市場推計・予測:技術別、2021年~2032年

- 主要動向

- センサー一体型シールド

- LED/ディスプレイ

- 空力

第8章 市場推計・予測:材料別、2021年~2032年

- 主要動向

- プラスチック/ポリマーベース

- 金属ベース

- コンポジット

第9章 市場推計・予測:販売チャネル別、2021年~2032年

- 主要動向

- OEM

- アフターマーケット

第10章 市場推計・予測:地域別、2021年~2032年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第11章 企業プロファイル

- Covestro

- Forvia Hella

- Harman

- Hyundai Mobis

- Infineon

- Intops

- Kia

- Magna

- Marelli

- Motherson

- Niebling

- Plastic Omnium

- Prolim

- Texas Instruments

- Valeo

The Global Automotive Front And Rear Phygital Shield Market was valued at USD 613.2 million in 2024 and is projected to grow at a robust CAGR of 6.4% from 2025 to 2034. Phygital shields have emerged as a critical component in the integration of cutting-edge sensor systems such as LiDAR, radar, and cameras, which are pivotal for the navigation, communication, and safety of autonomous and connected vehicles. These shields are meticulously designed to incorporate these advanced technologies while maintaining the vehicle's aesthetic appeal, meeting both functional and stylistic demands.

The market is segmented by product type into front phygital shields and rear phygital shields. In 2024, front phygital shields held the lion's share, accounting for 65% of the market. This segment is anticipated to reach USD 730 million by 2034, driven by the growing adoption of LED and display-enabled front shields in electric and luxury vehicles. These advanced shields incorporate features such as adaptive lighting systems and digital displays, which provide dynamic branding, signaling, and enhanced communication capabilities-key differentiators in modern automotive design.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $613.2 Million |

| Forecast Value | $1.1 Billion |

| CAGR | 6.4% |

On the technology front, the market is categorized into sensor-integrated shields, LED/display shields, and aerodynamic shields. Sensor-integrated shields are forecasted to generate USD 600 million by 2034, showcasing rapid advancements in smart shield technology. These shields now feature preprocessing capabilities that handle sensor data before it reaches the vehicle's central systems. By enabling distributed processing, they significantly reduce latency and enhance real-time decision-making for autonomous driving features. Furthermore, the ability to support over-the-air (OTA) updates aligns with the growing emphasis on edge computing, enabling automakers to refine sensor algorithms remotely and ensure continuous performance enhancements.

Germany represented a significant share of the market in 2024, accounting for 35% of the global demand. As a leading hub for automotive innovation, the country is home to numerous premium automotive manufacturers driving the adoption of advanced phygital shields. These shields play an integral role in housing sensors and cameras essential for Advanced Driver Assistance Systems (ADAS), which power features like lane-keeping assistance, collision avoidance, and pedestrian detection. The rising focus on vehicle safety and autonomy in the automotive sector continues to fuel the demand for these technologically sophisticated shields.

Report Content

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2032

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Component manufacturers

- 3.2.2 Tier-1 suppliers

- 3.2.3 Automotive OEM

- 3.2.4 Technology integrators

- 3.2.5 End users

- 3.3 Profit margin analysis

- 3.4 Technology differentiators

- 3.4.1 Sensor integration

- 3.4.2 LED lighting and display systems

- 3.4.3 Aerodynamic design enhancements

- 3.4.4 Others

- 3.5 Key news & initiatives

- 3.6 Patent analysis

- 3.7 Regulatory landscape

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Rise in electric vehicle adoption

- 3.8.1.2 Growth of autonomous and connected vehicles

- 3.8.1.3 Growing consumer demand for vehicle personalization

- 3.8.1.4 Growing focus on aerodynamics of vehicle body

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 High development costs

- 3.8.2.2 Complex manufacturing process

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter’s analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Front phygital shield

- 5.3 Rear phygital shield

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger vehicles

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 Light commercial vehicles (LCV)

- 6.3.2 Heavy commercial vehicles (HCV)

Chapter 7 Market Estimates & Forecast, By Technology, 2021 - 2032 ($Bn, Units)

- 7.1 Key trends

- 7.2 Sensor-integrated shield

- 7.3 LED/display

- 7.4 Aerodynamic

Chapter 8 Market Estimates & Forecast, By Material, 2021 - 2032 ($Bn, Units)

- 8.1 Key trends

- 8.2 Plastic/polymer-based

- 8.3 Metal-based

- 8.4 Composite

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2032 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2032 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Covestro

- 11.2 Forvia Hella

- 11.3 Harman

- 11.4 Hyundai Mobis

- 11.5 Infineon

- 11.6 Intops

- 11.7 Kia

- 11.8 Magna

- 11.9 Marelli

- 11.10 Motherson

- 11.11 Niebling

- 11.12 Plastic Omnium

- 11.13 Prolim

- 11.14 Texas Instruments

- 11.15 Valeo