|

市場調査レポート

商品コード

1892903

自動車用カーテンエアバッグ市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測Automotive Curtain Airbags Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 自動車用カーテンエアバッグ市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2025年12月09日

発行: Global Market Insights Inc.

ページ情報: 英文 225 Pages

納期: 2~3営業日

|

概要

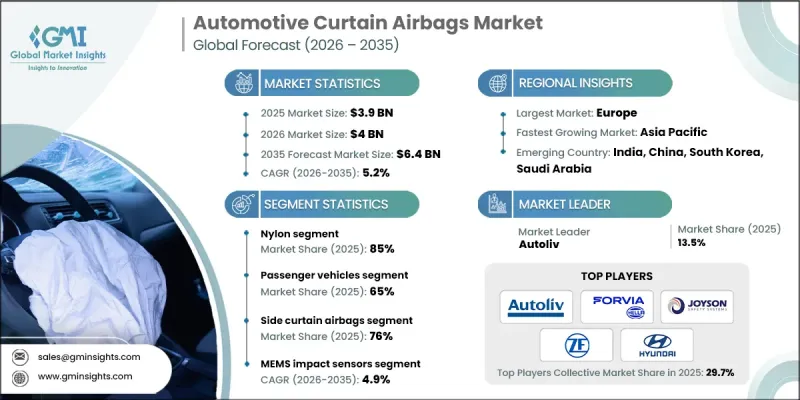

世界の自動車用カーテンエアバッグ市場は、2025年に39億米ドルと評価され、2035年までにCAGR 5.2%で成長し、64億米ドルに達すると予測されています。

SUVおよびクロスオーバー車の販売が着実に伸びていることが主な要因であり、キャビンの幅広化やルーフラインの高さが頭部保護システムの必要性を高めています。自動車メーカーは、カーテンエアバッグをより多くの車両に標準装備として順次導入しており、世界中で競争力のある価格で先進的な安全ソリューションを提供しています。EV用スケートボードプラットフォームの進化は車両構造を変革し、センサーや安全システムの配置方法に影響を与えています。この変化によりカーテンエアバッグの統合性が向上し、サプライヤーは軽量でコンパクトな膨張設計や、限られたキャビンスペースでも強力な保護性能を発揮する改良型繊維素材の開発を推進しています。複数の地域で規制が強化される中、OEMメーカーはほぼ全車種クラスにおいて側面衝突保護機能の提供が求められています。消費者の車両安全性への関心の高まりも、自動車メーカーに地域基準に準拠した先進的な受動安全システムによるラインナップの差別化を促しており、乗員保護を重視する購入者層への訴求力が高まっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 39億米ドル |

| 予測金額 | 64億米ドル |

| CAGR | 5.2% |

ナイロン素材セグメントは2025年に85%のシェアを占め、2035年までCAGR 4.2%で成長すると予測されています。ナイロン・ポリエステルハイブリッド、次世代ナイロン配合、バイオベースポリアミドの今後の開発により、性能向上と持続可能性目標の達成が期待されます。繊維化学の進歩により、ナイロンと代替素材の性能差は引き続き縮小しています。

乗用車セグメントは2025年に65%のシェアを占め、2026年から2035年にかけてCAGR 5.5%で成長すると予測されています。採用パターンは車種クラスによって異なります:高級車モデルではカーテンエアバッグシステムが広く採用されている一方、中級車では急速な統合が進んでいます。エントリーレベル市場では依然としてコスト制約がありますが、規制要件の強化と世界の消費者の安全意識の高まりに伴い、全体的な採用は増加傾向にあります。

米国自動車用カーテンエアバッグ市場は2025年に8億7,150万米ドルに達しました。規制当局は側面衝突および放出し防止試験の要件を拡大しており、メーカーに対し大型SUVやピックアップトラック向けに最適化された先進的なカーテンエアバッグの採用を促しています。これらの更新されたシステムは、従来の設計よりも広いカバー範囲と優れた横転時の性能を提供します。

よくあるご質問

目次

第1章 調査手法

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 乗員安全基準への適合性に対する重要性の高まり

- SUVおよびクロスオーバー車の普及拡大

- 適応型エアバッグシステムの技術的進歩

- 新興自動車拠点における生産拡大

- 持続可能な素材への移行

- 業界の潜在的リスク&課題

- 高いシステム統合性と部品コスト

- 新興市場における安全規制の不足

- 市場機会

- 自律走行車および準自律走行車の成長

- アフターマーケット向け交換部品およびリコールに伴う需要

- 商用車およびフリートへの拡大

- 持続可能性を重視した調達シフト

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 米国-FMVSS 214側面衝突保護

- カナダ-CMVSS 214側面衝突保護

- 欧州

- ドイツー国連規制135ポールサイド衝突保護装置

- 英国-UNECE規制95側面衝突保護

- フランス・EU一般安全規制 2019/2144

- イタリアー国連規制21室内装備の安全性

- スペイン-EU規制661/2009一般車両安全基準

- アジア太平洋地域

- 中国-GB 20071側面衝突保護

- インド-AIS-099側面衝突規制

- 日本-JNCAP側面衝突耐性試験プロトコル

- オーストラリア-ADR 72側面衝突保護

- 韓国-KMVSS側面衝突保護

- ラテンアメリカ

- ブラジル-Contran決議518側面衝突保護

- メキシコ-NOM-194-SCFI車両安全基準

- アルゼンチン-IRAM-AITA 1-20側面衝突基準

- 中東・アフリカ

- 南アフリカ-SANS 20079側面衝突保護

- サウジアラビア-SASO 2915車両安全規制

- UAE-UAE.S 5010-5車両衝突保護

- トルコ・UNECE規制95側面衝突保護装置

- 北米

- ポーター分析

- PESTEL分析

- 技術とイノベーションの動向

- 現行技術

- 新興技術

- 価格動向

- 製品別

- 地域別

- 生産統計

- 生産拠点

- 消費拠点

- 輸出入

- コスト内訳分析

- 特許分析

- 持続可能性と環境面

- 持続可能な取り組み

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に配慮した取り組み

- カーボンフットプリントに関する考慮事項

- 将来の市場見通しと機会

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ地域

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 事業拡大計画と資金調達

第5章 市場推計・予測:タイプ別、2022-2035

- サイドカーテンエアバッグ

- ナイロン

- ポリエステル

- フロントカーテンエアバッグ

- ナイロン

- ポリエステル

- リアカーテンエアバッグ

- ナイロン

- ポリエステル

第6章 市場推計・予測:材料別、2022-2035

- ナイロン

- ポリエステル

第7章 市場推計・予測:センサー別、2022-2035

- MEMS衝撃センサー

- ロールオーバージャイロセンサー

- 統合安全ECU

第8章 市場推計・予測:車両別、2022-2035

- 乗用車

- ハッチバック

- セダン

- SUV

- 商用車

- 小型商用車(LCV)

- 中型商用車(MCV)

- 大型商用車(HCV)

第9章 市場推計・予測:販売チャネル別、2021-2034

- OEM

- アフターマーケット

第10章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- ポルトガル

- クロアチア

- ベネルクス

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- シンガポール

- タイ

- インドネシア

- ベトナム

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ地域

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- トルコ

第11章 企業プロファイル

- 世界企業

- Autoliv

- ZF Friedrichshafen

- Joyson Safety Systems

- Continental

- Hyundai

- Toyoda Gosei

- Daicel

- Bosch Passive Safety Systems

- Magna International

- Denso

- Valeo

- Delphi Automotive/BorgWarner

- 地域メーカー

- Forvia Hella

- Kolon Industries

- Nihon Plast

- Porcher Industries

- Toray Industries

- Sumitomo

- SEIREN

- Toyota Boshoku

- Ashimori Industry

- U-Shin

- 新興・ニッチ企業

- Yanfeng Automotive Trim Systems

- Wuhu Ruili Automobile Airbag

- ARC Automotive

- Tata AutoComp Systems

- Ningbo Joyson Electronic

- Changzhou Changrui