|

市場調査レポート

商品コード

1664901

エンジン冷却用自動車用電動ウォーターポンプの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Automotive Electric Water Pump for Engine Cooling Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| エンジン冷却用自動車用電動ウォーターポンプの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2024年12月05日

発行: Global Market Insights Inc.

ページ情報: 英文 175 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

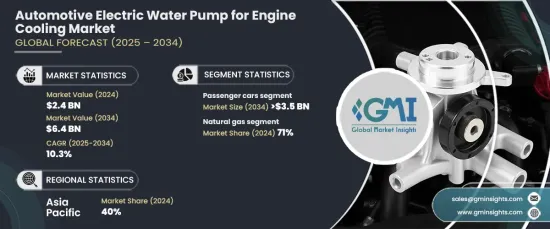

エンジン冷却用自動車用電動ウォーターポンプの世界市場は、2024年に24億米ドルとなり、2025年から2034年にかけて10.3%のCAGRで堅調に成長すると予測されています。

この成長の主な要因は、低燃費車に対する需要の急増です。世界各国の政府と消費者は、燃料消費を削減し環境への影響を軽減するためにエネルギー効率を重視する傾向を強めており、市場の大幅な拡大を牽引しています。

市場は車両タイプ別に商用車と乗用車に分類されます。2024年には、乗用車セグメントが全体の65%を占め、市場を独占しており、2034年までには35億米ドルに達すると予測されています。世界の排ガス規制の強化により、自動車メーカーは内燃機関(ICE)車に電動ウォーターポンプなどの高度な冷却ソリューションを採用する必要に迫られています。これらのポンプは、エンジン温度を最適に維持し、燃費を向上させ、エンジンストレスを軽減し、排出ガスを低減するために不可欠です。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 24億米ドル |

| 予測金額 | 64億米ドル |

| CAGR | 10.3% |

推進力タイプに基づき、市場は内燃機関車と電気自動車(EV)に分けられます。2024年には、ICEセグメントが71%の圧倒的な市場シェアを占めました。消費者が、より静かで、より効率的な車両と改良された機能を求めるようになるにつれ、電動ウォーターポンプの採用が勢いを増しています。これらのポンプは優れたエンジン冷却を実現するだけでなく、車内の暖房効率を高め、より快適でシームレスな運転体験を提供します。

アジア太平洋は最大の地域市場に浮上し、2024年には40%のシェアを占めました。中国やインドなど、自動車製造の主要拠点として知られる国々が、先進的なエンジン冷却技術の需要の先陣を切っています。この地域の自動車メーカーは、自動車の性能と効率に関する世界基準を満たすため、電動ウォーターポンプを内燃機関車と電気自動車モデルの両方に組み込んでいます。

補助金やインフラ整備を含む政府の取り組みにより、アジア太平洋ではEVの普及が加速しています。この急増は、EVの効果的な熱管理に不可欠な電動ウォーターポンプの需要を促進しています。世界最大のEV生産国である中国は、政府のインセンティブと急速に拡大する電気自動車の消費者層に支えられ、この成長において極めて重要な役割を果たしています。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 一次調査と検証

- 一次ソース

- データマイニングソース

- 市場範囲と定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム分析

- 原材料サプライヤー

- 部品サプライヤー

- メーカー

- 技術プロバイダー

- エンドユーザー

- サプライヤーの状況

- 利益率分析

- 技術とイノベーションの展望

- 特許分析

- 主要ニュース・イニシアチブ

- 規制状況

- 価格分析

- 影響要因

- 成長促進要因

- 電気自動車とハイブリッド車の普及

- 自動車の排出ガス削減と燃費向上に対する規制の注目の高まり

- 新興経済国における自動車生産の拡大

- 電動ウォーターポンプ設計の技術革新

- 業界の潜在的リスク・課題

- バッテリー性能への依存

- 電動ウォーターポンプを従来の自動車システムに組み込む際の初期コストの高さと複雑さ

- 成長促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業市場シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:電圧別、2021年~2034年

- 主要動向

- 12V

- 24V

第6章 市場推計・予測:推進力別、2021年~2034年

- 主要動向

- ICE

- ガソリン

- ディーゼル

- 電気自動車

- ハイブリッド電気自動車(HEV)

- バッテリー電気自動車(BEV)

- 燃料電池電気自動車

第7章 市場推計・予測:車両別、2021年~2034年

- 主要動向

- 乗用車

- セダン

- ハッチバック

- SUV車

- その他

- 商用車

- 小型商用車(LCV)

- 大型商用車(HCV)

第8章 市場推計・予測:販売チャネル別、2021年~2034年

- 主要動向

- OEM

- アフターマーケット

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- Aisin Seiki

- BLDC Pump

- Bosch

- Carter Fuel Systems

- Continental

- Cummins

- Davies Craig

- Denso

- Gates

- GMB Corporation

- Hanon

- Hitachi Automotive

- Mahle

- Mitsubishi Electric

- Rexroth

- Rheinmetall

- Schaeffler Technologies

- Shandong Boshan

- Valeo

- VOVYO Technology

The Global Automotive Electric Water Pump For Engine Cooling Market was valued at USD 2.4 billion in 2024 and is projected to grow at a robust CAGR of 10.3% from 2025 to 2034. This growth is primarily fueled by the surging demand for fuel-efficient vehicles. Governments and consumers worldwide are increasingly emphasizing energy efficiency to reduce fuel consumption and mitigate environmental impact, driving significant market expansion.

The market is categorized by vehicle type into commercial vehicles and passenger cars. In 2024, the passenger car segment dominated the market, accounting for 65% of the total share, and is projected to reach USD 3.5 billion by 2034. Stricter global emission regulations are compelling automakers to adopt advanced cooling solutions, such as electric water pumps, in internal combustion engine (ICE) vehicles. These pumps are critical for maintaining optimal engine temperatures, enhancing fuel efficiency, reducing engine stress, and lowering emissions-key factors in meeting rigorous environmental standards.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.4 Billion |

| Forecast Value | $6.4 Billion |

| CAGR | 10.3% |

Based on propulsion type, the market is divided into ICE and electric vehicles (EVs). In 2024, the ICE segment held a commanding 71% market share. As consumers increasingly demand quieter, more efficient vehicles with improved features, the adoption of electric water pumps has gained momentum. These pumps not only deliver superior engine cooling but also enhance cabin heating efficiency, offering a more comfortable and seamless driving experience.

Asia Pacific emerged as the largest regional market, holding a 40% share in 2024. Countries like China and India, recognized as major automotive manufacturing hubs, are spearheading the demand for advanced engine cooling technologies. Automakers in the region are integrating electric water pumps into both ICE and EV models to meet global standards for vehicle performance and efficiency.

Government initiatives, including subsidies and infrastructure development, are accelerating EV adoption in Asia Pacific. This surge is driving demand for electric water pumps, which are essential for effective thermal management in EVs. As the world's largest EV producer, China is playing a pivotal role in this growth, supported by government incentives and a rapidly expanding consumer base for electric vehicles.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material suppliers

- 3.1.2 Component suppliers

- 3.1.3 Manufacturers

- 3.1.4 Technology providers

- 3.1.5 End users

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Pricing analysis

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Rising adoption of electric and hybrid vehicles

- 3.9.1.2 Increasing regulatory focus on reducing vehicle emissions and improving fuel efficiency

- 3.9.1.3 Expansion of automotive production in emerging economies

- 3.9.1.4 Technological innovations in electric water pump design

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Dependence on battery performance

- 3.9.2.2 High initial costs and complexity in integrating electric water pumps into traditional automotive systems

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Voltage, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 12V

- 5.3 24V

Chapter 6 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 ICE

- 6.2.1 Gasoline

- 6.2.2 Diesel

- 6.3 Electric

- 6.3.1 Hybrid electric vehicles (HEVs)

- 6.3.2 Battery electric vehicles (BEVs)

- 6.3.3 Fuel cell electric vehicles

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.2.1 Sedans

- 7.2.2 Hatchbacks

- 7.2.3 SUVs

- 7.2.4 Others

- 7.3 Commercial vehicles

- 7.3.1 Light commercial vehicles (LCVs)

- 7.3.2 Heavy commercial vehicles (HCVs)

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Aisin Seiki

- 10.2 BLDC Pump

- 10.3 Bosch

- 10.4 Carter Fuel Systems

- 10.5 Continental

- 10.6 Cummins

- 10.7 Davies Craig

- 10.8 Denso

- 10.9 Gates

- 10.10 GMB Corporation

- 10.11 Hanon

- 10.12 Hitachi Automotive

- 10.13 Mahle

- 10.14 Mitsubishi Electric

- 10.15 Rexroth

- 10.16 Rheinmetall

- 10.17 Schaeffler Technologies

- 10.18 Shandong Boshan

- 10.19 Valeo

- 10.20 VOVYO Technology