|

市場調査レポート

商品コード

1664834

液浸冷却液の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Immersion Cooling Fluids Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 液浸冷却液の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2024年12月02日

発行: Global Market Insights Inc.

ページ情報: 英文 310 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

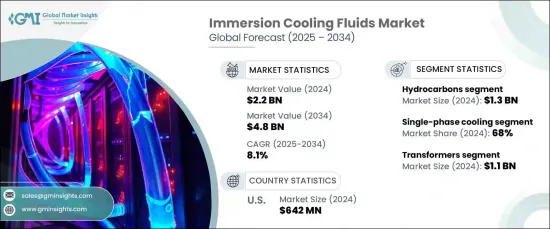

液浸冷却液の世界市場は、2024年に22億米ドルとなり、2025年から2034年にかけてCAGR8.1%で成長すると予測されています。

電子部品を水没させるように設計された液浸冷却液は、サーバー、変圧器、バッテリーなどの機器の熱を効率的に放散させるのに優れています。この技術は、優れた冷却性能とエネルギー効率で人気を集めています。

高性能システムにおけるエネルギー効率の高いソリューションに対する需要の高まりは、市場成長を促す重要な要因となっています。産業界が熱管理に関する課題に直面する中、液浸冷却は従来の冷却方法よりもコンパクトで効果的な代替手段を提供しています。さらに、熱伝導性と冷却効率を高める流体技術の進歩も、その採用を後押ししています。このような改良により、さまざまな産業でこれらの流体の利用可能性が広がり、持続可能で効率的な冷却ソリューションへの道が開かれます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 22億米ドル |

| 予測金額 | 48億米ドル |

| CAGR | 8.1% |

同市場は、流体タイプによって炭化水素とフルオロカーボンに分類されます。鉱物油と合成油を含む炭化水素は、2024年に13億米ドルを生み出し、優れた熱伝達能力とコスト優位性により、依然として好まれています。多様なシステム設計への適合性と環境への影響の低さが、その普及を後押ししています。フルオロカーボンはその安定性で注目を集めていますが、炭化水素はその総合的な性能の利点により優位性を維持しています。

技術的な観点から、市場は単相冷却と二相冷却に分けられます。単相冷却は、シンプルで信頼性が高く、メンテナンスの必要性が低いことから、2024年の市場シェアの68%を占めました。高性能アプリケーションで広く使用されていることから、重要な冷却ニーズに対応する有効性が浮き彫りになっています。二相冷却は、高熱負荷を管理するための高性能を提供しますが、単相システムは、その確立されたインフラにより、依然として好まれています。

用途別では、変圧器、データセンター、バッテリーなどの分野があります。変圧器は、2024年の売上高が11億米ドルで市場をリードしています。その冷却要件は、最適な機能性の維持と機器寿命の延長における浸漬型流体の役割を強調しています。産業界がますますエネルギー効率を優先するようになるにつれ、これらの流体に対する需要は様々な用途で拡大すると予想されます。

2024年には、米国が地域市場をリードし、6億4,200万米ドルの収益を獲得しました。同国は持続可能性を重視しており、インフラの進歩や産業需要の高まりと相まって、北米を液浸冷却技術の採用を促進する重要なプレーヤーとして位置付けています。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

- 一次

- 二次

- 有料情報源

- 公的情報源

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- 変革

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュース・取り組み

- 規制状況

- 影響要因

- 促進要因

- データセンターにおけるエネルギー効率の高い冷却ソリューションに対する需要の高まり

- 電気自動車(EV)バッテリーにおける液浸冷却技術の採用増加

- 熱伝導と冷却効率を高める流体技術の進歩

- 業界の潜在的リスク・課題

- 液浸冷却システムの初期コストと設備投資が高い

- データセンターと電気自動車(EV)バッテリー以外の産業での認知度と採用が限定的

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場規模・予測:流体タイプ別、2021年~2034年

- 主要動向

- 炭化水素

- 鉱物油

- 合成

- フルオロカーボン

第6章 市場規模・予測:技術別、2021年~2034年

- 主要動向

- 単相冷却

- 二相冷却

第7章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- 変圧器

- データセンター

- EVバッテリー

- その他

第8章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- 3M

- Cargill

- Chemie

- Chevron

- Dow

- Engineered Fluids

- Ergon

- ExxonMobil Chemical

- Shell

- Soltex

- Valvoline

The Global Immersion Cooling Fluids Market, valued at USD 2.2 billion in 2024, is anticipated to grow at a CAGR of 8.1% between 2025 and 2034. Immersion cooling fluids, designed to submerge electronic components, excel in efficiently dissipating heat from devices such as servers, transformers, and batteries. This technology is gaining traction for its superior cooling performance and energy efficiency.

Increasing demand for energy-efficient solutions in high-performance systems is a significant factor driving market growth. As industries face challenges related to heat management, immersion cooling offers a more compact and effective alternative to conventional cooling methods. Its adoption is further propelled by advancements in fluid technology that enhance thermal conductivity and cooling efficiency. These improvements broaden the usability of these fluids across multiple industries, paving the way for sustainable and efficient cooling solutions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.2 Billion |

| Forecast Value | $4.8 Billion |

| CAGR | 8.1% |

The market is categorized by fluid type into hydrocarbons and fluorocarbons. Hydrocarbons, including mineral oils and synthetic variants, generated USD 1.3 billion in 2024 and remain the preferred choice due to their superior heat transfer capabilities and cost advantages. Their compatibility with diverse system designs and lower environmental impact bolster their widespread use. While fluorocarbons are gaining attention for their stability, hydrocarbons maintain dominance due to their overall performance benefits.

From a technological standpoint, the market is divided into single-phase and two-phase cooling. Single-phase cooling captured 68% of the market share in 2024, thanks to its simplicity, reliability, and lower maintenance requirements. Its widespread use in high-performance applications highlights its effectiveness in addressing critical cooling needs. Although two-phase cooling offers enhanced performance for managing elevated heat loads, single-phase systems remain the favored choice due to their established infrastructure.

By application, the market includes segments such as transformers, data centers, and batteries. Transformers led the market in 2024 with USD 1.1 billion in revenue. Their cooling requirements emphasize the role of immersion fluids in maintaining optimal functionality and prolonging equipment life. As industries increasingly prioritize energy efficiency, demand for these fluids is expected to grow across various applications.

In 2024, the US led the regional market, earning USD 642 million in revenue. The country's emphasis on sustainability, coupled with advancements in infrastructure and growing industrial demands, positions North America as a key player in driving the adoption of immersion cooling technology.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Rising demand for energy-efficient cooling solutions in data centers

- 3.6.1.2 Increasing adoption of immersion cooling technology in electric vehicle (EV) batteries

- 3.6.1.3 Advancements in fluid technology enhancing heat transfer and cooling efficiency

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High initial cost and capital investment for immersion cooling systems

- 3.6.2.2 Limited awareness and adoption in industries outside data centers and EV batteries

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Size and Forecast, By Fluid Type, 2021-2034 (USD Billion, Metric Tons)

- 5.1 Key trends

- 5.2 Hydrocarbons

- 5.2.1 Mineral

- 5.2.2 Synthetic

- 5.3 Fluorocarbons

Chapter 6 Market Size and Forecast, By Technology, 2021-2034 (USD Billion, Metric Tons)

- 6.1 Key trends

- 6.2 Single-phase cooling

- 6.3 Two-phase cooling

Chapter 7 Market Size and Forecast, By Application, 2021-2034 (USD Billion, Metric Tons)

- 7.1 Key trends

- 7.2 Transformers

- 7.3 Data centre

- 7.4 EV batteries

- 7.5 Others

Chapter 8 Market Size and Forecast, By Region, 2021-2034 (USD Billion, Metric Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 3M

- 9.2 Cargill

- 9.3 Chemie

- 9.4 Chevron

- 9.5 Dow

- 9.6 Engineered Fluids

- 9.7 Ergon

- 9.8 ExxonMobil Chemical

- 9.9 Shell

- 9.10 Soltex

- 9.11 Valvoline