|

市場調査レポート

商品コード

1750532

燃料電池スタックの市場機会、成長促進要因、産業動向分析、2025~2034年予測Fuel Cell Stack Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 燃料電池スタックの市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年05月15日

発行: Global Market Insights Inc.

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

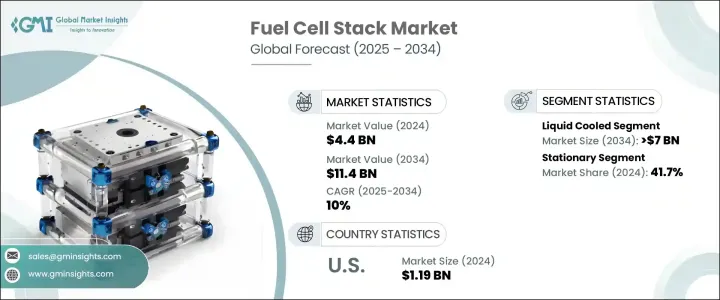

世界の燃料電池スタック市場は、2024年には44億米ドルと評価され、CAGR 10%で成長し、2034年には114億米ドルに達すると推定されています。

この成長の主な要因は、燃料電池を含む持続可能なエネルギー技術を支援する規制枠組みの施行が増加していることです。国家や産業界が気候変動と闘い、温室効果ガスの排出を抑制する取り組みを強化する中、燃料電池スタックは様々な用途で大きな支持を集めています。世界各国の政府は、税制優遇措置、補助金、研究イニシアティブを通じてクリーンエネルギーの導入を積極的に推進しており、市場成長にとって有利な環境を作り出しています。従来のエネルギー源が環境に与える影響に対する意識の高まりは、産業界にゼロエミッション解決策へのシフトを促しており、これが燃料電池技術の需要をさらに押し上げています。さらに、水素インフラの拡大や、特に高性能車や大型車の輸送手段への燃料電池の統合は、市場開発の新たな道を開くと期待されています。性能、コスト効率、拡張性の向上を目指した技術の進歩も、市場の勢いを加速させています。

燃料電池スタックの需要は、産業、商業、住宅の各分野でクリーンエネルギーの代替を継続的に推進していることに大きく影響されています。脱炭素化が戦略的優先事項となるにつれ、エネルギーシステムにおける燃料電池の役割は拡大しています。ハイブリッドセットアップをサポートし、グリッドの信頼性を向上させ、効率的なバックアップ電力を提供するその能力は、セクターを問わず魅力的な選択肢となっています。さらに、エネルギー企業、研究機関、メーカーを含む利害関係者間の協力が、製品イノベーションと展開を加速するのに役立っています。製造プロセスを合理化し、材料や生産技術の改善を通じてコストを削減する努力により、手頃な価格と入手しやすさが向上し、今後数年間で幅広い採用が可能になると予想されます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 44億米ドル |

| 予測金額 | 114億米ドル |

| CAGR | 10% |

製品タイプ別に見ると、市場は空冷式燃料電池スタックと液冷式燃料電池スタックに区分されます。2022年には38億米ドル、2023年には41億米ドル、2024年には44億米ドルを記録しました。このうち、液冷式セグメントは2034年までに70億米ドルを超えると予測されています。この成長の原動力となっているのは、燃料電池の高出力・高負荷用途での使用の増加と、高度な熱管理による性能向上です。液冷システムは、より安定した動作条件、より優れた熱放散、長寿命をサポートするため、安定した信頼性の高い出力が求められる分野に最適です。液冷システムの継続的な開発により、性能と耐久性が重要視される産業用および商業用バックアップシステムにますます適しています。

燃料電池スタック市場は、用途別に自動車、据置型、発電、その他に分類されます。2024年には、据置型セグメントが市場全体の41.7%を占め、最大のシェアを占めています。この優位性は、据置型燃料電池システムの進歩と、持続可能で分散型のエネルギー・ソリューションに対する需要の高まりに起因しています。産業界が二酸化炭素排出量の削減を目指す中、据置型燃料電池システムは、最小限の排出量でビルや工場、遠隔地の施設に電力を供給するために採用されています。また、再生可能エネルギー源との互換性により、エネルギー効率、信頼性、バックアップ機能を確保するハイブリッドシステムの構築もサポートされています。

地域別では、北米が2024年の世界燃料電池スタック市場で28.7%のシェアを占めています。米国だけの市場規模は、2022年に10億5,000万米ドル、2023年に11億1,000万米ドル、2024年に11億9,000万米ドルです。この地域の開発を支えているのは、水素充填インフラの整備と燃料電池自動車の導入拡大です。水素供給網の整備に官民が継続的に投資することで、同地域の市場はさらに強化され、北米は世界の燃料電池市場において重要な位置を占めると予想されます。

市場情勢の競合情勢は、既存企業と新興イノベーターによって特徴づけられます。主要企業5社(Plug Power社、Ballard Power Systems社、FuelCell Energy社、Bloom Energy社、Doosan Fuel Cell社)は、合計で市場シェア45%以上を占めています。有力企業が生産規模の拡大とシステム・コストの削減に注力する一方で、新興企業はニッチ・アプリケーションをターゲットとし、再生可能エネルギー技術との統合を模索しています。各社が製造効率の向上と代替材料の採用に努めるなか、費用対効果が高く拡張性の高い燃料電池ソリューションを提供するための競争が激化しています。戦略的投資、政府支援、クリーンエネルギー目標との整合は、市場力学を引き続き再構築し、業界全体の革新と競争を促しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略的取り組み

- 企業の市場シェア

- 企業ベンチマーク

- 戦略的ダッシュボード

- イノベーションとテクノロジーの情勢

第5章 市場規模・予測:タイプ別、2021 –2034

- 主要動向

- 空冷式

- 液冷式

第6章 市場規模・予測:容量別、2021 –2034

- 主要動向

- 5kW未満

- 5kW~100kW

- 100kW以上200kW以下

- 200kW以上

第7章 市場規模・予測:用途別、2021 –2034

- 主要動向

- 自動車

- 据置型

- 発電

- その他

第8章 市場規模・予測:地域別、2021 –2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オーストリア

- アジア太平洋地域

- 中国

- 日本

- 韓国

- インド

- フィリピン

- ベトナム

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- ラテンアメリカ

- ブラジル

- メキシコ

- ペルー

第9章 企業プロファイル

- Advent Technologies Holding

- Ballard Power Systems

- Commonwealth Automation Technologies

- Dana Incorporated

- ElringKlinger

- FuelCell Energy Solutions

- Freudenberg Group

- Horizon Fuel Cell Technologies

- Intelligent Energy Limited

- Nedstack Fuel Cell Technology

- Nuvera Fuel Cells

- PowerCell Sweden

- Plug Power

- Robert Bosch

- Schunk Bahn-und Industrietechnik

- TW Horizon Fuel Cell Technologies

The Global Fuel Cell Stack Market was valued at USD 4.4 billion in 2024 and is estimated to grow at a CAGR of 10% to reach USD 11.4 billion by 2034. This growth is largely fueled by the increasing enforcement of regulatory frameworks that support sustainable energy technologies, including fuel cells. As nations and industries intensify efforts to combat climate change and curb greenhouse gas emissions, fuel cell stacks are gaining significant traction across various applications. Governments around the world are actively promoting clean energy adoption through tax incentives, subsidies, and research initiatives, creating a favorable environment for market growth. Growing awareness of the environmental impact of conventional energy sources is prompting industries to shift toward zero-emission solutions, which is further bolstering the demand for fuel cell technology. Additionally, the expansion of hydrogen infrastructure and the integration of fuel cells into transportation-especially for high-performance and heavy-duty vehicles-are expected to create new avenues for market development. Technological advances aimed at improving performance, cost-efficiency, and scalability are also accelerating market momentum.

The demand for fuel cell stacks is heavily influenced by the continuous push for clean energy alternatives in the industrial, commercial, and residential sectors. As decarbonization becomes a strategic priority, the role of fuel cells in energy systems is expanding. Their ability to support hybrid setups, improve grid reliability, and provide efficient backup power makes them an attractive choice across sectors. Moreover, collaborations among stakeholders-including energy companies, research institutes, and manufacturers-are helping accelerate product innovation and deployment. Efforts to streamline manufacturing processes and reduce costs through improved materials and production techniques are expected to enhance affordability and accessibility, enabling broader adoption in the years ahead.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.4 Billion |

| Forecast Value | $11.4 Billion |

| CAGR | 10% |

In terms of product type, the market is segmented into air-cooled and liquid-cooled fuel cell stacks. The industry recorded USD 3.8 billion in 2022, USD 4.1 billion in 2023, and USD 4.4 billion in 2024. Among these, the liquid-cooled segment is projected to surpass USD 7 billion by 2034. This growth is being driven by the increasing use of fuel cells in high-power and intensive-duty applications, along with enhanced performance enabled by advanced thermal management. Liquid cooling systems support more stable operating conditions, better heat dissipation, and extended lifespan-making them ideal for sectors that demand consistent and reliable power output. The ongoing development of liquid-cooled systems is making them increasingly suitable for industrial and commercial backup systems where performance and durability are critical.

On the basis of application, the fuel cell stack market is categorized into automotive, stationary, power generation, and others. In 2024, the stationary segment held the largest share, accounting for 41.7% of the overall market. This dominance can be attributed to advancements in stationary fuel cell systems and the growing demand for sustainable and decentralized energy solutions. As industries seek to reduce their carbon footprints, stationary fuel cell systems are being adopted to power buildings, factories, and remote facilities with minimal emissions. Their compatibility with renewable energy sources also supports the creation of hybrid systems that ensure energy efficiency, reliability, and backup capabilities.

Regionally, North America held a 28.7% share of the global fuel cell stack market in 2024. The U.S. market alone was valued at USD 1.05 billion in 2022, USD 1.11 billion in 2023, and USD 1.19 billion in 2024. Growth in this region is supported by the development of hydrogen refueling infrastructure and increased deployment of fuel cell-powered vehicles. Continued public and private investment in building out hydrogen distribution networks is expected to strengthen the regional market further, positioning North America as a key player in the global fuel cell landscape.

The competitive landscape of the fuel cell stack market is marked by a combination of established companies and emerging innovators. The top five players- Plug Power, Ballard Power Systems, FuelCell Energy, Bloom Energy, and Doosan Fuel Cell-collectively contribute over 45% of the total market share. While dominant firms focus on scaling up production and reducing system costs, startups are targeting niche applications and exploring integration with renewable energy technologies. As companies strive to enhance manufacturing efficiency and adopt alternative materials, the race to provide cost-effective and scalable fuel cell solutions is intensifying. Strategic investments, government support, and alignment with clean energy goals continue to reshape market dynamics, encouraging innovation and competition throughout the industry.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Base estimates & calculations

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 – 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Trump administration tariff analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Strategic initiatives

- 4.3 Company market share

- 4.4 Company benchmarking

- 4.5 Strategic dashboard

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Type, 2021 – 2034 (USD Million & MW)

- 5.1 Key trends

- 5.2 Air Cooled

- 5.3 Liquid Cooled

Chapter 6 Market Size and Forecast, By Capacity, 2021 – 2034 (USD Million & MW)

- 6.1 Key trends

- 6.2 <5 kW

- 6.3 5 kW – 100 kW

- 6.4 >100 kW – 200 kW

- 6.5 >200 kW

Chapter 7 Market Size and Forecast, By Application, 2021 – 2034 (USD Million & MW)

- 7.1 Key trends

- 7.2 Automotive

- 7.3 Stationary

- 7.4 Power generation

- 7.5 Others

Chapter 8 Market Size and Forecast, By Region, 2021 – 2034 (USD Million & MW)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Austria

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 South Korea

- 8.4.4 India

- 8.4.5 Philippines

- 8.4.6 Vietnam

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Mexico

- 8.6.3 Peru

Chapter 9 Company Profiles

- 9.1 Advent Technologies Holding

- 9.2 Ballard Power Systems

- 9.3 Commonwealth Automation Technologies

- 9.4 Dana Incorporated

- 9.5 ElringKlinger

- 9.6 FuelCell Energy Solutions

- 9.7 Freudenberg Group

- 9.8 Horizon Fuel Cell Technologies

- 9.9 Intelligent Energy Limited

- 9.10 Nedstack Fuel Cell Technology

- 9.11 Nuvera Fuel Cells

- 9.12 PowerCell Sweden

- 9.13 Plug Power

- 9.14 Robert Bosch

- 9.15 Schunk Bahn-und Industrietechnik

- 9.16 TW Horizon Fuel Cell Technologies