|

|

市場調査レポート

商品コード

1620399

静止軌道リモートセンシング、画像、データサービス市場の市場機会、成長促進要因、産業動向分析、2024~2032年予測Geostationary Orbit (GEO) Remote Sensing, Imagery and Data Services Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2024 - 2032 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 静止軌道リモートセンシング、画像、データサービス市場の市場機会、成長促進要因、産業動向分析、2024~2032年予測 |

|

出版日: 2024年10月07日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

静止軌道(GEO)リモートセンシング、画像、データサービスの世界市場は、2023年に1億9,600万米ドルと評価され、2024~2032年までCAGR 17.6%で成長すると予測されています。

この成長の主因は、高解像度画像とデータ分析に対するニーズの高まりです。組織が意思決定のために正確なデータにますます依存するようになるにつれて、先進的な衛星ベースのソリューションへのニーズは拡大し続けています。衛星技術の進歩がGEOリモートセンシング市場を再形成しています。小型化、推進力、センサーシステムの改善により、高解像度の画像を低コストで撮影できる、より小型で手頃な衛星の開発が可能になりました。

こうした技術革新は、より頻繁なデータ収集を容易にし、分析の精度を高め、衛星サービスをより効率的で利用しやすいものにしています。市場はサービスタイプ別に画像とデータ分析に区分されます。画像セグメントはCAGR17.5%と最も速い成長が見込まれます。高解像度の衛星画像は、都市計画、環境モニタリング、災害管理などの用途に不可欠です。

土地利用のモニタリング、天然資源の追跡、危機発生時の被害評価に不可欠なデータを提供するため、業務上洞察力を高めたい政府や企業にとって不可欠なツールとなっています。産業別では、GEOリモートセンシング市場は、農業、林業、鉱業、エンジニアリング、エネルギー、環境モニタリング、海運、運輸、航空宇宙・防衛などのセグメントにサービスを提供しています。2023年には、航空宇宙・防衛セグメントが35.5%以上で最大の市場シェアを占めました。戦略的計画、モニタリング、偵察のためのGEO衛星サービスの利用は、軍事・防衛活動における状況認識の強化に不可欠であり、特にリアルタイムのモニタリング機能が重要です。

| 市場範囲 | |

|---|---|

| 開始年 | 2023年 |

| 予測年 | 2024~2032年 |

| 開始金額 | 1億9,600万米ドル |

| 予測金額 | 7億9,250万米ドル |

| CAGR | 17.6% |

2023年の世界市場は、北米がシェアの41%以上を占め、圧倒的な強さを見せた。この地域、特に米国は、政府の支援イニシアティブと強力な商業投資に牽引され、予測期間を通じて主導権を維持すると見られています。米国では衛星画像が国家安全保障、環境保護、災害対応に幅広く利用されており、市場成長をさらに後押ししています。農業、都市開発、気候モニタリングなどのセグメントで地理空間データが求められる中、米国はこのダイナミックなセグメントにおける技術革新の最前線にあり続けています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 産業洞察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- 変革

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュース

- 規制状況

- 影響要因

- 促進要因

- 世界の接続需要の急増

- 衛星技術における最先端のイノベーション

- 正確な気象予報へのニーズの高まり

- 新興技術との相乗効果

- 比類のないカバレッジとサービス品質

- 産業の潜在的リスク・課題

- スペクトル混雑の課題

- 高額な設備投資と長期的コミットメント

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

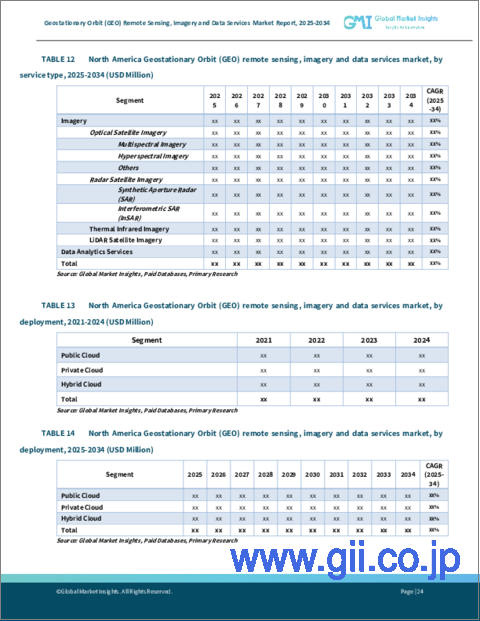

第5章 市場推定・予測:サービスタイプ別、2021~2032年

- 主要動向

- 画像

- 光学衛星画像

- マルチスペクトル画像

- ハイパースペクトル画像

- その他

- レーダー衛星画像

- 合成開口レーダー(SAR)

- 干渉SAR(InSAR)

- 熱赤外画像

- LiDAR衛星画像

- 光学衛星画像

- データ分析サービス

第6章 市場推定・予測:2021~2032年、展開別

- 主要動向

- パブリッククラウド

- プライベートクラウド

- ハイブリッドクラウド

第7章 市場推定・予測:産業別、2021~2032年

- 主要動向

- 農業

- エンジニアリング&インフラ

- エネルギー・電力

- 環境・気象

- 海運

- 輸送・物流

- 防衛

- その他

第8章 市場推定・予測:最終用途別、2021~2032年

- 主要動向

- 商業

- 政府・軍需

- 軍事・防衛

- 非国防機関

- 科学・学術研究

第9章 市場推定・予測:地域別、2021~2032年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Airbus Defence and Space

- BAE Systems

- China Aerospace Science and Technology Corporation

- Exolaunch

- GomSpace

- Lockheed Martin

- Maxar Technologies

- Millennium Space Systems

- Mitsubishi Electric

- Northrop Grumman

- OHB

- OneWeb

- Sierra Nevada

- SpaceX

- Thales Alenia Space

The Global Geostationary Orbit (GEO) Remote Sensing, Imagery And Data Services Market was valued at USD 196 million in 2023 and is projected to grow at 17.6% CAGR from 2024 to 2032. This growth is driven primarily by the rising need for high-resolution images and data analytics. As organizations increasingly rely on precise data for decision-making, the need for advanced satellite-based solutions continues to expand. Advancements in satellite technology are reshaping the GEO remote sensing market. Improvements in miniaturization, propulsion, and sensor systems have enabled the development of smaller, more affordable satellites capable of capturing high-resolution images at reduced costs.

These technological innovations facilitate more frequent data collection and enhance the precision of analytics, making satellite services more efficient and accessible. The market is segmented by service type into imagery and data analytics. The imagery segment is expected to see the fastest growth, with a CAGR of 17.5%. High-resolution satellite imagery is crucial for applications like urban planning, environmental monitoring, and disaster management.

It provides essential data for monitoring land use, tracking natural resources, and assessing damage during crises, making it an indispensable tool for governments and businesses looking to improve their operational insights. In terms of industry verticals, the GEO remote sensing market serves sectors such as agriculture, forestry, mining, engineering, energy, environment monitoring, maritime, transport, and aerospace & defense. In 2023, the aerospace and defense segment held the largest market share at over 35.5%. The use of GEO satellite services for strategic planning, surveillance, and reconnaissance is vital for enhancing situational awareness in military and defense operations, especially with real-time monitoring capabilities.

| Market Scope | |

|---|---|

| Start Year | 2023 |

| Forecast Year | 2024-2032 |

| Start Value | $196 Million |

| Forecast Value | $792.5 Million |

| CAGR | 17.6% |

North America dominated the global market in 2023, accounting for more than 41% of the share. This region, particularly the U.S., is expected to maintain its leadership throughout the forecast period, driven by government-backed initiatives and strong commercial investments. Satellite imagery is extensively used for national security, environmental protection, and disaster response in the U.S., further driving market growth. As sectors like agriculture, urban development, and climate monitoring demand geospatial data, the U.S. remains at the forefront of innovation in this dynamic field.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2032

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Surge in global connectivity demand

- 3.6.1.2 Cutting-edge innovations in satellite technology

- 3.6.1.3 Escalating need for precise weather forecasting

- 3.6.1.4 Synergy with emerging technologies

- 3.6.1.5 Unmatched coverage and service quality

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Spectrum congestion challenges

- 3.6.2.2 High capital investment and long-term commitment

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2023

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Service Type, 2021-2032 (USD Million)

- 5.1 Key trends

- 5.2 Imagery

- 5.2.1 Optical satellite imagery

- 5.2.1.1 Multispectral imagery

- 5.2.1.2 Hyperspectral imagery

- 5.2.1.3 Others

- 5.2.2 Radar satellite imagery

- 5.2.2.1 Synthetic Aperture Radar (SAR)

- 5.2.2.2 Interferometric SAR (InSAR)

- 5.2.3 Thermal infrared imagery

- 5.2.4 LiDAR satellite imagery

- 5.2.1 Optical satellite imagery

- 5.3 Data analytics services

Chapter 6 Market Estimates & Forecast, By Deployment, 2021-2032 (USD Million)

- 6.1 Key trends

- 6.2 Public cloud

- 6.3 Private cloud

- 6.4 Hybrid cloud

Chapter 7 Market Estimates & Forecast, By Industry Vertical, 2021-2032 (USD Million)

- 7.1 Key trends

- 7.2 Agriculture

- 7.3 Engineering & infrastructure

- 7.4 Energy & power

- 7.5 Environment & weathers

- 7.6 Maritime

- 7.7 Transport & logistics

- 7.8 Defense

- 7.9 Others

Chapter 8 Market Estimates & Forecast, By End Use, 2021-2032 (USD Million)

- 8.1 Key trends

- 8.2 Commercial

- 8.3 Government and military

- 8.3.1 Military & defense

- 8.3.2 Non-Defense organization

- 8.4 Scientific and academic research

Chapter 9 Market Estimates & Forecast, By Region, 2021-2032 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Airbus Defence and Space

- 10.2 BAE Systems

- 10.3 China Aerospace Science and Technology Corporation

- 10.4 Exolaunch

- 10.5 GomSpace

- 10.6 Lockheed Martin

- 10.7 Maxar Technologies

- 10.8 Millennium Space Systems

- 10.9 Mitsubishi Electric

- 10.10 Northrop Grumman

- 10.11 OHB

- 10.12 OneWeb

- 10.13 Sierra Nevada

- 10.14 SpaceX

- 10.15 Thales Alenia Space