|

市場調査レポート

商品コード

1892819

前立腺がん診断市場機会、成長要因、業界動向分析、および2026年から2035年までの予測Prostate Cancer Diagnostics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 前立腺がん診断市場機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2025年12月15日

発行: Global Market Insights Inc.

ページ情報: 英文 140 Pages

納期: 2~3営業日

|

概要

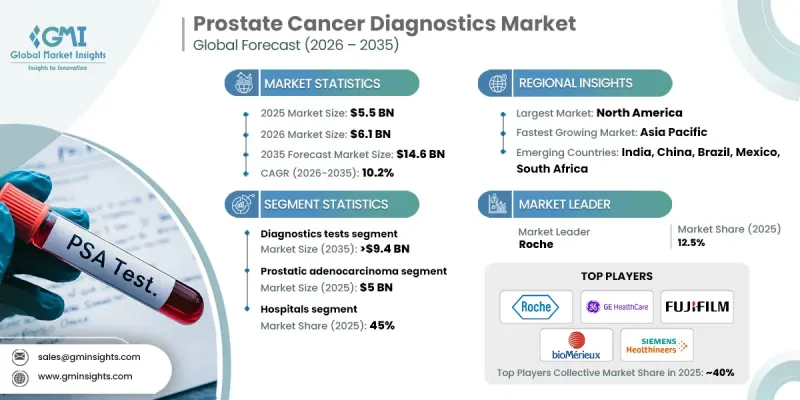

世界の前立腺がん診断市場は、2025年に55億米ドルと評価され、2035年までにCAGR10.2%で成長し、146億米ドルに達すると予測されています。

この成長は、診断技術の継続的な進歩、世界の前立腺がんの負担増加、啓発活動の拡大、スクリーニングプログラムの拡充、そして急速に進む男性人口の高齢化によって牽引されています。前立腺がん診断とは、疾患の検出、進行の評価、治療方針の決定を支援するために用いられる包括的な臨床検査および医療処置を指します。これらの診断には、血液検査、高度な画像診断技術、組織分析法など、正確な疾患の特定と経過観察を支える手法が含まれます。次世代シーケンシング、液体ベース診断アプローチ、多パラメトリック画像診断、AI支援分析ツールなどの近年の技術進歩により、診断精度が大幅に向上すると同時に、不必要な介入が減少しています。業界は、より正確で侵襲性の低い診断経路への移行、および分子・ゲノムプロファイリングへの依存度の高まりから引き続き恩恵を受けており、これらによって医療現場全体で早期発見率と臨床的意思決定が改善されています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測期間 | 2026-2035 |

| 開始時価値 | 55億米ドル |

| 予測金額 | 146億米ドル |

| CAGR | 10.2% |

診断検査セグメントは2025年に63.6%のシェアを占めました。この主導的な地位は、スクリーニング検査やバイオマーカー検査の利用増加、早期発見への志向の高まり、非侵襲的診断法の普及を反映しています。疾患の有病率の上昇と患者意識の向上により、信頼性が高く正確な検査ソリューションへの需要は引き続き堅調に推移しています。

病院セグメントは2025年に45%のシェアを占め、2025年から2035年の間に64億米ドルに達すると予測されています。病院は、初期患者評価、高度な画像診断、確定検査における役割から、前立腺がん診断の中心的存在であり続けています。統合された診断能力は、単一の医療環境内での包括的な疾患評価と病期分類を支援します。

北米前立腺がん診断市場は2025年に40.4%のシェアを占めました。高い疾患発生率、確立されたスクリーニング慣行、先進的な医療インフラが、この地域の堅調な業績を支えています。設備の整った診断施設と早期発見イニシアチブの存在が、地域全体での先進的診断技術の採用を継続的に推進しています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 前立腺がんの増加傾向

- 画像診断およびバイオマーカーに基づく診断技術の進歩

- 高まる意識とスクリーニング施策

- 低侵襲診断手技に対する需要の拡大

- 業界の潜在的リスク&課題

- 高度な診断モダリティの高コスト

- 低・中所得地域における限られたアクセス可能性

- 市場機会

- AIを活用した診断ツールの拡大

- 個別化医療の導入拡大

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- 技術動向

- 現在の技術動向

- 新興技術

- 償還シナリオ

- 将来の市場動向

- バリューチェーン分析

- ポーター分析

- PESTEL分析

- ギャップ分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業の市場シェア分析

- 世界

- 北米

- 欧州

- アジア太平洋地域

- 競合ポジショニングマトリックス

- 主要市場企業の競合分析

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 拡大計画

第5章 市場推計・予測:テストタイプ別、2022-2035

- 主要動向

- 診断検査

- PSA

- 前立腺生検

- 分子・ゲノム検査

- その他の診断検査

- 画像検査

- 経直腸的超音波検査(TRUS)

- MRI

- CTスキャン

- その他の画像検査

第6章 市場推計・予測:がん種別、2022-2035

- 主要動向

- 前立腺腺がん

- 小細胞がん

- その他のがん種

第7章 市場推計・予測:最終用途別、2022-2035

- 主要動向

- 病院

- 診断検査室

- がん研究機関

- その他の用途

第8章 市場推計・予測:地域別、2022-2035

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Abbott

- Beckman Coulter

- Becton, Dickinson and Company

- bioMerieux

- FUJIFILM

- GE HealthCare

- Glycanostics

- HEALGEN

- KOELIS

- Metamark Genetics

- Myriad Genetics

- OPKO Health

- PHILIPS

- Proteomedix

- Roche

- SIEMENS Healthineers

- Veracyte