|

市場調査レポート

商品コード

1892808

眼科用縫合糸市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測Ophthalmic Sutures Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 眼科用縫合糸市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2025年12月10日

発行: Global Market Insights Inc.

ページ情報: 英文 160 Pages

納期: 2~3営業日

|

概要

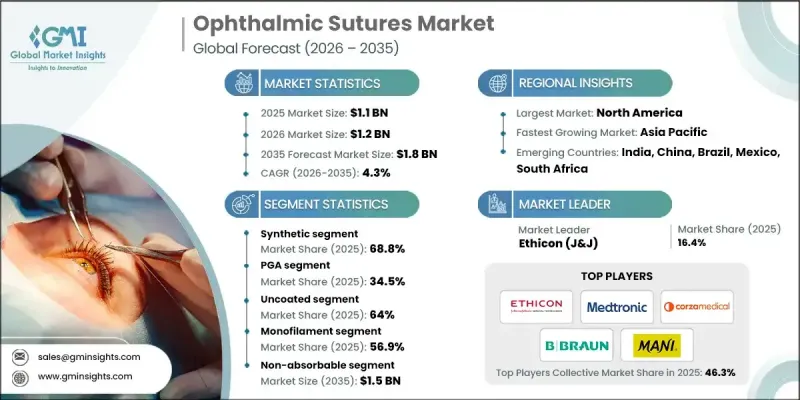

世界の眼科用縫合糸市場は、2025年に11億米ドルと評価され、2035年までにCAGR4.3%で成長し、18億米ドルに達すると予測されています。

市場拡大の主な要因としては、眼科手術件数の増加、高齢化社会の進展、技術革新、眼疾患の有病率上昇に加え、質の高い医療へのアクセス拡大が挙げられます。眼科用縫合糸は、病院、専門眼科クリニック、外来手術センターに重要な外科的ソリューションを提供し、白内障、角膜、緑内障、網膜手術における患者様の治療成果、精密な創傷管理、手術効率の向上に貢献しております。高度な吸収性および非吸収性の選択肢を含むこれらの縫合糸は、優れた操作性、最小限の組織損傷、信頼性の高い術後治癒を実現するよう設計されており、眼科医が繊細な手術をより高い精度と安全性で行えるようにいたします。顕微手術技術の進歩と、外来・日帰り眼科手術への移行動向の高まりにより、炎症を軽減し、治癒を促進し、予測可能な回復結果をもたらす縫合糸への需要が増加しています。新興国における医療インフラの拡充と医療費の増加も、矯正眼科手術への患者アクセスを改善し、市場の持続的な成長を支えています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 11億米ドル |

| 予測金額 | 18億米ドル |

| CAGR | 4.3% |

合成縫合糸セグメントは、高い引張強度、予測可能な吸収性、そして臨床現場での広範な採用により、2025年に68.8%のシェアを占めました。ポリグラクチン、ポリグリコール酸、ポリジオキサノンなどの素材で構成される合成縫合糸は、組織反応性が低く、感染や炎症のリスクも最小限であるため、繊細な眼科手術に非常に適しています。

PGAセグメントは、生分解性と優れた引張強度により、2025年に34.5%のシェア(6億700万米ドル相当)を占めました。PGA縫合糸は体内での段階的な分解により抜糸が不要となり、患者の不快感を軽減し、特に小児および高齢者患者における通院回数を最小限に抑えます。

北米眼科用縫合糸市場は、先進的な医療インフラ、高い医療支出、眼疾患の増加傾向に支えられ、2025年に38.1%のシェアを占めました。同地域には、白内障、緑内障、網膜手術を多数実施する病院、外来手術センター、専門眼科クリニックの広範なネットワークが存在し、眼科用縫合糸の持続的な需要を保証しています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 眼疾患の増加傾向

- 技術的進歩

- 糖尿病の有病率上昇に伴う眼科疾患の増加

- 政府による有利な施策

- 低侵襲手術に対する需要と選好の高まり

- 業界の潜在的リスク&課題

- 眼科手術に伴う術後合併症

- 熟練した眼科医の不足

- 市場機会

- 特殊縫合糸および高級縫合糸の採用拡大

- 眼科医療インフラの改善に伴う新興市場での拡大

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- 技術的進歩

- 現在の技術動向

- 精密設計された縫合針と縫合糸の組み合わせ

- プリロード済み・即使用可能な縫合キット

- 低侵襲マイクロ外科縫合技術

- 新興技術

- 生体吸収性縫合糸およびコーティング縫合糸

- 高度なポリマーおよび複合材料

- スマート外科用器具およびロボット支援縫合

- 現在の技術動向

- ギャップ分析

- ポーター分析

- PESTEL分析

- 将来の市場動向

- デジタル手術計画とAI支援マイクロ外科手術の統合

- バイオエンジニアリングおよび薬剤溶出型縫合糸の開発

- 眼科医療インフラが発展する新興市場における拡大

第4章 競合情勢

- イントロダクション

- 企業マトリクス分析

- 企業の市場シェア分析

- 世界

- 北米

- 欧州

- アジア太平洋地域

- 競合ポジショニングマトリックス

- 主要市場企業の競合分析

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 拡大計画

第5章 市場推計・予測:タイプ別、2022-2035

- 主要動向

- 天然

- 合成

第6章 市場推計・予測:材料別、2022-2035

- 主要動向

- PGA

- ナイロン

- シルク

- ポリプロピレン

- その他の素材

第7章 市場推計・予測:コーティング別、2022-2035

- 主要動向

- コーティング済み

- 無塗装

第8章 市場推計・予測:素材構造別、2022-2035

- 主要動向

- モノフィラメント

- マルチフィラメント/編組

第9章 市場推計・予測:吸収性別、2022-2035

- 主要動向

- 吸収性

- 非吸収性

第10章 市場推計・予測:用途別、2022-2035

- 主要動向

- 白内障手術

- 角膜移植手術

- 緑内障手術

- 硝子体切除術

- 眼形成外科

- その他の用途

第11章 市場推計・予測:最終用途別、2022-2035

- 主要動向

- 病院

- 外来手術センター

- その他の用途

第12章 市場推計・予測:地域別、2022-2035

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第13章 企業プロファイル

- Alcon

- Assut Medical

- Aurolab

- Accutome

- B Braun

- Corza Medical

- DemeTECH

- Ethicon

- FCI Ophthalmics

- Geuder AG

- Mani

- Medtronic

- Teleflex Incorporated

- Unilene