|

市場調査レポート

商品コード

1782146

高圧電気コンデンサの市場機会、成長促進要因、産業動向分析、2025~2034年予測High Voltage Electric Capacitor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 高圧電気コンデンサの市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年07月14日

発行: Global Market Insights Inc.

ページ情報: 英文 141 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

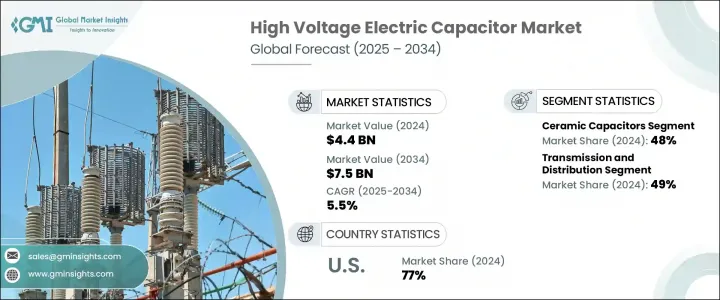

高圧電気コンデンサの世界市場規模は、2024年に44億米ドルとなり、CAGR 5.5%で成長し、2034年には75億米ドルに達すると予測されています。

この市場は、送電、配電システム、エネルギー貯蔵、力率補正を含む幅広い用途でこれらの部品への依存度が高まっているため、世界的に牽引力を増しています。高圧コンデンサは、安定した電圧制御を確保し、送電網の効率を高め、送電損失を最小限に抑えるために不可欠なものとなっています。電力ネットワークが太陽光、風力、水力などの再生可能エネルギー源をますます統合するにつれて、先進的なコンデンサソリューションへの需要が加速しています。これらのデバイスは、高い耐久性、耐熱性、高電圧性能を備えており、105℃を超えて動作する厳しい商業・産業環境に最適です。

メーカー各社はまた、スペースに制約のある過酷な動作条件下で優れた効率を実現するコンパクト設計にも注力しています。これらの技術革新は、性能を損なうことなく電気システム全体の設置面積を縮小し、システム・アーキテクチャやレイアウトの柔軟性を高めることを目的としています。コンパクトな高圧コンデンサは、モジュール式グリッドコンポーネント、移動式変電所、オフショアプラットフォームなど、スペースと熱管理が重要な高需要環境において特に有益です。サイズ対キャパシタンス比を最適化することで、各社はエンジニアやユーティリティプロバイダーがこれらのソリューションを高度なパワーエレクトロニクスや再生可能エネルギー設備に統合しやすくしています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 44億米ドル |

| 予測金額 | 75億米ドル |

| CAGR | 5.5% |

フィルムコンデンサ分野は2034年までに21億米ドルに達し、CAGR 5.4%で成長します。フィルムコンデンサが広く使用されているのは、長寿命、熱安定性、低インダクタンスによるもので、エネルギーエレクトロニクスのフィルタリング、電力補正、サージ吸収に高い信頼性をもたらしています。エネルギー転換の動向が続く中、フィルムコンデンサはクリーンエネルギーシステム、特に太陽光発電や風力発電のグリッド統合用インバータやコンバータにおいて、電力の流れを管理する上で重要なコンポーネントとなりつつあります。

送電・配電分野は2024年に49%のシェアを占め、2034年までのCAGRは5.2%と予測されています。送電網の効率化と長距離での安定した電力供給への注目が高まる中、高性能コンデンサへの需要が高まっています。これらの部品は、広大な送電インフラの電圧安定性を確保する上で重要な役割を担っており、特に開発途上地域や、電力需要の増加と広い地域スパンをサポートするために超高電圧(UHV)システムや超高電圧(EHV)システムを拡張している国々で重要な役割を果たしています。

米国の高圧電気コンデンサ市場は2024年に77%のシェアを占め、6億5,000万米ドルを生み出します。成長の主因は、老朽化した電力網を近代化し、よりクリーンなエネルギー源の統合を拡大するための継続的な取り組みです。米国中の公益事業者は、無効電力を管理し、電圧の安定性を向上させ、変動するエネルギー負荷に対応して送電網の回復力を強化するために、堅牢なコンデンサ技術に多額の投資を行っています。

同市場で活躍する主要企業には、Kemet, Murata, Panasonic, ABB, and Cornell Dubilier.などがあります。市場でのポジショニングを強化するため、高圧電気コンデンサセクターの企業は、製品イノベーション、戦略的パートナーシップ、地理的拡大に注力しています。再生可能エネルギーの統合とスマートグリッドの近代化におけるアプリケーションをサポートするため、より高い耐熱性、より優れたエネルギー密度、より長い寿命を持つ先進的なコンデンサ技術の開発に重点が置かれています。企業はまた、産業および公益事業部門における進化する顧客需要に対応する、スペース効率の高い高性能製品を製造するための研究開発にも投資しています。各地域に製造ユニットやサービスセンターを設立することで、納期の短縮や地域密着型のサポートが可能になります。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 戦略ダッシュボード

- 戦略的取り組み

- 競合ベンチマーキング

- イノベーションとテクノロジーの情勢

第5章 市場規模・予測:材料別、2021年~2034年

- 主要動向

- フィルムコンデンサ

- セラミックコンデンサ

- 電解コンデンサ

- その他

第6章 市場規模・予測:最終用途別、2021年~2034年

- 主要動向

- 家電

- 自動車

- 通信・技術

- 送電・配電

- その他

第7章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- フランス

- ドイツ

- イタリア

- オーストリア

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- クウェート

- ラテンアメリカ

- ブラジル

- アルゼンチン

- チリ

第8章 企業プロファイル

- ABB

- Cornell Dubilier

- Elna

- Havells

- Kemet

- Kyocera AVX

- Murata Manufacturing

- Panasonic

- Samsung Electro-Mechanics

- Schneider Electric

- Siemens

- Taiyo Yuden

- TDK

- Vishay Intertechnology

The Global High Voltage Electric Capacitor Market was valued at USD 4.4 billion in 2024 and is estimated to grow at a CAGR of 5.5% to reach USD 7.5 billion by 2034. This market is gaining traction worldwide due to the growing reliance on these components for a wide range of uses, including power transmission, distribution systems, energy storage, and power factor correction. High-voltage capacitors have become indispensable for ensuring consistent voltage regulation, enhancing grid efficiency, and minimizing transmission losses. As power networks increasingly integrate renewable sources like solar, wind, and hydro, demand for advanced capacitor solutions is accelerating. These devices offer high durability, heat resistance, and elevated voltage performance, making them ideal for demanding commercial and industrial environments operating beyond 105°C.

Manufacturers are also focusing on compact designs that deliver superior efficiency in space-constrained and extreme operational conditions. These innovations aim to reduce the overall footprint of electrical systems without compromising performance, allowing for greater flexibility in system architecture and layout. Compact high voltage capacitors are particularly beneficial in modular grid components, mobile substations, offshore platforms, and other high-demand settings where space and thermal management are critical. By optimizing size-to-capacitance ratios, companies are making it easier for engineers and utility providers to integrate these solutions into advanced power electronics and renewable installations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.4 Billion |

| Forecast Value | $7.5 Billion |

| CAGR | 5.5% |

The film capacitors segment will reach USD 2.1 billion by 2034, growing at a 5.4% CAGR. Their widespread use is attributed to their long service life, strong thermal stability, and low inductance, making them highly reliable for filtering, power correction, and surge absorption in energy electronics. As energy transition trends continue, film capacitors are becoming a critical component in managing power flow in clean energy systems, especially within inverters and converters for solar and wind grid integration.

The transmission and distribution segment held a 49% share in 2024 and is forecast to grow at a CAGR of 5.2% through 2034. With the growing focus on grid efficiency and consistent power delivery over long distances, high-performance capacitors are in high demand. These components play a vital role in ensuring voltage stability across vast transmission infrastructures, especially in developing regions and nations expanding ultra-high voltage (UHV) and extra-high voltage (EHV) systems to support increasing electricity needs and wide territorial spans.

U.S. High Voltage Electric Capacitor Market held 77% share in 2024, generating USD 650 million. Growth is primarily driven by ongoing efforts to modernize the aging electric grid and increase the integration of cleaner energy sources. Utilities across the U.S. are investing heavily in robust capacitor technologies to manage reactive power, improve voltage consistency, and enhance grid resilience in response to fluctuating energy loads.

Key companies active in the market include Kemet, Murata, Panasonic, ABB, and Cornell Dubilier. To enhance their market positioning, companies in the high voltage electric capacitor sector are focusing on product innovation, strategic partnerships, and geographic expansion. Emphasis is being placed on developing advanced capacitor technologies with higher temperature resistance, better energy density, and longer service life to support applications in renewable integration and smart grid modernization. Firms are also investing in R&D to manufacture space-efficient, high-performance products that meet evolving customer demands in industrial and utility sectors. Establishing regional manufacturing units and service centers allows for reduced delivery times and localized support.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, 2024

- 4.3 Strategy dashboard

- 4.4 Strategic initiative

- 4.5 Competitive benchmarking

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Material, 2021 - 2034, ('000 Units and USD Billion)

- 5.1 Key trends

- 5.2 Film capacitors

- 5.3 Ceramic capacitors

- 5.4 Electrolytic capacitors

- 5.5 Others

Chapter 6 Market Size and Forecast, By End Use, 2021 - 2034, ('000 Units and USD Billion)

- 6.1 Key trends

- 6.2 Consumer electronics

- 6.3 Automotive

- 6.4 Communication & technology

- 6.5 Transmission & distribution

- 6.6 Others

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034, ('000 Units and USD Billion)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 France

- 7.3.3 Germany

- 7.3.4 Italy

- 7.3.5 Austria

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 South Korea

- 7.4.5 Australia

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Qatar

- 7.5.4 Kuwait

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

- 7.6.3 Chile

Chapter 8 Company Profiles

- 8.1 ABB

- 8.2 Cornell Dubilier

- 8.3 Elna

- 8.4 Havells

- 8.5 Kemet

- 8.6 Kyocera AVX

- 8.7 Murata Manufacturing

- 8.8 Panasonic

- 8.9 Samsung Electro-Mechanics

- 8.10 Schneider Electric

- 8.11 Siemens

- 8.12 Taiyo Yuden

- 8.13 TDK

- 8.14 Vishay Intertechnology