|

|

市場調査レポート

商品コード

1523352

自動車用プリント基板(PCB)の世界市場:市場シェア分析、産業動向・統計、成長予測(2024~2029年)Automotive Printed Circuit Board (PCB) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 自動車用プリント基板(PCB)の世界市場:市場シェア分析、産業動向・統計、成長予測(2024~2029年) |

|

出版日: 2024年07月15日

発行: Mordor Intelligence

ページ情報: 英文 90 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

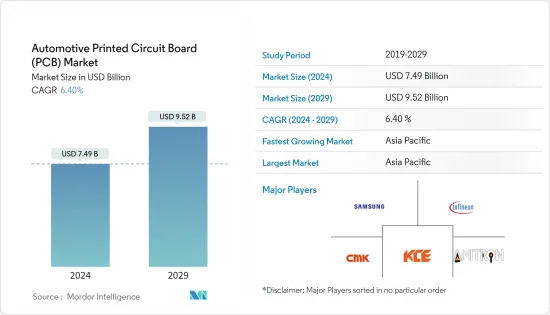

世界の自動車用プリント基板(PCB)の市場規模は、2024年に74億9,000万米ドルに達し、2024~2029年の予測期間中にCAGR 6.40%で成長し、2029年には95億2,000万米ドルに達すると予測されています。

自動車における電気システムの使用の増加、自動車におけるドライバーの快適性と安全性へのニーズの拡大、自動車セクターの大幅な拡大が、予測期間中の市場成長の主な促進要因として作用すると予想されます。

さらに、自動車の自動化が普及し、コネクテッドカーに対する需要が世界中で高まっていることから、自動車用PCBの需要は予測期間中に大きく伸びると予想されます。

人工知能(AI)、クラウド、IoT対応デバイスの統合により、車両および車両間通信が改善・強化されます。感情認識や行動認識、パーソナルアシスタントなどのAI搭載技術は、Vehicle As A Marketplaceのような安全性やシナリオの成長を後押ししており、ひいては自動車のパワーエレクトロニクス部品の需要を高める可能性が高いです。こうして、対象市場はさらに推進されています。

長期的には、産業大手による研究開発投資の増加、電気自動車やハイブリッド車の販売台数の増加、コネクテッドカー需要の高まりが、自動車用プリント基板の販売急増を伴う自動車・輸送産業の需要を生み出しています。

市場の主要企業は、自動車用プリント基板の需要増に対応するため、生産能力を拡大しています。

Denkai America Inc.は2022年7月、ジョージア州オーガスタに4億3,000万米ドルを投資し、北米本社と製造施設を設立すると発表しました。この製造施設には、EVバッテリー用のED銅箔を製造するための1億5,000万米ドルの製造ラインが含まれます。2022年3月、Ather EnergyとFoxconn Technology Groupの子会社であるBharat FIHは、Bharat FIHがプリント基板(PCB)を含むAther Energyの電気部品をインドで開発・製造する契約を締結しました。

自動車用プリント基板(PCB)市場動向

市場成長を牽引する電気自動車販売の拡大

中国、インド、欧州などの自動車大国の多くの政府は、これらの市場がすべて署名している2015年パリ気候変動協定の二酸化炭素削減目標を達成するために、EVの販売を促進することを目的とした様々な政府のインセンティブや政策を通じて、電気自動車の採用を執拗に推進しています。

電気自動車の販売台数は、昨年は全般的に低調であったにもかかわらず、2022年には世界全体で2021年比で約60%増加し、初めて1,000万台を突破しました。その結果、国際エネルギー機関(IEA)によれば、2022年に世界で購入された乗用車の7台に1台が電気自動車となった。とはいえ、2023年も電気自動車が上回る可能性が高いです。2023年第1四半期に販売された電気自動車は230万台を超え、前年同期比を上回る約25%の伸びとなった。2023年には、1,400万台の電気自動車が販売され、前年同期比35%の成長が見込まれます。

アジア太平洋と欧州のさまざまな国が、2040年までに内燃機関車の新車販売を禁止し、バッテリー式電気自動車を普及させると発表しています。石油価格の高騰、汚染レベルの上昇、環境意識の高まり、そして電気自動車を促進するための政府による数々の優遇措置が、世界中でEVの販売を非常に健全な成長へと導いています。

中国では、2022年のEV販売台数が366万台(9月まで)に達し、前年比119%の伸びを記録しました。インドでは、2022年のEV販売台数が39万399台(7月まで)に達し、前年比333%の伸びを記録しました。

電動ターボチャージャー(電動アシストターボチャージャーまたはeターボチャージャーとも呼ばれる)の登場は最近の動向です。これらのシステムは電気モーターを利用してターボチャージャーの性能を高め、過渡応答を改善することでターボラグを低減します。

自動車用PCBは、EVの中核部品であるバッテリーのすべての機能を制御します。このように、EVの販売台数の大幅な伸びは、世界の自動車用PCB産業の成長に非常に大きな原動力となっています。

乗用車の需要の増加と電気モビリティに対する意識の高まりにより、主要企業は設備の生産能力を増強しています。例えば

2023年5月、Hyundai Motor India Limitedは、インド全土の電気自動車製造施設を強化するために2,000億インドルピーを投資すると発表しました。

電気自動車の動向の高まりは、今後の市場成長を促進すると予想されます。

予測期間中、アジア太平洋が大きく成長すると予測

アジア太平洋は最も支配的な市場であり、北米、欧州がこれに続く。

アジア太平洋には、世界最大の自動車生産国であるインド、中国、日本、韓国があります。インドと中国は世界最大級の電気自動車市場であり、世界の電気自動車販売台数の60%近くを占めているため、アジア太平洋は自動車用プリント配線板にとって最も有利な市場となっています。自動車用プリント基板は、電気自動車に不可欠な機能を制御するため、この地域の大半の自動車に採用されています。

中国は世界最大の電気自動車製造・消費国です。国内需要は、販売目標、有利な法律、自治体の大気質目標によって支えられています。

中国は、電気自動車やハイブリッド車のメーカーに、新車販売台数の10%以上を占めるという割り当てを課しています。また、北京市は市民に電気自動車への乗り換えを促すため、内燃エンジン車の登録許可証を月に1万台しか発行しないです。自動車販売の増加と急速な都市化に伴い、中国は自動車の排気ガス削減を決定しています。その一方で、電気自動車の需要と販売を増やすことで、石油輸入への依存度を下げようとしています。

他国への輸出を目的とした自動車生産の増加は、同国における電動モビリティの採用とともに、中国におけるパワーエレクトロニクスとPCBの需要を押し上げると予想される主な要因です。

欧州と北米も、自動車OEMの存在感が大きく、自動車産業の電動化が進んでいるため、これらの地域では電気自動車の販売台数が多く、主要市場となっています。このように、自動車用プリント配線板市場は、各社がこの分野でイノベーションを打ち出していることから、予測期間中に電気自動車分野で成長すると予想されます。例えば、PCB Technologiesは2022年6月、シグナルインテグリティの向上と不要なインダクタンス効果の大幅な低減を実現するシステムインパッケージ(SIP)ソリューション、iNPACKを発表しました。このSIPソリューションは、自動車、家電、医療機器産業のさまざまな用途に利用できます。

自動車用プリント基板(PCB)産業の概要

自動車用プリント基板(PCB)市場は適度に統合されています。市場の特徴は、各地域の主要自動車OEMと長期供給契約を結んでいる世界企業やローカル企業が存在することです。これらのプレーヤーはまた、ブランドポートフォリオを拡大し、市場での地位を固めるために、合弁事業、M&A、新製品の発売、製品開拓を行っています。

世界市場を独占している主要企業には、Samsung Electro-Mechanical Ltd.、Infineon Corp.、CMK Corp.、KCE Electronics Ltd.、Amitron Corp.などがあります。多くのプレーヤーは、市場での地位を確保し、市場のカーブを先取りするために製造能力を拡大しています。例えば、2023年2月、Elna PCB Malaysia Sdn Bhdはマレーシアのペナンに新しいPCB製造工場を建設し、2024年に量産を開始すると発表しました。MYRの10億の投資予算は、設備、工場、機械、および2022年12月に開始したこの新工場の建設のために確保されました。この新工場では、自動車や電子機器用のPCBなどを製造します。

2022年4月、Infineon Technologies Corpの完全子会社であるPT Infineon Technologies Batam(インドネシア)は、2024年までにインドネシアのバックエンド生産能力を拡大すると発表しました。この拡張により、バタム工場はInfineon Technologies Corpにとって、マレーシアのマラッカ工場(車載用PCB)に次いで2番目に大きな工場となります。さらに、STMicroelectronics NVは2022年6月、車載および産業用アプリケーション向けの新しい高電圧プリント基板ベースのオペアンプを発表しました。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- EV販売の増加による自動車用PCB需要の増加

- 市場抑制要因

- 複雑な設計と統合の課題

- バリューチェーン/サプライチェーン分析

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 自動車タイプ別

- 乗用車

- 商用車

- 推進力タイプ別

- ICエンジン

- 電気式

- タイプ別

- シングルレイヤー

- ダブルレイヤー

- マルチレイヤー

- 用途別

- ADAS

- ボディ・コンフォート

- インフォテインメントシステム

- パワートレイン部品

- その他

- 地域別

- 北米

- 米国

- カナダ

- その他の北米

- 欧州

- ドイツ

- 英国

- フランス

- その他の欧州

- アジア太平洋

- インド

- 中国

- 日本

- 韓国

- その他のアジア太平洋

- その他の地域

- ブラジル

- アラブ首長国連邦

- その他の国

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Infineon Technologies AG

- Samsung Electro Mechanics

- CMK Corporation

- Amitron Corporation

- KCE Group

- Daeduck Phil. Inc.

- MEIKO ELECTRONICS Co. Ltd

- CHIN POON Industrial Co. Ltd

- Unimicron Group

- STMicroelectronics NV

- Tripod Technologies

第7章 市場機会と今後の動向

The Automotive Printed Circuit Board Market size is estimated at USD 7.49 billion in 2024, and is expected to reach USD 9.52 billion by 2029, growing at a CAGR of 6.40% during the forecast period (2024-2029).

The increasing use of electrical systems in cars and the expanding need for driver comfort and safety in vehicles, coupled with significant expansion of the automotive sector, are anticipated to act as major driving factors for market growth during the forecast period.

Furthermore, with the increasing popularity of vehicle automation and the growing demand for connected cars across the world, the demand for automotive PCBs is expected to grow significantly during the forecast period.

The integration of Artificial Intelligence (AI), cloud, and IoT-enabled devices to improve and enhance vehicle and vehicle-to-infrastructure communication. AI-powered technologies, such as emotional and behavioral recognition and personal assistants, have been fueling the growth of safety and scenarios, such as Vehicle As A Marketplace, which in turn is likely to enhance the demand for power electronics components in vehicles. Thus further propelling the target market.

Over the long term, increasing investments in R&D by major industry players and a rise in sales of electric and hybrid vehicles, as well as rising demand for connected vehicles fare creating demand in the automotive and transportation industry with a surge in sales of automotive printed circuit boards.

Key players in the market are expanding their production capacity to cater to the increased demand for automotive printed circuit boards. For instance,

In July 2022, Denkai America Inc. announced that it would invest USD 430 million in Augusta, Georgia, to set up its North American HQ and manufacturing facility. The manufacturing facility will include a USD 150 million production line to manufacture ED copper foils for EV batteries. In March 2022, Ather Energy and Bharat FIH, a Foxconn Technology Group subsidiary, signed an agreement wherein Bharat FIH will develop and manufacture electric components for Ather Energy, including printed circuit boards (PCBs), in India.

Automotive Printed Circuit Board Market Trends

Growing Electric Vehicles Sales Driving the Market Growth

Many governments in some of the largest automotive markets like China, India, and Europe are relentlessly promoting the adoption of electric vehicles through various government incentives and policies aimed at boosting the sales of EVs to meet the carbon reduction goals under the Paris Climate Change Accord 2015 to which all these markets are signatories.

Sales of electric cars increased by around 60% in 2022 globally when compared to 2021, surpassing 10 million for the first time, even though car sales broadly were soft last year. As a result, one in every seven passenger cars bought globally in 2022 was an EV, according to the International Energy Agency (IEA). Nonetheless, electric vehicles are likely to outperform in 2023 as well. More than 2.3 million electric cars have been sold during the first quarter of 2023, which translates to a growth of about 25%, which is more than in comparison to the same period last year. In 2023, 14 million electric car sales are expected, representing 35% year-on-year growth; this will increase the market share of electric cars up to 18% in total car sales.

Various countries in Asia-Pacific and Europe have announced that they will ban the sales of new ICE vehicles by 2040 in favor of battery electric vehicles. Rising oil prices, growing pollution levels, increasing environmental consciousness, and a number of government incentives to promote electromobility are all contributing to very healthy growth in sales of EVs around the world. For instance,

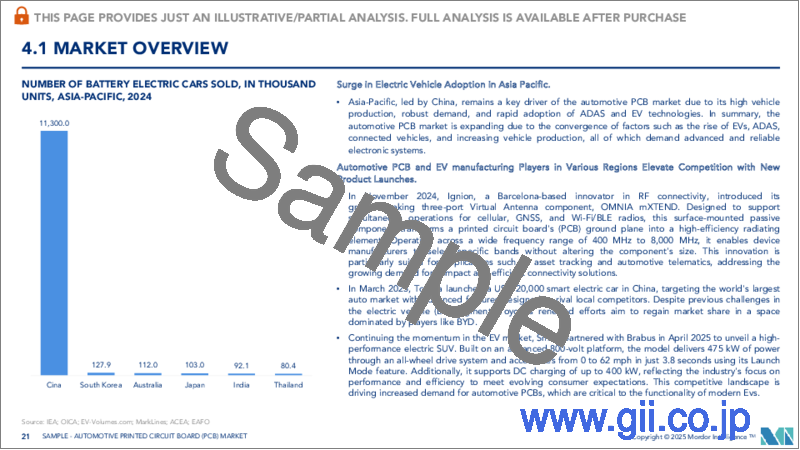

In China, EV sales rose to 3.66 million units in 2022 (till September), posting a YoY growth of 119%, while in India, EV sales stood at 390,399 units (till July) in 2022, registering a YoY increase of 333%.

The emergence of electric turbochargers, also known as electrically assisted turbochargers or e-turbochargers, is a recent development. These systems utilize electric motors to enhance turbocharger performance and improve transient response, thereby reducing turbo lag.

An automotive PCB controls all the functions of a battery, which is the core component of an EV. Thus, the massive growth in sales of EVs is providing a very high impetus to the growth of the automotive PCB industry worldwide.

Owing to the increase in the demand for passenger cars and the growing awareness of electric mobility, significant players are ramping up the production capacity of their facilities. For instance,

In May 2023, Hyundai Motor India Limited announced an investment of INR 200 billion to enhance its electric vehicle manufacturing facility across India.

The increase in the trend of electric vehicles is expected to drive market growth in the future.

Asia-Pacific Region Anticipated to Grow at a Significant Level During the Forecast Period

The Asia-Pacific is the most dominant market, followed by North America and Europe.

Asia-Pacific is home to India, China, Japan, and South Korea, the world's largest automobile manufacturing countries. India and China are some of the world's largest markets for electric vehicles, contributing to almost 60% of worldwide electric vehicle sales, thus making Asia-Pacific the most lucrative market for automotive printed circuit boards. Automotive printed circuit boards are employed in the majority of these vehicles within the region to control the essential functions of an electric vehicle.

China is the largest manufacturer and consumer of electric vehicles in the world. Domestic demand is being supported by sales targets, favorable laws, and municipal air-quality targets. For instance,

China has imposed a quota on manufacturers of electric or hybrid vehicles, which must represent at least 10% of total new sales. Also, the city of Beijing only issues 10,000 permits for the registration of combustion engine vehicles per month to encourage its inhabitants to switch to electric vehicles. With increased vehicle sales and rapid urbanization, China is determined to reduce vehicle exhaust emissions. Meanwhile, the country intends to reduce its reliance on oil imports by increasing demand for and sales of electric vehicles.

An increase in vehicle production for exporting to other countries, along with the adoption of electric mobility in the country, are the key factors that are expected to boost the demand for power electronics and PCBs in China.

Europe and North America are also major markets due to the large presence of automotive OEMs and the rising electrification of the automotive industry, leading to high electric vehicle sales in these geographies. Thus, with companies coming up with innovations in this segment, the market for automotive Printed Circuit Boards is expected to grow over the forecast period for the electric vehicles segment. For instance, in June 2022, PCB Technologies launched iNPACK, a System-in-Package (SIP) solution that offers improved signal integrity and a significant reduction in unwanted inductance effects. The SIP solution can be utilized for a variety of applications in the automobile, consumer electronics, and medical devices industries.

Automotive Printed Circuit Board Industry Overview

The automotive PCB market is moderately consolidated. The market is characterized by the presence of some global and local players who have secured long-term supply contracts with major automotive OEMs in their respective regions. These players also engage in joint ventures, mergers and acquisitions, new product launches, and product development to expand their brand portfolios and cement their market positions.

Some of the major players dominating the global market are Samsung Electro-Mechanical Ltd, Infineon Corp., CMK Corp., KCE Electronics Ltd, and Amitron Corp. Many players are expanding their manufacturing capacity to secure their market position and stay ahead of the market curve. For instance, in February 2023, Elna PCB Malaysia Sdn Bhd announced a new PCB manufacturing plant in Penang, Malaysia, with mass production set to start in 2024. MYR's 1 billion investment budget has been set aside for the equipment, plant, and machinery, as well as the construction of this new plant that commenced in December 2022. This new plant will manufacture PCBs for automotive and electronic devices usage, among other products.

In April 2022, PT Infineon Technologies Batam, Indonesia, a wholly owned subsidiary of Infineon Technologies Corp, announced it would expand the backend production capacity in Indonesia by 2024. This expansion will see the Batam site become the second biggest one for Infineon Technologies Corp after their Melaka, Malaysia plant for automotive PCBs. Additionally, in June 2022, STMicroelectronics NV introduced a new high-voltage Printed Circuit board-based op amplifier for automotive and industrial applications.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising EV Sales to Fuel Automotive PCB Demand

- 4.3 Market Restraints

- 4.3.1 Complex Design and Integration Challenges

- 4.4 Value Chain / Supply Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Vehicle Type

- 5.1.1 Passenger Cars

- 5.1.2 Commercial Vehicles

- 5.2 By Propulsion Type

- 5.2.1 IC Engine

- 5.2.2 Electric

- 5.3 By Type

- 5.3.1 Single Layer

- 5.3.2 Double Layer

- 5.3.3 Multi-Layer

- 5.4 By Application

- 5.4.1 ADAS

- 5.4.2 Body and Comfort

- 5.4.3 Infotainment System

- 5.4.4 Powertrain Components

- 5.4.5 Other Applications

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 India

- 5.5.3.2 China

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Rest of the World

- 5.5.4.1 Brazil

- 5.5.4.2 United Arab Emirates

- 5.5.4.3 Other Countries

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Infineon Technologies AG

- 6.2.2 Samsung Electro Mechanics

- 6.2.3 CMK Corporation

- 6.2.4 Amitron Corporation

- 6.2.5 KCE Group

- 6.2.6 Daeduck Phil. Inc.

- 6.2.7 MEIKO ELECTRONICS Co. Ltd

- 6.2.8 CHIN POON Industrial Co. Ltd

- 6.2.9 Unimicron Group

- 6.2.10 STMicroelectronics NV

- 6.2.11 Tripod Technologies