|

市場調査レポート

商品コード

1844349

自己免疫疾患診断の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Autoimmune Disease Diagnostics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 自己免疫疾患診断の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年09月17日

発行: Global Market Insights Inc.

ページ情報: 英文 145 Pages

納期: 2~3営業日

|

概要

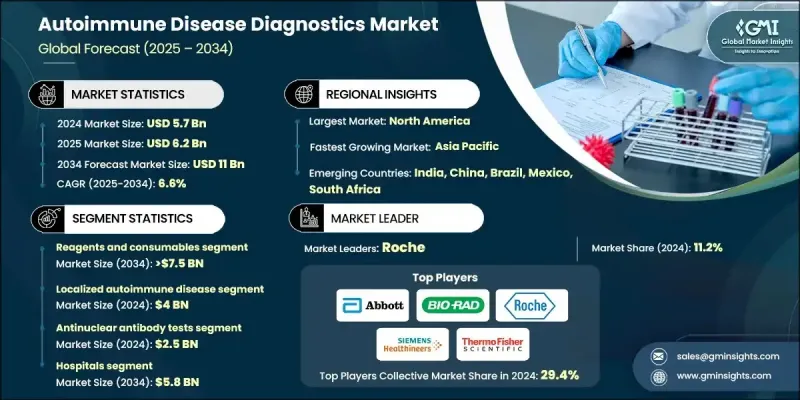

世界の自己免疫疾患診断市場は2024年に57億米ドルと評価され、CAGR 6.6%で成長し、2034年には110億米ドルに達すると推定されます。

自己免疫疾患の罹患率の上昇、早期診断に対する意識の高まり、継続的なスクリーニングプログラム、診断技術の着実な進歩が市場拡大に拍車をかけています。ヘルスケア支出の改善や早期発見のための革新的ツールの導入も、正確で迅速な検査に対する需要を強化しています。分子アッセイからイムノアッセイ、バイオマーカーに基づく検出まで、診断能力は臨床ニーズの高まりに合わせて進化しています。政府やヘルスケア機関が主導する患者教育キャンペーンは、検査件数を大幅に増加させています。同時に、特定のバイオマーカーを利用した精密診断の採用が拡大し、疾患の早期発見や患者ごとのモニタリングを通じて転帰が改善されつつあります。自己免疫疾患用のポータブルで迅速な検査ソリューションも人気を集めており、さまざまな医療現場で迅速な結果を提供し、市場の勢いをさらに加速させています。

| 市場規模 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 市場規模 | 57億米ドル |

| 予測金額 | 110億米ドル |

| CAGR | 6.6% |

2024年、試薬・消耗品セグメントは、自己免疫検査で繰り返し使用されるため、67%のシェアを占めています。診断用途におけるアッセイキット、抗体、緩衝液の絶え間ないニーズが、同分野の安定した成長に寄与しています。診断と長期的な疾患モニタリングの両方において検査がより頻繁に行われるようになるにつれ、これらの材料に対する需要は増加の一途をたどっています。検査機関や診療所は、正確で効率的な診断を行うために消耗品に大きく依存しており、このセグメントにおける安定した収益源を生み出しています。

局所自己免疫疾患分野は2024年に40億米ドルを生み出し、2034年までCAGR 6.4%で成長すると予想されています。このセグメントには、甲状腺疾患、炎症性腸疾患、1型糖尿病など、特定の臓器を標的とする疾患が含まれ、世界中で診断されるようになってきています。このような臓器特異的な疾患の増加は、局所的な疾患検出に特化した高感度かつ高精度の診断薬に対するニーズを煽るものです。この分野の継続的な成長は、長期的な合併症を回避するための早期介入と一貫したモニタリングの必要性によって支えられています。

北米自己免疫疾患診断2024年のシェアは36.6%。同地域では、多発性硬化症、ループス、関節リウマチ、1型糖尿病などの自己免疫疾患の罹患率が世界的に最も高いです。このような患者数の増加が、高度な診断検査に対する大きな需要を牽引しています。強力なヘルスケア・インフラと広範なスクリーニング・イニシアチブにより、この地域はルーチンとアドバンス両方の自己免疫検査をサポートし続けています。早期診断と個別化医療が重視され、市場の成長をさらに支えています。

自己免疫疾患診断の世界市場で活躍している主な企業は、Euroimmun、Thermo Fisher Scientific、Roche、Quest Diagnostics、Inova Diagnostics(Werfen)、DIAsource、Trinity Biotech、Revvvity、Labcorp、Siemens Healthineers、GRIFOLS、Hemagen Diagnostics、BIO-RAD、BIOMERIEUX、Abbottなどです。自己免疫疾患診断市場の企業は、戦略的提携、買収、先端技術への投資を通じてポートフォリオを拡大しています。多くの企業は、感度とスピードを向上させるため、バイオマーカーに基づく診断薬や次世代分子ツールの開発に注力しています。研究開発への投資拡大により、企業はポイントオブケア検査キットなど、より精密で使いやすい診断プラットフォームを導入できるようになっています。企業はまた、ラボのワークフローを合理化し、スループットを向上させるために自動化を優先しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 自己免疫疾患の発症率と有病率が高め

- 自己免疫疾患に関する意識の高まり

- 自己免疫疾患に関する調査活動に対する政府の支援政策

- 技術の進歩とラボ自動化技術の導入の増加

- 業界の潜在的リスク&課題

- 高度な診断検査の高コスト

- 検査結果の返却時間が遅く、複数の診断検査が必要

- 市場機会

- 診断におけるAIと機械学習の導入増加

- 家庭用および自己診断キットの成長

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- テクノロジーの情勢

- 現在の技術動向

- 新興技術

- ギャップ分析

- ポーターの分析

- PESTEL分析

- 将来の市場動向

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業の市場シェア分析

- グローバル

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ・中東・アフリカ

- 競合ポジショニングマトリックス

- 主要市場企業の競合分析

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品別、2021-2034

- 主要動向

- 試薬および消耗品

- 機器

第6章 市場推計・予測:病気の種類別、2021-2034

- 主要動向

- 局所性自己免疫疾患

- 1型糖尿病

- 炎症性腸疾患

- 甲状腺

- その他の局所性自己免疫疾患

- 全身性自己免疫疾患

- 関節リウマチ

- 全身性エリテマトーデス(SLE)

- 多発性硬化症

- 乾癬

- その他の全身性自己免疫疾患

第7章 市場推計・予測:テストタイプ別、2021-2034

- 主要動向

- 抗核抗体検査

- 自己抗体検査

- 全血球算定(CBC)

- C反応性タンパク質(CRP)

- 尿検査

- その他のテストの種類

第8章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 病院

- 診断センター

- その他の用途

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Abbott

- BIOMERIEUX

- BIO-RAD

- DIAsource

- Euroimmun

- GRIFOLS

- Hemagen Diagnostics

- Inova Diagnostics(Werfen)

- Labcorp

- Quest Diagnostics

- Revvity

- Roche

- SIEMENS Healthineers

- Thermo Fisher Scientific

- Trinity Biotech