|

市場調査レポート

商品コード

1833628

補聴器市場機会と促進要因、業界動向分析、2025年~2034年予測Hearing Amplifiers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 補聴器市場機会と促進要因、業界動向分析、2025年~2034年予測 |

|

出版日: 2025年09月15日

発行: Global Market Insights Inc.

ページ情報: 英文 135 Pages

納期: 2~3営業日

|

概要

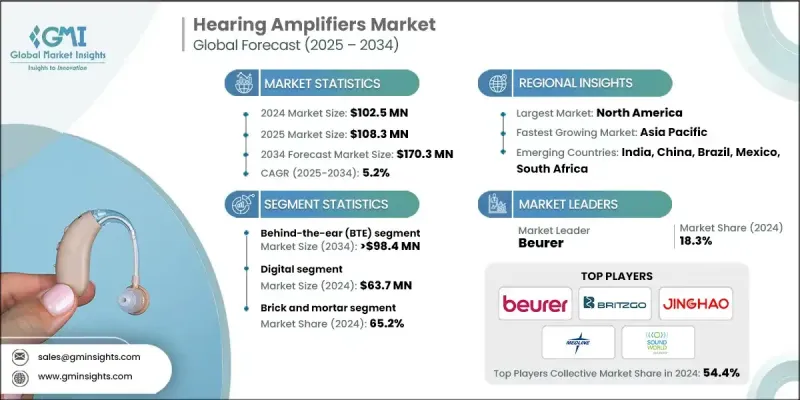

補聴器の世界市場は、2024年には1億250万米ドルとなり、CAGR 5.2%で成長し、2034年には1億7,030万米ドルに達すると予測されています。

この成長には、難聴経験者の増加、世界人口の急速な高齢化、音響増幅技術の継続的な革新、認知度と消費者の受け入れの増加など、いくつかの重要な要因があります。個人用音響増幅器(PSAP)と呼ばれるこの製品は、軽度から中等度の難聴者のために周囲の音の音量を上げるように設計されています。従来の補聴器とは異なり、PSAPは医療機器に分類されないため、聴覚専門医を必要とせず、店頭で簡単に手に入れることができます。手頃な価格と利便性により、多くの人々、特に高価な補聴器への投資をためらう高齢者にとって魅力的な選択肢となっています。主要企業は、戦略的な地理的ポジショニング、製品革新への強いこだわり、研究開発への多大な投資を通じて競争力を維持し、補聴器製品に磨きをかけています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 市場規模 | 1億250万米ドル |

| 予測金額 | 1億7,030万米ドル |

| CAGR | 5.2% |

2024年には、耳かけ型(BTE)分野が59%のシェアを占める。この分野は、ユーザーフレンドリーな機能、強力な増幅能力、様々な程度の聴覚障害への適合性から人気を博しています。BTEモデルは、耳かけ型に比べて調整が簡単で、快適で、人間工学的に優れているため、高齢の消費者、特に手が不自由な消費者に支持されています。このような品質により、BTE補聴器は幅広い層に好まれるソリューションとなっており、市場での優位性をさらに確固たるものにしています。

アナログ・セグメントは、2034年までCAGR 5.5%で成長すると予測されています。費用対効果を優先する消費者は、アナログモデルに引き寄せられ続けています。その魅力は、手頃な価格だけでなく、サウンド設定をカスタマイズできるシンプルで使いやすい操作性にもあります。これらの特徴は、先進国、開発途上国を問わず、パーソナル・サウンド・アンプに機能的で予算重視の選択肢を求める購買層を惹きつけています。

北米補聴器市場は2024年に38.5%のシェアを占める。同地域の成長の大きな原動力となっているのは、規制状況の変化、特に市販(OTC)補聴器の認可です。このような政策転換は、従来の参入障壁を取り除き、小売チャネルを拡大し、消費者が医師の診察を受けずに利用しやすい聴覚ソリューションを検討できるようにすることで、新たな成長機会を生み出しています。このような変化により、補聴器の認知度と関心は地域全体で大幅に高まっています。

補聴器業界を積極的に形成している主要プレーヤーには、MEDCA HEARING、JINGHAO、Sound World Solutions、Diglo、NUHEARA、Beurer、Alango、Medline、Britzgo、Kinetik Medical、Innerscope Hearing Technologies、Conversor、Foshan Vohom Technologyなどがいます。補聴器市場での足場を固めるため、各社は製品のイノベーションに重点を置き、高齢の消費者に合わせた人間工学的で高性能なデザインに焦点を当てています。多くの企業は、機能性、音質、ユーザー・コントロールを強化するため、研究開発に多額の投資を行っています。ワイヤレス技術と小型化の進歩を活用することで、各社は使いやすく、控えめで強力な機器を提供することを目指しています。OTCやオンライン小売チャネルを通じた流通の拡大は、アクセシビリティを高めるのに役立ちます。さらに、ヘルスケアプロバイダーとの提携や認知度向上を目指したプロモーション活動により、企業はより幅広い層を取り込み、成熟市場と新興市場の両方でブランドの存在感を確固たるものにしています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 加齢に伴う難聴の増加

- 高齢化人口の増加

- 増幅とノイズ低減の技術的改善

- 業界の潜在的リスク&課題

- 処方箋補聴器や人工内耳との競合

- 払い戻し/保険適用範囲が限られている

- 市場機会

- オンライン販売と遠隔聴覚検査プラットフォームの成長

- 製品の小型化と人間工学の改善

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- テクノロジーの情勢

- 現在の技術動向

- 新興技術

- 消費者経路

- 価格分析、2024

- ギャップ分析

- ポーター分析

- PESTEL分析

- 将来の市場動向

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業の市場シェア分析

- グローバル

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ・中東・アフリカ

- 競合ポジショニングマトリックス

- 主要市場企業の競合分析

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品別、2021-2034

- 主要動向

- 耳かけ型(BTE)

- 耳の中に装着するタイプ(ITE)

- その他の製品

第6章 市場推計・予測:技術別、2021-2034

- 主要動向

- デジタル

- アナログ

第7章 市場推計・予測:流通チャネル別、2021-2034

- 主要動向

- 店舗

- eコマース

第8章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Alango

- Beurer

- Britzgo

- Conversor

- Diglo

- Foshan Vohom Technology

- Innerscope Hearing Technologies

- JINGHAO

- Kinetik Medical

- MEDCA HEARING

- Medline

- NUHEARA

- Sound World Solutions