|

市場調査レポート

商品コード

1755367

スイッチング商用電圧レギュレータの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Switching Commercial Voltage Regulator Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| スイッチング商用電圧レギュレータの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月19日

発行: Global Market Insights Inc.

ページ情報: 英文 125 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

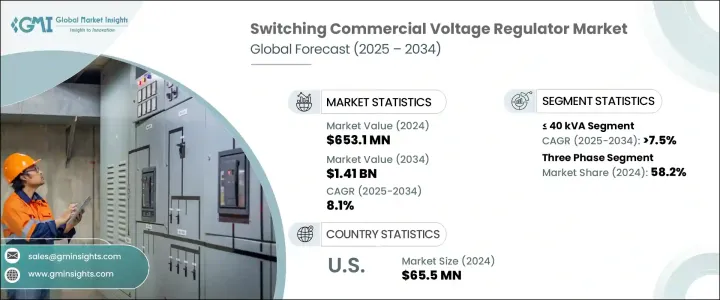

スイッチング商用電圧レギュレータの世界市場は、2024年に6億5,310万米ドルと評価され、電力品質管理の重要性の高まりとともに、高感度機器の精密な保護に対する需要の増加により、CAGR 8.1%で成長し、2034年には14億1,000万米ドルに達すると推定されます。

AIを活用した電圧安定化技術の技術的進歩が業界を強化すると予想されます。さらに、商業ビルにおける電力消費の増加や電力サージに対する懸念が市場の拡大に寄与しています。風力発電や太陽光発電などの再生可能エネルギーを送電網に統合することで、高度な電圧調整システムへの需要が高まる。

世界各国の政府がエネルギー効率化の取り組みに力を入れていることも、電力消費を最適化し運用コストを削減するこれらの装置の必要性をさらに高めています。自動化され、信頼性が高く、プログラム可能なデジタル・システムの継続的な進歩が、商用電圧レギュレータ市場の新たな成長機会を引き出しています。データセンターと通信ネットワークの成長とともに、産業オートメーションの採用が増加していることが、正確な電圧レギュレータの需要を促進しています。企業のデジタルインフラへの依存度が高まるにつれ、重要な業務をサポートする安定した正確な電力システムの必要性がこれまで以上に高まり、電圧レギュレータに大きなビジネスチャンスが生まれています。こうした分野の継続的な増加に伴い、高性能電圧レギュレーション・システムに対する需要は急増すると予想されます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 6億5,310万米ドル |

| 予測金額 | 14億1,000万米ドル |

| CAGR | 8.1% |

40kVA市場40 kVAスイッチング商用電圧レギュレータセグメントは、2034年まで7.5%以上の堅調な成長率が予測されています。これらの電圧レギュレーターは、繊細な業務用機器を電圧変動から保護し、コンピュータ、POSシステム、HVACユニット、照明システムなどの電子機器の動作信頼性と寿命を保証する上で極めて重要です。

同様に、三相スイッチング電圧レギュレータの需要も、2034年までにCAGR 8%で成長すると予測されています。これらのレギュレーターは、HVACシステム、エレベーター、その他の産業機器の無停止運転の維持など、高負荷アプリケーションに不可欠です。より厳しい電力品質基準の採用が、三相電圧レギュレータの需要を牽引しています。

米国スイッチング商用電圧レギュレータ2024年の市場規模は6,550万米ドル。政府の支援政策、技術の進歩、信頼性の高い配電システムへのニーズの高まりにより、大幅な成長が見込まれています。データセンター、ヘルスケア・インフラ、その他安定した高品質の電力システムを必要とする重要セクターの急速な拡大が、今後数年間の同市場の成長をさらに加速させると思われます。

スイッチング商用電圧レギュレータ世界市場の主要企業には、シーメンス、インフィニオンテクノロジーズ、マイクロチップテクノロジー、アナログ・デバイセズ、東芝電子デバイス&ストレージなどが含まれます。各社は、製品イノベーションへの投資、戦略的パートナーシップの形成、販売チャネルの強化により、市場でのプレゼンス拡大に注力しています。これにより、先進的なソリューションを提供し、業務効率を向上させ、高性能電圧レギュレーターの需要増に対応することができます。さらに、これらの企業の多くは、より自動化された信頼性の高い電圧調整ソリューションを提供するために、AI駆動技術やスマートシステムに投資しており、通信、ヘルスケア、産業オートメーションなど、さまざまな業界の進化するニーズに対応しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 戦略的ダッシュボード

- 戦略的取り組み

- 競合ベンチマーキング

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:フェーズ別、2021年~2034年

- 主要動向

- 単相

- 三相

第6章 市場規模・予測:電圧別、2021年~2034年

- 主要動向

- 40 kVA以下

- 40kVA~250kVA以上

- 250kVA以上

第7章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- フランス

- ロシア

- 英国

- イタリア

- スペイン

- オランダ

- オーストリア

- アジア太平洋

- 中国

- 日本

- 韓国

- インド

- オーストラリア

- ニュージーランド

- マレーシア

- インドネシア

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- エジプト

- 南アフリカ

- ナイジェリア

- クウェート

- オマーン

- ラテンアメリカ

- ブラジル

- ペルー

- アルゼンチン

第8章 企業プロファイル

- Analog Devices

- Bel Fuse

- Eaton

- Infineon Technologies

- Legrand

- MaxLinear

- Microchip Technology

- Minmax Technology

- Nisshinbo Micro Devices

- NXP Semiconductors

- Renesas Electronics Corporation

- ROHM

- SEMTECH

- Siemens

- STMicroelectronics

- SynQor

- TOREX SEMICONDUCTOR

- Toshiba Electronic Devices &Storage Corporation

- Vicor Corporation

- Vishay Intertechnology

The Global Switching Commercial Voltage Regulator Market was valued at USD 653.1 million in 2024 and is estimated to grow at a CAGR of 8.1% to reach USD 1.41 billion by 2034, driven by the increasing demand for precise protection of sensitive equipment, along with the rising importance of managing power quality. Technological advancements in AI-powered voltage stabilization technologies are expected to strengthen the industry. Additionally, the growing power consumption in commercial buildings and concerns about power surges contribute to the market's expansion. Integrating renewable energy sources such as wind and solar power into the grid spurs demand for advanced voltage regulation systems.

Governments worldwide are focusing on energy efficiency initiatives, which are further boosting the need for these devices to optimize power consumption and reduce operational costs. The continuous advancements in automated, reliable, and programmable digital systems are unlocking new growth opportunities in the commercial voltage regulator market. The increasing adoption of industrial automation, alongside the growth of data centers and telecommunication networks, is driving the demand for precise voltage regulation. As businesses rely more on digital infrastructure, the need for stable and accurate power systems to support critical operations is more important than ever, creating significant business opportunities for voltage regulators. With the continuous rise of these sectors, the demand for high-performance voltage regulation systems is expected to surge.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $653.1 Million |

| Forecast Value | $1.41 Billion |

| CAGR | 8.1% |

The market for ? 40 kVA switching commercial voltage regulator segment is projected to experience a robust growth rate of over 7.5% through 2034. These voltage regulators are crucial in protecting sensitive commercial equipment from voltage fluctuations, ensuring the operational reliability and longevity of electronics such as computers, point-of-sale systems, HVAC units, and lighting systems.

Similarly, the demand for three-phase switching voltage regulator segment is forecast to grow at a CAGR of 8% by 2034. These regulators are vital for high-load applications, such as maintaining the uninterrupted operation of HVAC systems, elevators, and other industrial equipment. Adopting stricter power quality standards drives the demand for three-phase voltage regulators.

United States Switching Commercial Voltage Regulator Market was valued at USD 65.5 million in 2024. It is expected to grow significantly due to supportive government policies, technological advancements, and the increasing need for reliable distribution systems. The rapid expansion of data centers, healthcare infrastructure, and other critical sectors that demand consistent and high-quality power systems will further fuel this market's growth in the coming years.

Key players in the Global Switching Commercial Voltage Regulator Market include Siemens, Infineon Technologies, Microchip Technology, Analog Devices, and Toshiba Electronic Devices & Storage Corporation, among others. Companies focus on expanding their market presence by investing in product innovation, forming strategic partnerships, and enhancing distribution channels. This allows them to offer advanced solutions, improve operational efficiencies, and meet the increasing demand for high-performance voltage regulators. Additionally, many of these companies are investing in AI-driven technologies and smart systems to offer more automated and reliable voltage regulation solutions, catering to the evolving needs of various industries such as telecommunications, healthcare, and industrial automation.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, 2024

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Phase, 2021 - 2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 Single phase

- 5.3 Three phase

Chapter 6 Market Size and Forecast, By Voltage, 2021 - 2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 ≤ 40 kVA

- 6.3 > 40 kVA to 250 kVA

- 6.4 > 250 kVA

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 France

- 7.3.3 Russia

- 7.3.4 UK

- 7.3.5 Italy

- 7.3.6 Spain

- 7.3.7 Netherlands

- 7.3.8 Austria

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 South Korea

- 7.4.4 India

- 7.4.5 Australia

- 7.4.6 New Zealand

- 7.4.7 Malaysia

- 7.4.8 Indonesia

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Qatar

- 7.5.4 Egypt

- 7.5.5 South Africa

- 7.5.6 Nigeria

- 7.5.7 Kuwait

- 7.5.8 Oman

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Peru

- 7.6.3 Argentina

Chapter 8 Company Profiles

- 8.1 Analog Devices

- 8.2 Bel Fuse

- 8.3 Eaton

- 8.4 Infineon Technologies

- 8.5 Legrand

- 8.6 MaxLinear

- 8.7 Microchip Technology

- 8.8 Minmax Technology

- 8.9 Nisshinbo Micro Devices

- 8.10 NXP Semiconductors

- 8.11 Renesas Electronics Corporation

- 8.12 ROHM

- 8.13 SEMTECH

- 8.14 Siemens

- 8.15 STMicroelectronics

- 8.16 SynQor

- 8.17 TOREX SEMICONDUCTOR

- 8.18 Toshiba Electronic Devices & Storage Corporation

- 8.19 Vicor Corporation

- 8.20 Vishay Intertechnology