|

市場調査レポート

商品コード

1716722

水素化処理植物油(HVO)市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Hydrotreated Vegetable Oil Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 水素化処理植物油(HVO)市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月12日

発行: Global Market Insights Inc.

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

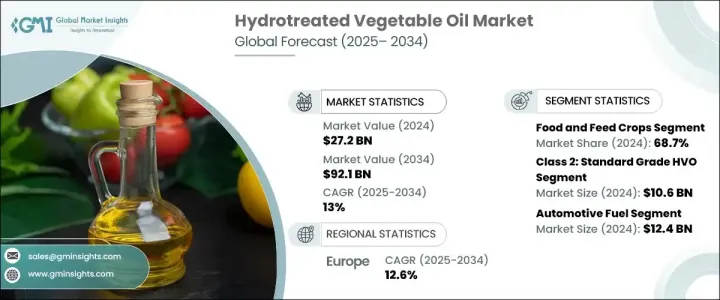

世界の水素化処理植物油(HVO)市場は、2024年に272億米ドルに達し、2025年から2034年にかけてCAGR 13%で拡大すると予測されています。

再生可能エネルギー源へのシフトの高まりにより、HVOは産業界全体で持続可能な代替燃料としての役割を急速に高めています。世界経済が化石燃料への依存度低減に軸足を移す中、HVOは脱炭素目標を達成するための重要なソリューションとして台頭しつつあります。HVOは従来のディーゼル燃料のドロップイン代替燃料として機能し、よりクリーンな燃焼と温室効果ガス排出量の削減を実現することから、運輸、航空、産業用発電などの主要セクターで需要が高まっています。

特に北米と欧州のいくつかの政府は、HVOの使用を直接奨励する税額控除、混合燃料の義務付け、排出枠の設定などの政策枠組みにより、炭素排出削減の義務付けを強化しています。こうした政策は、HVOメーカーに新たな成長機会をもたらし、より環境に優しいエネルギーへの世界的シフトにおけるHVOの重要性を強めています。先進バイオ燃料や次世代原料への官民投資の増加は、コスト競争力を維持しながらHVO生産を拡大する革新的な方法を公開会社が模索する中で、市場の見通しをさらに強めています。ESG(環境・社会・ガバナンス)目標の達成を目指す産業が増える中、HVOのようなクリーンで低炭素な代替燃料への注目はますます高まっており、先進経済諸国と新興経済諸国の両方で急速な普及が進んでいます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 272億米ドル |

| 予測金額 | 921億米ドル |

| CAGR | 13% |

2024年には、食用・飼料用作物分野が68.7%のシェアでHVO市場を独占し、2034年までのCAGRは12.4%で成長すると予測されます。HVO生産における食用・飼料用作物の広範な使用は、その豊富な入手可能性、強固なサプライチェーン、それらを支える確立された農業の枠組みが主な要因です。大豆や菜種のような作物は、効率的なHVO生産に必要な油の供給において極めて重要であり、増大するバイオ燃料需要を満たすための安定した原料供給を保証しています。食料安全保障や土地利用をめぐる懸念が注目される一方で、作物由来のバイオ燃料を支持する政策が各地域で続いており、市場の成長をさらに後押ししています。

市場はグレード別にも区分され、プレミアムグレード、スタンダードグレード、ベーシックグレード、スペシャルティグレードがあります。このうち、スタンダードグレードのHVOセグメントは、2024年に106億米ドルを生み出し、2025年から2034年にかけてCAGR 12.7%で成長するとみられています。標準グレードは、コスト、性能、汎用性のバランスからますます好まれるようになっており、輸送、産業運営、発電に理想的な選択肢となっています。スタンダードグレードは、ニッチで高性能なセクターで一般的に使用される高級プレミアムグレードに比べ、経済的に実行可能でありながら、厳しい排出規制に適合しています。

地域別では、欧州の水素化処理植物油(HVO)市場は2024年に103億米ドルに達し、2034年までのCAGRは12.6%と予測されています。欧州は、強力な規制状況の後押しと再生可能燃料への需要の高まりにより、引き続き世界のHVO市場をリードしています。欧州連合(EU)のRED II指令とバイオ燃料混合義務付けの増加は、HVOの統合を大幅に加速させ、欧州を低炭素エネルギーへの移行に向けた世界の取り組みの最前線に位置付けています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュースと取り組み

- 規制状況

- 影響要因

- 促進要因

- HVO生産技術の進歩

- 再生可能エネルギーへの需要の高まり

- 自動車セクターからの需要増加

- 業界の潜在的リスク&課題

- 高い生産コスト

- 他の再生可能燃料との競合

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場規模・予測:原料供給源別、2021年~2034年

- 主要動向

- 食品・飼料用作物

- 大豆油

- カノーラ油

- ひまわり油

- パーム油

- その他

- 動物性油脂

- タロウ

- ラード

- 使用済み食用油

- パーム油工場廃液

- その他

第6章 市場規模・予測:グレード別、2021年~2034年

- 主要動向

- クラス1:プレミアムグレードHVO

- クラス2:スタンダードグレードHVO

- クラス3:ベーシックグレードHVO

- クラス4:スペシャルティグレードHVO

第7章 市場規模・予測:技術別、2021年~2034年

- 主要動向

- 独立型水素化処理技術

- コプロセシング技術

第8章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- サステナブル航空燃料

- 自動車燃料

- 船舶用燃料

- 産業用発電燃料

- 暖房用燃料

- 農業機械燃料

- 潤滑油

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第10章 企業プロファイル

- ALFA LAVAL

- Cepsa

- Desmet

- DIAMOND GREEN DIESEL

- Neste

- Preem

- Repsol

- Shell

- TotalEnergies

- UPM Biofuels

- Valero Energy

- World Energy

The Global Hydrotreated Vegetable Oil Market reached USD 27.2 billion in 2024 and is projected to expand at a CAGR of 13% between 2025 and 2034. The growing shift toward renewable energy sources is rapidly elevating HVO's role as a sustainable fuel alternative across industries. As global economies pivot to reducing dependence on fossil fuels, HVO is emerging as a critical solution for meeting decarbonization goals. Its ability to serve as a drop-in replacement for traditional diesel, combined with cleaner combustion and lower greenhouse gas emissions, is pushing demand among major sectors, including transportation, aviation, and industrial power generation.

Several governments, particularly in North America and Europe, are stepping up mandates to cut carbon emissions with policy frameworks like tax credits, blending mandates, and emission caps that directly encourage the use of HVO. These policies are opening new growth opportunities for HVO producers and reinforcing their importance in the global shift toward greener energy. Increasing public and private investments in advanced biofuels and next-generation feedstocks are further enhancing the market outlook as companies explore innovative ways to scale HVO production while keeping costs competitive. As more industries seek to meet ESG (Environmental, Social, and Governance) goals, the focus on clean-burning, low-carbon alternatives like HVO continues to intensify, fueling rapid adoption across both developed and emerging economies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $27.2 Billion |

| Forecast Value | $92.1 Billion |

| CAGR | 13% |

In 2024, the food and feed crops segment dominated the HVO market with a 68.7% share and is anticipated to grow at a CAGR of 12.4% through 2034. The widespread use of food and feed crops in HVO production is largely driven by their abundant availability, robust supply chains, and the well-established agricultural framework supporting them. Crops like soybeans and rapeseed are pivotal in supplying the oils required for efficient HVO production, ensuring a steady feedstock supply to meet growing biofuel demand. While concerns around food security and land use are gaining attention, policies across regions still back crop-based biofuels, further propelling market growth.

The market is also segmented by grade, covering premium grade, standard grade, basic grade, and specialty grade. Among these, the standard grade HVO segment generated USD 10.6 billion in 2024 and is set to grow at a CAGR of 12.7% from 2025 to 2034. Standard grade is increasingly preferred due to its balance of cost, performance, and versatility, making it an ideal choice for transportation, industrial operations, and power generation. It meets stringent emission norms while remaining economically viable compared to higher-end premium grades that are typically used in niche, high-performance sectors.

Regionally, Europe's Hydrotreated Vegetable Oil Market reached USD 10.3 billion in 2024 and is projected to grow at a CAGR of 12.6% through 2034. Europe continues to lead the global HVO landscape, driven by powerful regulatory backing and escalating demand for renewable fuels. The European Union's RED II directive and rising biofuel blending mandates have greatly accelerated HVO integration, positioning Europe at the forefront of global efforts to transition to low-carbon energy.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Advancements in HVO production technology

- 3.6.1.2 Growing demand for renewable energy sources

- 3.6.1.3 Increasing demand from the automotive sector

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High production costs

- 3.6.2.2 Competition from other renewable fuels

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Size and Forecast, By Source of Feedstock, 2021 – 2034 (USD Billion, Kilo Tons)

- 5.1 Key trends

- 5.2 Food and feed crops

- 5.2.1 Soybean oil

- 5.2.2 Canola oil

- 5.2.3 Sunflower oil

- 5.2.4 Palm oil

- 5.2.5 Others

- 5.3 Animal fats

- 5.3.1 Tallow

- 5.3.2 Lard

- 5.4 Used cooking oils

- 5.5 Palm oil mill effluent

- 5.6 Others

Chapter 6 Market Size and Forecast, By Grade, 2021 – 2034 (USD Billion, Kilo Tons)

- 6.1 Key trends

- 6.2 Class 1: premium grade HVO

- 6.3 Class 2: standard grade HVO

- 6.4 Class 3: basic grade HVO

- 6.5 Class 4: specialty grade HVO

Chapter 7 Market Size and Forecast, By Technology, 2021 – 2034 (USD Billion, Kilo Tons)

- 7.1 Key trends

- 7.2 Standalone hydrotreating technology

- 7.3 Co-Processing technology

Chapter 8 Market Size and Forecast, By Application, 2021 – 2034 (USD Billion, Kilo Tons)

- 8.1 Key trends

- 8.2 Sustainable aviation fuel

- 8.3 Automotive fuel

- 8.4 Marine fuel

- 8.5 Industrial power generation

- 8.6 Heating fuel

- 8.7 Agricultural equipment fuel

- 8.8 Lubricants

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 ALFA LAVAL

- 10.2 Cepsa

- 10.3 Desmet

- 10.4 DIAMOND GREEN DIESEL

- 10.5 Neste

- 10.6 Preem

- 10.7 Repsol

- 10.8 Shell

- 10.9 TotalEnergies

- 10.10 UPM Biofuels

- 10.11 Valero Energy

- 10.12 World Energy