|

市場調査レポート

商品コード

2019217

産業用ラムノリピッド市場の機会、成長要因、業界動向分析、および2026年~2035年の予測Industrial Rhamnolipid Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 産業用ラムノリピッド市場の機会、成長要因、業界動向分析、および2026年~2035年の予測 |

|

出版日: 2026年03月31日

発行: Global Market Insights Inc.

ページ情報: 英文 205 Pages

納期: 2~3営業日

|

概要

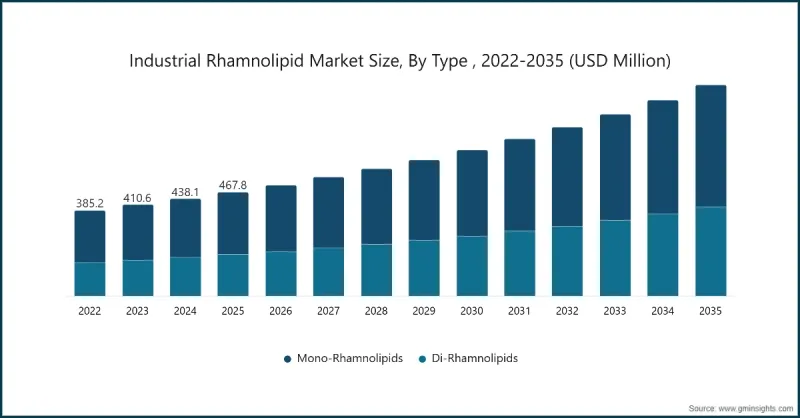

世界の産業用ラムノリピッド市場は、2025年に4億6,780万米ドルと評価され、CAGR8.4%で成長し、2035年までに9億5,050万米ドルに達すると推定されています。

産業用ラムノリピッドは当初、ニッチなバイオ由来界面活性剤として登場しましたが、現在では複数の産業分野において不可欠な成分へと進化しています。その機能的な用途は現在、エネルギー生産、工業用洗浄、農業、環境修復などの分野において、プロセス効率の向上、材料適合性の強化、および運用信頼性の確保にまで広がっています。産業分野における調達では、再生可能で、毒性が低く、環境的に持続可能なものであると同時に、高い性能を発揮する原料がますます好まれるようになっています。バイオテクノロジー、発酵制御、菌株の最適化、および後工程処理の進歩により、ラムノリピッドの性能は産業基準を満たすレベルにまで向上しました。配合との適合性、生分解性、および環境中での残留性の低さが相まって、特に規制が厳格で持続可能性の要件が課されている地域において採用が加速しており、既存市場と新興市場の両方で着実な成長を牽引しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025 |

| 予測期間 | 2026-2035 |

| 開始時の市場規模 | 4億6,780万米ドル |

| 予測額 | 9億5,050万米ドル |

| CAGR | 8.4% |

モノラムノリピッドセグメントは60.4%のシェアを占めており、2035年までCAGR7.8%で成長すると予想されています。その広範な利用は、優れた界面活性、溶解性、および製剤との相容性に起因しています。各業界では、界面張力を低減するコスト効率の高い性能から、洗浄、油田化学、環境修復などの用途にモノラムノリピッドを活用しています。ダイラムノリピッドは市場規模は小さいもの、優れた乳化特性、過酷な条件下での安定性、および長期的な機能耐久性により、注目を集めています。

液体製剤セグメントは2025年に70.6%のシェアを占め、2026年から2035年にかけてCAGR8.1%で成長すると予測されています。液体ラムノリピドは、取り扱いの容易さ、即時の溶解性、および油田作業、工業用洗浄、環境処理などのプロセスへのシームレスな統合が可能であることから、大規模な産業用途で好まれています。連続処理への適性、正確な投与、柔軟な製剤開発が可能である点が、産業分野での人気をさらに高めています。

北米の産業用ラムノリピッド市場は、エネルギー生産、工業用洗浄、環境保護の各分野におけるバイオ由来界面活性剤の導入において戦略的な役割を果たしていることから、2025年には28.4%のシェアを占めました。好調な市場環境、高度な産業インフラ、そして持続可能なソリューションの普及率の高さが、同地域を主要な成長拠点としています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 石油・ガス産業における増進採油(EOR)での利用拡大

- 化粧品およびパーソナルケア産業における用途の拡大

- 環境に優しいおよび生分解性界面活性剤への需要の高まり

- 業界の潜在的リスク&課題

- 高い生産コスト

- ラムノリピド生産用原材料の供給不足

- 市場機会

- バイオレメディエーションおよび環境分野への展開

- 医薬品および薬物送達システムの開発

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- タイプ別

- 今後の市場動向

- 技術・イノベーションの動向

- 現在の技術動向

- 新興技術

- 特許動向

- 貿易統計(HSコード)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境面

- 持続可能な取り組み

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に配慮した取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 事業拡大計画

第5章 市場推計・予測:タイプ別、2022-2035

- モノラムノリピド

- ジーラムノリピド

第6章 市場推計・予測:形態別、2022-2035

- 液体

- 即用型

- 濃縮タイプ

- 水懸濁液

- 粉末

- 噴霧乾燥

- 凍結乾燥

- バルク工業用

第7章 市場推計・予測:グレード別、2022-2035

- テクニカルグレード(85~90%)

- 高純度グレード(90~95%)

- 超高純度グレード(95%超)

第8章 市場推計・予測:エンドユーザー別、2022-2035

- 石油・ガス

- 農業

- 医薬品・ヘルスケア

- 化粧品・パーソナルケア

- その他(繊維、家庭用・工業用洗剤など)

第9章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ地域

第10章 企業プロファイル

- Evonik Industries AG

- Stepan Company

- AGAE Technologies LLC

- Jeneil Biotech Inc

- Biotensidon GmbH

- GlycoSurf

- TensioGreen

- Zhejiang Silver Elephant Bio-engineering Co. Ltd

- Shaanxi Deguan Biotechnology Co. Ltd

- Holiferm Ltd

- CD BioGlyco