|

市場調査レポート

商品コード

1755381

自動モータースターターの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Automatic Motor Starter Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 自動モータースターターの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月22日

発行: Global Market Insights Inc.

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

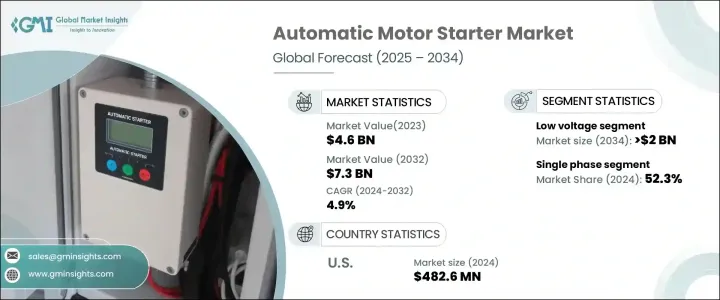

自動モータースターターの世界市場規模は、2024年に46億米ドルとなり、CAGR 4.9%で成長し、2034年には73億米ドルに達すると予測されています。

成長の原動力となっているのは、産業オートメーションの急増と、エネルギー効率の高い運用に対する需要の高まりです。自動モータースタータは、電気モーターの制御を支援し、合理化された始動停止機能を可能にし、過負荷、相故障、短絡からの保護を提供します。電力供給を制御することで、これらのデバイスは効率的なモーター運転、スムーズな始動を保証し、潜在的な電気的危険から保護します。

化学、石油・ガス、製造、水処理などの産業で電気モーターの使用が拡大していることが、市場を強化しています。これらのセクターが持続可能な実践とデジタル変革を追求する中、自動モータースタータはエネルギー使用量を削減し、始動時のサージを防止するためにエネルギー管理システムと統合されています。さらに、産業用IoTとスマート工場のフレームワークの進展が、これらのソリューションの需要を支えています。トランプ政権下では、産業用電気部品、特に中国からの輸入品に関税が課され、生産コストとサプライチェーンの混乱が増大しました。短期的な影響は厳しいものであったが、こうした貿易制限は国内生産に新たな機会をもたらし、海外調達への依存を減らし、長期的な供給の安定性を向上させました。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 46億米ドル |

| 予測金額 | 73億米ドル |

| CAGR | 4.9% |

中電圧分野は、2034年までにCAGR 4.5%で成長します。これらのシステムは、石油・ガス、鉱業、水処理などの分野での高出力運転に不可欠であり、大型モーターを正確に管理することが機器の安全性と運転効率にとって重要です。中電圧スターターは、モーター始動時の機械的ストレスを軽減するのに役立ち、過酷な条件下で高負荷の産業用機器を扱う施設には不可欠です。これらのシステムに対する需要は、公共事業や重工業におけるインフラのアップグレードやエネルギー需要の増加によってさらに高まっています。

三相自動モータースターターセグメントは、商業用HVAC、スマート灌漑システム、大規模ビルインフラでの設置増加により、2034年までに35億米ドルに達する見込みです。ModbusやBACnetのようなインテリジェント通信機能を備えたこれらのスターターは、リアルタイムのシステム監視、予測診断、ビルオートメーションシステムとのシームレスな統合を可能にします。これは、エネルギー効率、システムの最適化、遠隔制御機能を優先する、よりスマートな産業環境へ向けた増加傾向に沿ったものです。

米国の自動モータースターター2024年の市場規模は4億8,260万米ドルで、産業オートメーションにおける高度なマイクロプロセッサベースの制御システムの採用が後押ししています。米国市場はまた、デジタル産業エコシステムへの移行が加速し、再生可能エネルギーへの依存度が高まっていることから、力強い勢いを見せています。これらの要因は、コネクテッド、低排出、エネルギー重視のモーター制御ソリューションの拡大に有利な環境を作り出しています。

世界の自動モータースターター産業の革新と市場競争を牽引する主要企業には、Eaton、ABB、Danfoss、General Electric、Schneider Electric、Rockwell Automation、三菱電機、Honeywell International、Siemens、WEG、Emerson Electric、Fuji Electric FA Components &Systems、L&T Electrical &Automation、Kalp Controls、CHINT Group、C&S Electric、Havells India、SKN-BENTEX GROUP、LOVATO ELECTRICなどがあります。競争力を強化するため、自動モータースターター市場の主要企業は、進化する工業規格に対応したデジタル統合型のエネルギー効率に優れたソリューションの開発に注力しています。その戦略には、リアルタイムの故障検知や遠隔監視機能を備えた、よりスマートなスターターの研究開発への投資も含まれます。これらのブランドは、イノベーションとパートナーシップを通じて製品ポートフォリオを拡大し、複数の業界の需要に対応しています。貿易障壁を回避し、リードタイムを改善するための生産の現地化も、重要な焦点となっています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 戦略的ダッシュボード

- 戦略的取り組み

- 競合ベンチマーキング

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:電圧別、2021年~2034年

- 主要動向

- 低

- 中

- 高

第6章 市場規模・予測:フェーズ別、2021年~2034年

- 主要動向

- 単相

- 三相

第7章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- 住宅用

- 商業用

- 産業

第8章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- フランス

- ロシア

- 英国

- イタリア

- スペイン

- オランダ

- オーストリア

- アジア太平洋

- 中国

- 日本

- 韓国

- インド

- オーストラリア

- ニュージーランド

- マレーシア

- インドネシア

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- エジプト

- 南アフリカ

- ナイジェリア

- クウェート

- オマーン

- ラテンアメリカ

- ブラジル

- ペルー

- アルゼンチン

第9章 企業プロファイル

- ABB

- C&S Electric

- CHINT Group

- Danfoss

- Eaton

- Emerson Electric

- Fuji Electric FA Components &Systems

- General Electric

- Havells India

- Honeywell International

- Kalp Controls

- L&T Electrical &Automation

- LOVATO ELECTRIC

- Mitsubishi Electric

- Rockwell Automation

- Schneider Electric

- Siemens

- SKN-BENTEX GROUP

- WEG

The Global Automatic Motor Starter Market was valued at USD 4.6 billion in 2024 and is estimated to grow at a CAGR of 4.9% to reach USD 7.3 billion by 2034. The growth is fueled by the surge in industrial automation and the rising demand for energy-efficient operations. Automatic motor starters help control electric motors, enabling streamlined start-stop functions and offering protection from overloads, phase faults, and short circuits. By controlling power delivery, these devices ensure efficient motor operation, smoother startups, and safeguard against potential electrical hazards.

The expanding use of electric motors across industries such as chemicals, oil and gas, manufacturing, and water treatment is strengthening the market. As these sectors pursue sustainable practices and digital transformation, automatic motor starters are integrated with energy management systems to cut energy usage and prevent surges during startup. In addition, the advancement of industrial IoT and smart factory frameworks support the demand for these solutions. During the Trump administration, tariffs on industrial electrical parts, especially those imported from China increased production costs and supply chain disruption. Although the short-term impact was challenging, these trade restrictions also opened new opportunities for domestic production, reducing dependence on foreign sourcing and improving long-term supply stability.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.6 Billion |

| Forecast Value | $7.3 Billion |

| CAGR | 4.9% |

The medium voltage segment will grow at a CAGR of 4.5% by 2034. These systems are vital for high-power operations in sectors like oil and gas, mining, and water treatment, where managing large motors with precision is critical for equipment safety and operational efficiency. Medium voltage starters help reduce mechanical stress during motor startup, making them essential for facilities handling heavy-duty industrial loads under harsh conditions. The demand for these systems is further driven by infrastructure upgrades and rising energy needs across utilities and heavy industries.

The three-phase automatic motor starter segment is expected to reach USD 3.5 billion by 2034 fueled by increased installations in commercial HVAC, smart irrigation systems, and large-scale building infrastructure. These starters with intelligent communication features like Modbus and BACnet, enabling real-time system monitoring, predictive diagnostics, and seamless integration with building automation systems. This aligns with the growing trend toward smarter industrial environments prioritizing energy efficiency, system optimization, and remote-control capabilities.

United States Automatic Motor Starter Market was valued at USD 482.6 million in 2024, bolstered by the adoption of advanced microprocessor-based control systems in industrial automation. The U.S. market is also experiencing strong momentum due to an accelerated transition to digital industrial ecosystems and an increasing reliance on renewable energy. These factors create a favorable climate for expanding connected, low-emission, and energy-conscious motor control solutions.

Key players driving innovation and market competition in the Global Automatic Motor Starter Industry include Eaton, ABB, Danfoss, General Electric, Schneider Electric, Rockwell Automation, Mitsubishi Electric, Honeywell International, Siemens, WEG, Emerson Electric, Fuji Electric FA Components & Systems, L&T Electrical & Automation, Kalp Controls, CHINT Group, C&S Electric, Havells India, SKN-BENTEX GROUP, and LOVATO ELECTRIC. To strengthen their competitive edge, leading companies in the automatic motor starter market focus on developing digitally integrated and energy-efficient solutions that align with evolving industrial standards. Strategies include investing in R&D for smarter starters with real-time fault detection and remote monitoring. These brands expand their product portfolios through innovation and partnerships to meet demand across multiple industries. Localization of production to bypass trade barriers and improve lead times has also become a key focus.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, 2024

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Voltage, 2021 - 2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 Low

- 5.3 Medium

- 5.4 High

Chapter 6 Market Size and Forecast, By Phase, 2021 - 2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Single phase

- 6.3 Three phase

Chapter 7 Market Size and Forecast, By Application, 2021 - 2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 Residential

- 7.3 Commercial

- 7.4 Industrial

Chapter 8 Market Size and Forecast, By Region, 2021 - 2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 France

- 8.3.3 Russia

- 8.3.4 UK

- 8.3.5 Italy

- 8.3.6 Spain

- 8.3.7 Netherlands

- 8.3.8 Austria

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 South Korea

- 8.4.4 India

- 8.4.5 Australia

- 8.4.6 New Zealand

- 8.4.7 Malaysia

- 8.4.8 Indonesia

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 Qatar

- 8.5.4 Egypt

- 8.5.5 South Africa

- 8.5.6 Nigeria

- 8.5.7 Kuwait

- 8.5.8 Oman

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Peru

- 8.6.3 Argentina

Chapter 9 Company Profiles

- 9.1 ABB

- 9.2 C&S Electric

- 9.3 CHINT Group

- 9.4 Danfoss

- 9.5 Eaton

- 9.6 Emerson Electric

- 9.7 Fuji Electric FA Components & Systems

- 9.8 General Electric

- 9.9 Havells India

- 9.10 Honeywell International

- 9.11 Kalp Controls

- 9.12 L&T Electrical & Automation

- 9.13 LOVATO ELECTRIC

- 9.14 Mitsubishi Electric

- 9.15 Rockwell Automation

- 9.16 Schneider Electric

- 9.17 Siemens

- 9.18 SKN-BENTEX GROUP

- 9.19 WEG