|

|

市場調査レポート

商品コード

1577260

自動車向けOTA(Over-The-Air)アップデート市場、機会、成長促進要因、産業動向分析と予測、2024年~2032年Automotive Over-The-Air (OTA) Update Market, Opportunity, Growth Drivers, Industry Trend Analysis and Forecast, 2024-2032 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 自動車向けOTA(Over-The-Air)アップデート市場、機会、成長促進要因、産業動向分析と予測、2024年~2032年 |

|

出版日: 2024年08月12日

発行: Global Market Insights Inc.

ページ情報: 英文 250 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

2023年に38億米ドルと評価された世界の自動車向けOTA(Over-The-Air)アップデート市場は、2024年から2032年にかけて17%以上のCAGRで成長すると予測されています。

コネクテッド・ビークルの需要と生産の急増が主な促進要因であり、シームレスなリモート・ソフトウェアとファームウェアのアップデートを促進しています。自動車の高度なコネクティビティ機能の台頭により、自動車メーカーは物理的なリコールに頼ることなく、性能、セキュリティ、機能性を高めることができるようになった。

コンポーネントに基づき、市場はソフトウェアとサービスに区分されます。2023年の市場シェアはソフトウェアが約69%と圧倒的です。OTA市場におけるソフトウェア・コンポーネントの存在感が高まっているのは、それが自動車の性能とユーザー・エクスペリエンスに直接影響を与えるからです。自動車がソフトウェア中心になるにつれ、タイムリーで効率的なアップデートの需要が急増しています。これらのアップデートは新機能を導入するだけでなく、安全性とセキュリティを確保する上でも重要な役割を果たしています。さらに、競合市場でメーカーが差別化を図る中、定期的なソフトウェア機能強化が重要なセールスポイントとなり、OTA市場におけるソフトウェア分野の需要をさらに押し上げています。

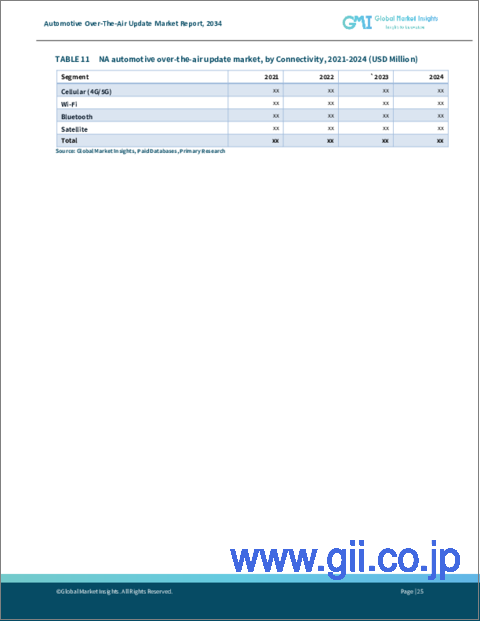

接続性に基づいて、市場はセルラー(4G/5G)、Wi-Fi、Bluetooth、衛星に分けられます。2023年、Bluetoothは約49%の市場シェアを獲得したが、これは現代の自動車に広く組み込まれていることに起因します。低消費電力やデバイスのペアリングの容易さといったBluetooth固有の利点が、メーカーにとって魅力的な選択肢となっています。自動車が機能性とセキュリティの向上のためにソフトウェアアップデートに依存するようになっている中、こうしたアップデートを効率的に促進するBluetoothの能力は、OTAエコシステムにおける重要なプレーヤーとして位置づけられています。さらに、自動車業界の技術革新が進むにつれて、将来の自動車モデルへのBluetooth技術の統合は拡大し、OTA市場での影響力はさらに強固なものとなるでしょう。

アジア太平洋地域は、急成長する自動車部門と最先端技術の迅速な導入に後押しされ、2023年には約30%の大きなシェアを獲得して世界の自動車用OTAアップデート市場をリードしました。中国や日本のような先進的な製造能力を持ち、自動車技術に多額の投資を行っている国々が牽引しています。この地域は電気自動車とスマートカーに重点を置いており、コネクテッド機能に対する需要の高まりと相まって、OTAアップデートの採用を加速させています。これらの国々がその技術的専門知識と膨大な消費者基盤を活用し続けるにつれて、アジア太平洋におけるOTA市場の成長軌道は有望に見えます。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- プラットフォームプロバイダー

- サプライヤー

- ディストリビューター/ロジスティクス

- エンドユーザー

- 利益率分析

- テクノロジーとイノベーションの展望

- 特許分析

- 主要ニュースとイニシアチブ

- 規制状況

- 影響要因

- 促進要因

- コネクテッドカーの需要と生産の増加

- 高度な自動車インフォテインメント・システムへの注目の高まり

- コネクティビティ技術の進歩

- 自律走行車に対する需要の高まり

- 業界の潜在的リスク&課題

- データ・セキュリティとプライバシーに関する問題

- 自動車のOTAアップデートに伴う高コスト

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 各社の市場シェア

- 主要市場プレーヤーの競合分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:自動車別、2021年~2032年

- 主要動向

- 乗用車

- 商用車

- 小型商用車

- 大型商用車

第6章 市場推計・予測:コンポーネント別、2021年~2032年

- 主要動向

- ソフトウェア

- ソフトウェアアップデート(SOTA)

- ファームウェアアップデート(FOTA)

- サービス

第7章 市場推計・予測:用途別、2021年~2032年

- 主要動向

- テレマティクスコントロールユニット(TCU)

- 電子制御ユニット(ECU)

- インフォテインメント

- セーフティ&セキュリティ

- その他

第8章 市場推計・予測:接続性別、2021年~2032年

- 主要動向

- セルラー(4G/5G)

- Wi-Fi

- Bluetooth

- 衛星

第9章 市場推計・予測:地域別、2021-2032年

- 主要動向:地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ニュージーランド

- 東南アジア

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- その他中東・アフリカ

第10章 企業プロファイル

- Aptiv PLC

- BlackBerry QNX Software Systems Limited

- Bosch Mobility Solutions

- Continental AG

- Digi International Inc.

- ExcelFore Technologies, Inc.

- Ficosa International S.A.

- Harman International Industries, Incorporated

- HCL Technologies

- Infineon Technologies AG

- Intel Corporation

- Mender, Inc.

- Microsoft Corporation

- Mojio

- NXP Semiconductors N.V.

- Particle Industries, Inc.

- Red Bend Software

- Sibro Technologies Inc.

- Thales Group

- Wind River Systems, Inc.

The Global Automotive Over-The-Air Update Market, valued at USD 3.8 billion in 2023, is projected to grow at a CAGR of over 17% from 2024 to 2032. The surge in demand and production of connected vehicles is a primary driver, facilitating seamless remote software and firmware updates. With the rise of advanced connectivity features in vehicles, automakers can now boost performance, security, and functionality without resorting to physical recalls.

The overall Automotive Over-The-Air (OTA) Update Market is sorted based on Offering, Deployment Mode, Organization Size, end use , and Region.

Based on components, the market is segmented into software and services. In 2023, software held a dominant market share of approximately 69%. The software component's rising prominence in the OTA market can be attributed to its direct impact on vehicle performance and user experience. As vehicles become more software-centric, the demand for timely and efficient updates has surged. These updates not only introduce new features but also play a crucial role in ensuring safety and security. Moreover, as manufacturers strive to differentiate their offerings in a competitive market, the ability to provide regular software enhancements becomes a significant selling point, further driving the demand for the software segment in the OTA landscape.

Based on connectivity, the market is divided into cellular (4G/5G), Wi-Fi, Bluetooth, and satellite. In 2023, Bluetooth captured a market share of about 49%, attributed to its prevalent integration in contemporary vehicles. Its inherent advantages, such as low power consumption and ease of device pairing, make it an attractive choice for manufacturers. As vehicles increasingly rely on software updates for enhanced functionality and security, Bluetooth's ability to facilitate these updates efficiently positions it as a key player in the OTA ecosystem. Furthermore, as the automotive industry continues to innovate, the integration of Bluetooth technology in future vehicle models is likely to expand, further solidifying its influence in the OTA market.

Asia Pacific led the global automotive OTA update market with a significant share of around 30% in 2023, fueled by its burgeoning automotive sector and swift adoption of cutting-edge technologies. Countries like China and Japan, with their advanced manufacturing capabilities and significant investments in automotive technology, are leading the charge. The region's focus on electric vehicles and smart cars, combined with a growing demand for connected features, has accelerated the adoption of OTA updates. As these nations continue to leverage their technological expertise and vast consumer base, the growth trajectory for the OTA market in Asia Pacific looks promising.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2032

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Platform providers

- 3.2.2 Suppliers

- 3.2.3 Distributors/ Logistics

- 3.2.4 End user

- 3.3 Profit margin analysis

- 3.4 Technology and innovation landscape

- 3.5 Patent analysis

- 3.6 Key news and initiatives

- 3.7 Regulatory landscape

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Increasing demand and production of connected vehicles

- 3.8.1.2 Rising emphasis on advanced car infotainment systems

- 3.8.1.3 Growing advancements in the connectivity technology

- 3.8.1.4 Rising demand for autonomous vehicles

- 3.8.2 Industry pitfalls and challenges

- 3.8.2.1 Issues related to data security and privacy

- 3.8.2.2 High cost involved in automotive OTA updates

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2023

- 4.1 Introduction

- 4.2 Company market share

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Vehicle, 2021-2032 ($Bn)

- 5.1 Key trends

- 5.2 Passenger vehicles

- 5.3 Commercial vehicles

- 5.3.1 Light commercial vehicles

- 5.3.2 Heavy commercial vehicles

Chapter 6 Market Estimates and Forecast, By Component, 2021-2032 ($Bn)

- 6.1 Key trends

- 6.2 Software

- 6.2.1 Software updates (SOTA)

- 6.2.2 Firmware updates (FOTA)

- 6.3 Services

Chapter 7 Market Estimates and Forecast, By Application, 2021-2032 ($Bn)

- 7.1 Key trends

- 7.2 Telematics control unit (TCU)

- 7.3 Electronic control unit (ECU)

- 7.4 Infotainment

- 7.5 Safety and security

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Connectivity, 2021-2032 ($Bn)

- 8.1 Key trends

- 8.2 Cellular (4G/5G)

- 8.3 Wi-Fi

- 8.4 Bluetooth

- 8.5 Satellite

Chapter 9 Market Estimates and Forecast, By Region, 2021-2032 ($Bn)

- 9.1 Key trends, by region

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.3.8 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.4.7 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

- 9.6.4 Rest of MEA

Chapter 10 Company Profiles

- 10.1 Aptiv PLC

- 10.2 BlackBerry QNX Software Systems Limited

- 10.3 Bosch Mobility Solutions

- 10.4 Continental AG

- 10.5 Digi International Inc.

- 10.6 ExcelFore Technologies, Inc.

- 10.7 Ficosa International S.A.

- 10.8 Harman International Industries, Incorporated

- 10.9 HCL Technologies

- 10.10 Infineon Technologies AG

- 10.11 Intel Corporation

- 10.12 Mender, Inc.

- 10.13 Microsoft Corporation

- 10.14 Mojio

- 10.15 NXP Semiconductors N.V.

- 10.16 Particle Industries, Inc.

- 10.17 Red Bend Software

- 10.18 Sibro Technologies Inc.

- 10.19 Thales Group

- 10.20 Wind River Systems, Inc.