|

市場調査レポート

商品コード

1928898

貯湯式給湯器市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測Storage Water Heater Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 貯湯式給湯器市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2026年01月07日

発行: Global Market Insights Inc.

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

概要

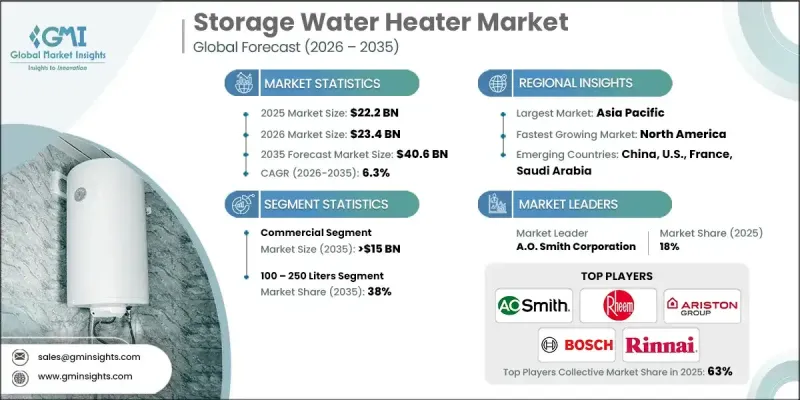

世界の貯湯式給湯器市場は、2025年に222億米ドルと評価され、2035年までにCAGR6.3%で成長し、406億米ドルに達すると予測されています。

成長は、優れた断熱材、よりスマートな制御システム、大容量ユニットの性能と使いやすさを向上させる効率的な熱交換器設計などの技術進歩によって推進されています。採用の増加は、より厳格な国内および国際的なエネルギー効率基準、ならびに持続可能な給湯ソリューションへの投資増加によってさらに支えられています。企業は、企業の持続可能性目標を達成するために、エネルギー効率に優れ、環境に優しい給湯器を優先しています。一方、政府のインセンティブ、リベート、税額控除は、商業施設および住宅のアップグレードを促進しています。スマートグリッドや太陽熱・地熱システムなどの再生可能エネルギー源との統合により、エネルギー使用の最適化、コスト削減、化石燃料への依存度低減が可能となります。都市化、生活水準の向上、新興市場における電化が進むことで導入がさらに促進され、貯湯式給湯器は住宅用・商業用双方において不可欠な存在として位置づけられています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 222億米ドル |

| 予測金額 | 406億米ドル |

| CAGR | 6.3% |

住宅セグメントは、家庭のエネルギー需要の増加と日常使用における信頼性の高い給湯の必要性により、2035年までにCAGR5.5%で成長すると予測されています。強化された断熱材、スマートサーモスタット、家庭用エネルギーシステムとの統合を備えた省エネモデルは、利便性と性能を向上させながら光熱費を削減しています。

30リットルカテゴリーは、小規模世帯、アパート、スペースに制約のある地域で好まれることから、2035年までに40億米ドルに達すると予測されています。これらのユニットは、迅速な加熱と限定的な給湯需要が一般的なキッチンやバスルームなどの使用地点での用途に最適です。成長は、都市化の進展、コンパクト住宅の動向、手頃な価格、新興経済国における電化拡大によって支えられています。

米国貯湯式給湯器市場は2025年に30億米ドル規模に達し、エネルギー貯蔵との統合や再生可能エネルギープロジェクトへの積極的な投資が成長を牽引しています。信頼性が高く持続可能な給湯ソリューションへの需要を背景に、太陽光発電と蓄電システムの組み合わせの導入が増加しています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界のエコシステム

- 原材料の入手可能性と調達分析

- 製造能力評価

- サプライチェーンのレジリエンスとリスク要因

- 流通ネットワーク分析

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- 価格動向分析

- 容量別

- 地域別

- コスト構造分析

- ポーターの分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- PESTEL分析

- 新たな機会と動向

- デジタル化とIoT統合

- 新興市場への進出

- 投資分析と将来展望

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ユーラシア

- CIS

- 中東・アフリカ

- ラテンアメリカ

- 戦略的ダッシュボード

- 戦略的取り組み

- イノベーションと技術動向

第5章 市場規模・予測:容量別、2023-2035

- 30リットル未満

- 30~100リットル

- 100~250リットル

- 250~400リットル

- 400リットル超

第6章 市場規模・予測:エネルギー源別、2023-2035

- 電気

- ガス

第7章 市場規模・予測:用途別、2023-2035

- 住宅用

- 商業用

- カレッジ・高等教育機関

- オフィス

- 政府・軍事

- その他

第8章 市場規模・予測:地域別、2023-2035

- 北米

- 米国

- カナダ

- 欧州

- 英国

- フランス

- ドイツ

- イタリア

- オーストリア

- スペイン

- オランダ

- デンマーク

- フィンランド

- スウェーデン

- ノルウェー

- アジア太平洋地域

- 中国

- 日本

- 韓国

- インド

- オーストラリア

- インドネシア

- マレーシア

- シンガポール

- タイ

- ニュージーランド

- フィリピン

- ベトナム

- ユーラシア

- ロシア

- ベラルーシ

- カザフスタン

- キルギス

- アルメニア

- CIS

- アゼルバイジャン

- モルドバ

- タジキスタン

- トルクメニスタン

- ウズベキスタン

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- クウェート

- オマーン

- トルコ

- 南アフリカ

- ナイジェリア

- エジプト

- イスラエル

- イラク

- ラテンアメリカ

- ブラジル

- アルゼンチン

- チリ

- メキシコ

第9章 企業プロファイル

- A.O. Smith

- Ariston Holding N.V.

- Bosch Thermotechnology Ltd.

- Bradford White Corporation, USA

- Essency

- Ferroli S.p.A

- Groupe Atlantic

- Havells India Ltd.

- Hubbell Heaters

- Haier Inc.

- Jaquar India

- Linuo Ritter International Co., Ltd.

- Nihon Itomic Co., Ltd.

- Rheem Manufacturing Company

- Rinnai America Corporation

- State Industries.

- Saudi Ceramics Company

- Viessmann

- Vaillant

- Whirlpool Corporation