|

市場調査レポート

商品コード

1766309

産業用温水器の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Industrial Water Heater Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 産業用温水器の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年06月12日

発行: Global Market Insights Inc.

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

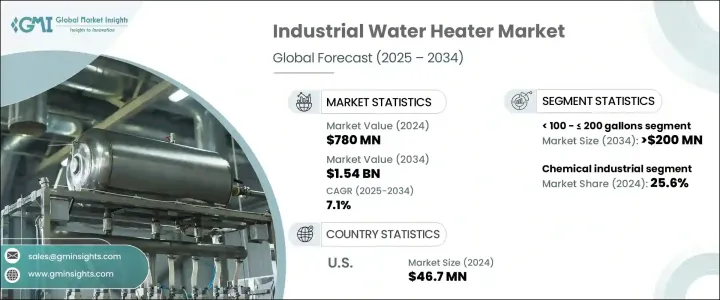

産業用温水器の世界市場規模は7億8,000万米ドルで、CAGR 7.1%で成長し、2034年には15億4,000万米ドルに達すると予測されています。

この成長を牽引しているのは、エネルギー効率の高いシステムに対するニーズの高まりと、産業用エネルギー消費の増加です。この上昇動向は、排出量削減や厳しいエネルギー規制への対応に向けた世界の取り組みに沿った、持続可能でコスト効率の高い加熱ソリューションへの幅広い業界のシフトを反映しています。

産業オペレーションは急速に進化しており、メーカーはより信頼性の高い高度な給湯技術を採用するよう求められています。安定した性能を提供するだけでなく、操業停止時間を短縮するシステムに対する需要の急増が顕著です。このような進歩は、操業効率を維持しながらエネルギー使用を最適化することに重点を置く産業にとって特に重要です。高度な熱エネルギー技術を特徴とする洗練された給湯器は現在、旧式のシステムに取って代わり、環境への影響を低減し、全体的なエネルギー管理を改善しています。自動化された産業プロセスが重視されるようになったことも需要増に寄与しており、予知保全やAI主導の温度制御といったスマート機能が運転の柔軟性を高めています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 7億8,000万米ドル |

| 予測金額 | 15億4,000万米ドル |

| CAGR | 7.1% |

製造施設におけるデジタルインフラ統合の進展が、最新の給湯機器の採用をさらに後押ししています。インダストリー4.0の革新は、産業用暖房の情勢を再構築し、施設がメンテナンス要件を予測し、予期せぬ故障を回避することを可能にしています。この進化は単に性能を向上させるだけでなく、特に季節的または変動する処理需要に対応する施設にとっては、拡張性のあるオペレーションをサポートすることでもあります。

容量別に、産業用温水器市場は3つの主要カテゴリーに区分されます。100~200ガロン未満、200~500ガロン、 そして、500ガロン以上。このうち、100から200ガロン未満の容量のシステムが広く注目を集めており、その市場は2034年までに2億米ドルを超えると予測されています。これらのユニットは、柔軟でモジュール式の加熱ソリューションを必要とする場面で採用されることが多くなっています。コンパクトな設置面積、エネルギー効率の向上、スマートテクノロジーとの互換性により、さまざまな産業用途に適しています。

この分野の市場成長は、従来の燃料ベースのシステムから、性能を損なうことなく高効率を実現する最新の環境に優しい代替品への移行に大きく起因しています。

用途に基づき、市場はパルプ・製紙、食品加工、金属・鉱業、化学、精製など、いくつかの産業に分けられます。このうち、2024年に最も高いシェアを占めたのは化学産業で、市場全体の25.6%を占めています。この優位性は、過酷な化学環境に耐える耐腐食性高性能ヒーターへの一貫した需要が後押ししています。

化学処理部門ではエネルギーの最適化が優先されるため、高効率の給湯器は過酷な運転条件下での信頼性とプロセスの安定性を確保するために不可欠です。

地域別では、米国が引き続き産業用温水器の採用で一貫した成長を示しています。米国の市場規模は2022年に3,550万米ドル、2023年には4,370万米ドルに増加し、2024年には4,670万米ドルに達しました。この成長は主に、省エネルギーに焦点を当てた規制の義務化と、高効率機器への投資を奨励する有利な税制規定によって支えられています。

産業用温水器市場の競合情勢を積極的に形成している著名企業には、Ariston Group、A.O. Smith、Bradford White Corporation、FLEXIHEAT UK、Eemax、Hevac、Jaguar India、Hubbell Heaters、Lochinvar、Thermex Corporation、Sioux Corporation、Thermotech Systems、Herambh Coolingz、Viessmann、Andrewsなどがあります。これらの企業は、持続可能でスマート、かつ耐久性のある給湯ソリューションに対する世界の需要の高まりに対応するため、絶えず技術革新を行っています。製品開発、スマート技術の統合、新興国市場への進出に注力しており、予測期間中も競争力学に影響を与え続けると予想されます。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 戦略的ダッシュボード

- 戦略的取り組み

- 競合ベンチマーキング

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:容量別、2021年~2034年

- 主要動向

- 100~200ガロン未満

- 200~500ガロン

- 500ガロン以上

第6章 市場規模・予測:燃料別、2021年~2034年

- 主要動向

- 電気

- ガス

- その他

第7章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- 食品加工

- パルプ・紙

- 化学薬品

- 製油所

- 金属・鉱業

- その他

第8章 市場規模・予測:販売チャネル別、2021年~2034年

- 主要動向

- オンライン

- ディーラー

- 小売り

第9章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- フランス

- 英国

- イタリア

- スペイン

- ポルトガル

- ルーマニア

- オランダ

- スイス

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- エジプト

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

第10章 企業プロファイル

- A.O. Smith

- Andrews

- Ariston Group

- Bradford White Corporation

- Eemax

- FLEXIHEAT UK

- Herambh Coolingz

- Hevac

- Hubbell Heaters

- Jaguar India

- Lochinvar

- Sioux Corporation

- Thermex Corporation

- Thermotech Systems

- Viessmann

The Global Industrial Water Heater Market was valued at USD 780 million and is estimated to grow at a CAGR of 7.1% to reach USD 1.54 billion by 2034. The growth is driven by the rising need for energy-efficient systems and increased industrial energy consumption. This upward trend reflects a broader industry shift toward sustainable and cost-effective heating solutions that align with global efforts to reduce emissions and comply with stringent energy regulations.

Industrial operations are evolving rapidly, prompting manufacturers to adopt more reliable and advanced water heating technologies. There is a noticeable demand surge for systems that not only deliver consistent performance but also reduce operational downtime. These advancements are especially relevant for industries focused on optimizing their energy use while maintaining operational efficiency. Sophisticated water heaters featuring advanced thermal energy technologies are now replacing older systems, reducing environmental impact and improving overall energy management. The growing emphasis on automated industrial processes is also contributing to the rise in demand, with smart features like predictive maintenance and AI-driven temperature control enhancing operational flexibility.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $780 Million |

| Forecast Value | $1.54 Billion |

| CAGR | 7.1% |

The increasing integration of digital infrastructure in manufacturing facilities is further supporting the adoption of modern water heating equipment. Industry 4.0 innovations are reshaping industrial heating landscapes, enabling facilities to anticipate maintenance requirements and avoid unexpected failures. This evolution is not just about improving performance but also about supporting scalable operations, especially for facilities dealing with seasonal or fluctuating processing demands.

By capacity, the industrial water heater market is segmented into three key categories: 100 to <= 200 gallons, > 200 to <= 500 gallons, and > 500 gallons. Among these, systems with capacities ranging from 100 to <= 200 gallons are gaining widespread attention, and their market is projected to exceed USD 200 million by 2034. These units are increasingly being adopted in settings that require flexible and modular heating solutions. Their compact footprint, enhanced energy efficiency, and compatibility with smart technologies make them suitable for various industrial applications. The market's growth in this segment is largely attributed to the transition from traditional fuel-based systems to modern, environmentally friendly alternatives that deliver high efficiency without compromising performance.

Based on application, the market is divided into several industries, including pulp and paper, food processing, metal and mining, chemicals, refinery, and others. Among these, the chemical industry accounted for the highest share in 2024, representing 25.6% of the total market. This dominance is fueled by a consistent demand for corrosion-resistant, high-performance heaters that can withstand aggressive chemical environments. The chemical processing sector prioritizes energy optimization, making high-efficiency water heaters essential for ensuring reliability and process stability in harsh operating conditions.

Regionally, the United States continues to demonstrate consistent growth in industrial water heater adoption. The market in the U.S. was valued at USD 35.5 million in 2022, increased to USD 43.7 million in 2023, and reached USD 46.7 million in 2024. This growth is primarily supported by regulatory mandates focused on energy conservation, as well as favorable tax provisions that encourage investments in high-efficiency equipment. Additionally, federal initiatives designed to reduce emissions from industrial facilities have further fueled the replacement of outdated systems with advanced heating solutions.

Prominent companies actively shaping the competitive landscape of the industrial water heater market include Ariston Group, A.O. Smith, Bradford White Corporation, FLEXIHEAT UK, Eemax, Hevac, Jaguar India, Hubbell Heaters, Lochinvar, Thermex Corporation, Sioux Corporation, Thermotech Systems, Herambh Coolingz, Viessmann, and Andrews. These players are constantly innovating to meet the growing demand for sustainable, smart, and durable water heating solutions across global industries. Their focus on product development, integration of smart technologies, and expansion into emerging markets is expected to continue influencing the competitive dynamics over the forecast period.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, 2024

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Capacity, 2021 - 2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 < 100 - ≤ 200 gallons

- 5.3 > 200 - ≤ 500 gallons

- 5.4 > 500 gallons

Chapter 6 Market Size and Forecast, By Fuel, 2021 - 2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Electric

- 6.3 Gas

- 6.4 Others

Chapter 7 Market Size and Forecast, By Application, 2021 - 2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 Food processing

- 7.3 Pulp & paper

- 7.4 Chemical

- 7.5 Refinery

- 7.6 Metal & mining

- 7.7 Others

Chapter 8 Market Size and Forecast, By Sales Channel, 2021 - 2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 Online

- 8.3 Dealer

- 8.4 Retail

Chapter 9 Market Size and Forecast, By Region, 2021 - 2034 (USD Million & Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 France

- 9.3.3 UK

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Portugal

- 9.3.7 Romania

- 9.3.8 Netherlands

- 9.3.9 Switzerland

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Middle East & Africa

- 9.5.1 Saudi Arabia

- 9.5.2 UAE

- 9.5.3 Egypt

- 9.5.4 South Africa

- 9.6 Latin America

- 9.6.1 Brazil

- 9.6.2 Argentina

Chapter 10 Company Profiles

- 10.1 A.O. Smith

- 10.2 Andrews

- 10.3 Ariston Group

- 10.4 Bradford White Corporation

- 10.5 Eemax

- 10.6 FLEXIHEAT UK

- 10.7 Herambh Coolingz

- 10.8 Hevac

- 10.9 Hubbell Heaters

- 10.10 Jaguar India

- 10.11 Lochinvar

- 10.12 Sioux Corporation

- 10.13 Thermex Corporation

- 10.14 Thermotech Systems

- 10.15 Viessmann