|

市場調査レポート

商品コード

1913322

利用ベース保険市場の機会、成長促進要因、産業動向分析、2026年~2035年の予測Usage-based Insurance (UBI) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 利用ベース保険市場の機会、成長促進要因、産業動向分析、2026年~2035年の予測 |

|

出版日: 2025年12月30日

発行: Global Market Insights Inc.

ページ情報: 英文 235 Pages

納期: 2~3営業日

|

概要

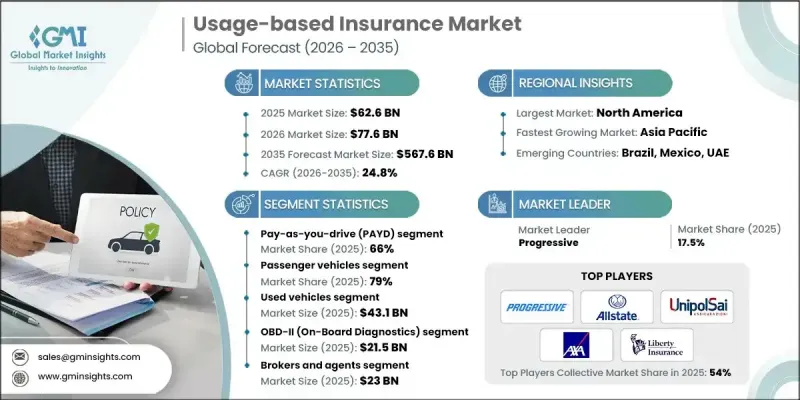

世界の利用ベース保険(UBI)市場は、2025年に626億米ドルと評価され、2035年までにCAGR24.8%で成長し、5,676億米ドルに達すると予測されています。

この急速な成長は、保険リスクの評価および価格設定方法における根本的な変化を反映しています。保険会社は、固定的な保険料モデルから、実際の使用状況とコストをより適切に連動させる動的で行動連動型の価格設定構造へと移行しつつあります。この堅調な成長は、コネクテッドモビリティソリューションの普及拡大、パーソナライズされた保険商品に対する消費者の嗜好の高まり、および分析主導の引受業務の広範な受容によって支えられています。利用ベース保険は、保険料を実際の利用パターンに連動させることで、保険会社が価格設定の精度向上、リスクエクスポージャーの最適化、顧客関係の強化を実現することを可能にします。データ中心のプラットフォームが保険契約ライフサイクル全体における透明性、柔軟性、エンゲージメントを向上させるため、デジタル保険エコシステムへの移行が導入をさらに加速させています。こうした構造的変化により、利用ベース保険は引き続き世界の保険業界における中核的な成長分野としての地位を確立しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 626億米ドル |

| 予測金額 | 5,676億米ドル |

| CAGR | 24.8% |

技術進歩により、継続的なデータ収集、リアルタイムのリスク評価、自動化された保険契約管理が可能となり、市場は再構築されています。デジタル監視システムと高度な分析プラットフォームにより、保険会社は運転行動をより正確に評価し、価格設定モデルを動的に調整することが可能となりました。この技術基盤は、変化する消費者の移動パターンに対応する拡張可能な保険モデルを支えています。使用量連動型保険構造の採用増加、データ駆動型価格設定に対する規制の開放性拡大、使用量や行動に直接連動する保険ソリューションに対する消費者の認識向上により、市場拡大はさらに強化されています。

走行距離連動型保険セグメントは2025年に66%のシェアを占め、2026年から2035年にかけてCAGR24.7%超で成長すると予測されています。その優位性は、導入の簡便さ、透明性の高い価格設定ロジック、実際の車両使用量に応じたコスト調整を求めるドライバー層への強い訴求力によって支えられています。

乗用車セグメントは2025年に79%のシェアを占め、2035年までCAGR25.1%で成長すると見込まれています。このセグメントは、幅広い被保険者基盤と、個人の運転習慣や使用頻度を反映したパーソナライズド保険構造との高い適合性から恩恵を受けています。

米国における利用ベース保険(UBI)市場は2025年に78%のシェアを占め、200億米ドルの規模に達しました。同地域は確立された保険エコシステム、デジタル技術の普及、データ活用型保険プラットフォームの先進的な導入といった利点を有しています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- コネクテッドカーおよびテレマティクスインフラの急速な成長

- パーソナライズされた使用量連動型保険料金設定への需要の高まり

- AI、機械学習、データ分析の進歩

- 保険業界のデジタルトランスフォーメーションと規制当局の受容

- 業界の潜在的リスク&課題

- データプライバシーとサイバーセキュリティに関する懸念事項

- 行動モニタリングに対する顧客の抵抗感

- 市場機会

- テレマティクス対応保険の導入拡大:

- 導入および統合コストの高さ

- データ精度と標準化に関する課題

- 自動車メーカーおよび技術プロバイダーとの提携

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 米国保険監督官協会(NAIC)ガイドライン

- 州保険局の規制

- カナダOSFI及び州保険ガイドライン

- 欧州

- ドイツBaFin規制

- フランスACPRおよびCNILガイドライン

- 英国金融行動監視機構(FCA)及び一般データ保護規則(GDPR)への準拠

- イタリア保険監督庁(IVASS)ガイドライン

- アジア太平洋地域

- 中国銀行保険監督管理委員会(CBIRC)ガイドライン

- 日本金融庁のコンプライアンス

- 韓国金融監督院(FSS)の規制

- インド保険規制開発庁(IRDAI)ガイドライン

- ラテンアメリカ

- ブラジルSUSEPガイドライン

- メキシコCNSFガイドライン

- 中東・アフリカ

- アラブ首長国連邦保険庁ガイドライン

- サウジアラビア中央銀行(SAMA)規制

- 北米

- ポーター分析

- PESTEL分析

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- コスト内訳分析

- 特許分析

- 持続可能性と環境的側面

- 持続可能な実践

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に配慮した取り組み

- カーボンフットプリントに関する考慮事項

- 使用事例シナリオ

- アクチュアリーモデリング及びリスクスコアリングフレームワーク

- 使用量ベースのリスク変数と重み付けメカニズム

- 運転行動スコアリング調査手法

- アクチュアリー意思決定におけるAI/MLの統合

- 損害率と保険金請求の影響分析

- 顧客の採用状況と行動経済学分析

- データ所有権、収益化及びプライバシー経済学

- OEM、通信事業者、プラットフォームとの提携モデル

- 導入モデルと運用アーキテクチャ

- 製品の差別化と機能ベンチマーク

- 主要UBIサービスにおける機能比較

- 価格設定、割引構造、および報酬モデル

- 保険会社間の差別化戦略

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 事業拡大計画と資金調達

第5章 市場推計・予測:パッケージ別、2022-2035

- 運転行動連動型(PHYD)

- 走行距離連動型(PAYD)

- デバイスベース

- テレマティクスベース

- 運転方法管理(MHYD)

第6章 市場推計・予測:車両別、2022-2035

- 乗用車

- OBD-II

- ブラックボックス

- スマートフォン

- 組み込みテレマティクス

- 商用車

- 小型商用車(LCV)

- OBD-II

- ブラックボックス

- スマートフォン

- 組み込みテレマティクス

- 中型商用車(MCV)

- OBD-II

- ブラックボックス

- スマートフォン

- 組み込みテレマティクス

- 大型商用車(HCV)

- OBD-II

- ブラックボックス

- スマートフォン

- 組み込みテレマティクス

- 小型商用車(LCV)

第7章 市場推計・予測:技術別、2022-2035

- OBD-II

- ブラックボックス

- スマートフォン

- 組み込みテレマティクス

第8章 市場推計・予測:車齢別、2022-2035

- 新車

- 中古車

第9章 市場推計・予測:流通チャネル別、2022-2035

- ブローカーおよび代理店

- 直接販売

- オンラインプラットフォーム

- バンカシュアランス

第10章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ベルギー

- オランダ

- スウェーデン

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- シンガポール

- 韓国

- ベトナム

- インドネシア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ地域

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第11章 企業プロファイル

- 世界企業

- Allianz

- Allstate

- AXA

- Liberty Mutual Insurance

- Metromile

- Octo Group

- Progressive

- State Farm Mutual Automobile Insurance Company

- UNIPOLSAI ASSICURAZIONI

- Zurich Insurance

- 地域企業

- Aviva

- Chubb

- Direct Line Insurance

- Generali

- ICICI Lombard

- MAPFRE

- RSA Insurance

- Sompo

- Suncorp

- Tokio Marine

- 新興企業

- By Miles

- Cuvva

- Noblr

- Sureify

- Zego