|

市場調査レポート

商品コード

1822644

病院情報システムの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Hospital Information System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 病院情報システムの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年08月29日

発行: Global Market Insights Inc.

ページ情報: 英文 155 Pages

納期: 2~3営業日

|

概要

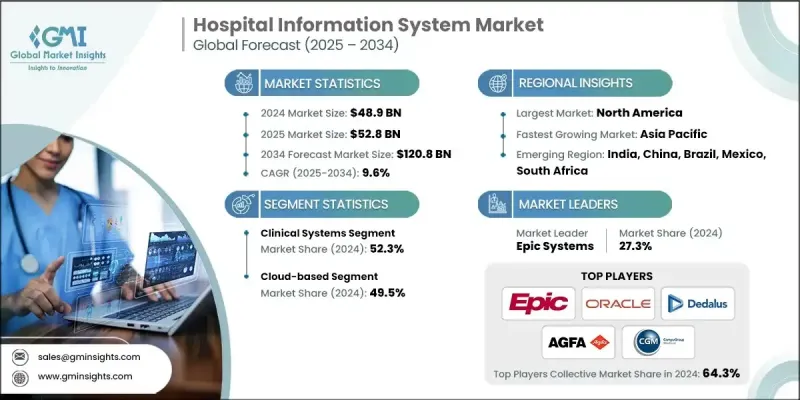

Global Market Insights, Inc.が発行した最新レポートによると、世界の病院情報システム(HIS)市場は2024年に489億米ドルと評価され、2025年の528億米ドルから2034年までには1,208億米ドルに成長し、CAGR9.6%で拡大すると予測されています。

ヘルスケアのデジタル化の進展、相互運用可能なソリューションへの要求の高まり、臨床ワークフローの最適化へのニーズの高まりが、世界中でHISの採用を促進しています。病院は、患者記録、臨床情報、医療費請求、規制遵守を扱う統合ソフトウェアシステムを選択する傾向が強まっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 489億米ドル |

| 予測金額 | 1,208億米ドル |

| CAGR | 9.6% |

主な促進要因

1.臨床データと管理データの統合管理への要求:病院は、部門間で異なるワークフローを統合するためにHISを導入しています。

2.慢性疾患の増加と高齢化:効果的な患者追跡と最適化された治療には、高度な医療情報プラットフォームが必要です。

3.クラウドとAIベースのシステムの採用:ITインフラ費用の削減、柔軟性、リモートアクセスにより、クラウドの採用が普及しています。

4.コンプライアンスとデータセキュリティ:国際的および地域的な規制により、病院はコンプライアンスに準拠し、安全で監査可能なシステムの導入を余儀なくされています。

主要企業

- Epicは2024年の市場シェア27.3%で病院情報システム市場を独占しました。

- Oracleは、Cernerの確立されたHIS/EHRの地位を買収し、クラウドコンピューティング、データ分析、AIにおけるそれぞれの強みを活かしています。

- Dedalusは、相互運用性とオープンデジタルヘルスエコシステムに強い関心を持つ欧州市場のリーダーです。

主な課題

- 相互運用性の制約:レガシーシステム、検査室、画像処理、サードパーティプラットフォームとのHIS統合は引き続き課題となっています。

- 高いトレーニングと導入費用:カスタマイズ、移行、従業員へのオンボーディングの投資は高額になる可能性があります。

- セキュリティとデータ・プライバシーの脅威:医療データ流出やランサムウェアに対する懸念の高まりが、コンプライアンスと安全なクラウド導入の推進につながっています。

1.システムコンポーネント別-臨床システムが増加傾向

2024年のHIS市場では、臨床システムコンポーネントが約66%で最大のシェアを占めています。EMR、CPOE、LIS、RISに代表される臨床システムコンポーネントは、日々の病院業務の根幹を支える働き者です。

2.展開別-クラウドベースのソリューションが台頭

クラウドベースのHISの導入は、拡張性の向上、インフラをサポートするための資本支出の削減、リモートアプリケーションへのアクセスの増加により加速しています。各地域の病院は、業務、コラボレーション、継続的ケアの改善を目的にクラウドソリューションを導入しています。

3.地域別-北米が好調を維持

北米は、政府の強力な支援、非常に高いデジタルリテラシー、公立病院と私立病院の両方における強力な導入により、2024年も引き続き最大の市場シェアを維持し、リードを保っています。北米は、強力なヘルスケアインフラ、EHRの普及、HIPAAやHITECHなどの政府規制、クラウドベースの医療ITソリューションの存在感の高まりにより、病院情報システム市場における優位性を維持しています。米国の病院や医療ネットワークは、臨床意思決定支援、集団健康分析、遠隔ケアモジュールを病院の基幹システムに迅速に統合しています。

病院情報システム市場の主要企業としては、AGFA Healthcare、CAMBIO、ChipSoft、CompuGroup Medical、Dedalus、Docaposte、Engineering Ingegneria Informatica、Epic Systems、InterSystems、Meierhofer AG、NextGen、Nexus、Oracle、SECTRA、Veradigmなどが挙げられます。

同市場の主要HIS企業は、クラウド統合、他地域への進出、AI対応モジュール、ヘルスケアリーダーとの協業契約を採用し、競争力を高めています。DedalusとInterSystemsは、クラウドプラットフォームを成長させ、相互運用機能を追加しています。CompuGroup MedicalとAGFA Healthcareは、意思決定支援機能をHISプラットフォームに統合しています。OracleはCerner買収後、統合クラウドとデータ分析機能を取り入れ、最終的にEHRとポピュレーションヘルスにより価値あるモジュールを作り出そうとしています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- 業界への影響要因

- 成長促進要因

- デジタルヘルスソリューションの導入拡大

- 政府の取り組みと規制

- ヘルスケア費の増加

- 統合ヘルスケアシステムへの需要の高まり

- 業界の潜在的リスク・課題

- 実装と保守のコストが高め

- データセキュリティとプライバシーに関する懸念

- 市場機会

- 政府のヘルスケアデジタル化イニシアチブの増加

- 分析・ビジネスインテリジェンスツールの需要の高まり

- 成長促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- 技術的情勢

- 現在の技術動向

- 新興技術

- 将来の市場動向

- 消費者行動と動向

- 地域別病院数

- 病院デジタルエコシステムの概要

- 電子医療記録(EMR)/電子健康記録(EHR)

- 遠隔医療と遠隔患者モニタリング

- サイバーセキュリティとデータ保護

- ポーター分析

- PESTEL分析

- EMRへのAIの統合

- ギャップ分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業の市場シェア分析

- グローバル

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ、中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:システムコンポーネント別、2021年~2034年

- 主要動向

- 臨床システム

- 電子医療記録(EMR)/電子健康記録(EHR)

- 放射線情報システム(RIS)

- 薬局情報システム

- 検査情報システム(LIS)

- その他の臨床システム

- 管理/バックオフィスシステム

- 財務と請求

- サプライチェーンマネジメント

- 施設管理・人事

- 運用システム

- 入院・退院・転院(ADT)/ベッド管理システム(BMS)

- 運用標準サポート/スケジュールシステム

- 患者向けテクノロジー

- モバイルヘルスアプリケーション

- 患者ポータル

- 統合層

- インターフェースエンジン/API

- 医療情報交換(HIE)

- データとセキュリティ

- 臨床データリポジトリ

- アイデンティティとアクセス管理(IAM)

- 一般データ保護規則(GDPR)

第6章 市場推計・予測:展開別、2021年~2034年

- 主要動向

- クラウドベース

- ウェブベース

- オンプレミス

第7章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第8章 企業プロファイル

- AGFA Healthcare

- CAMBIO

- ChipSoft

- CompuGroup Medical

- Dedalus

- Docaposte

- Engineering Ingegneria Informatica

- Epic Systems

- InterSystems

- Meierhofer AG

- NextGen

- Nexus

- Oracle

- SECTRA

- Veradigm