|

|

市場調査レポート

商品コード

1699381

高周波高速銅張積層板市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測High Frequency High Speed Copper Clad Laminate (CCL) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 高周波高速銅張積層板市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月26日

発行: Global Market Insights Inc.

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

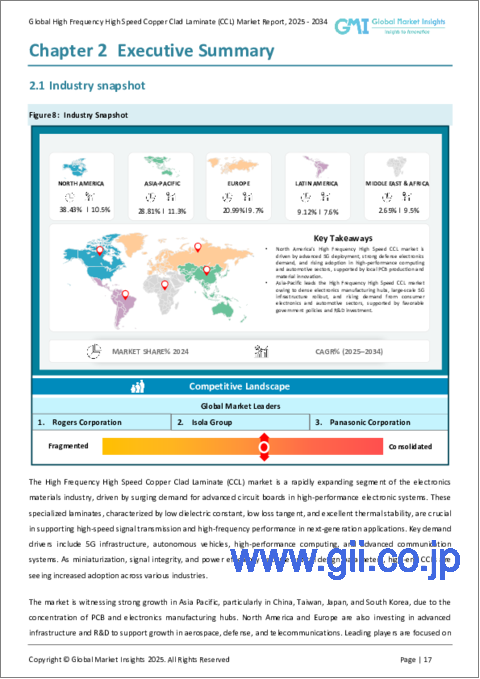

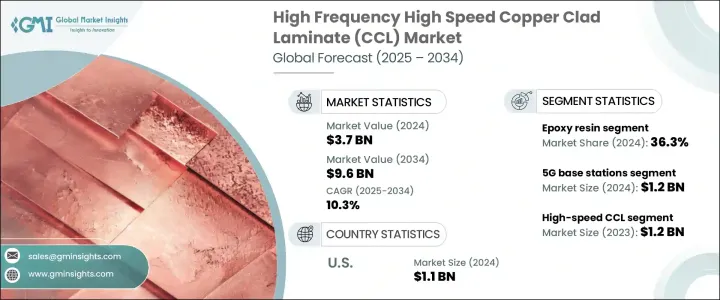

世界の高周波高速銅張積層板市場は、2024年に37億米ドルに達し、2025年から2034年にかけてCAGR 10.3%の堅調な成長が見込まれています。

この成長は、5G技術の急速な採用と、様々な産業における高度な電子機器に対する需要の急増が大きな要因となっています。高速データ・トランスミッションやコネクティビティ強化のニーズが高まる中、メーカーは高周波・高速CCLなどの高性能材料への依存度を高めています。これらのラミネートは、最新の電子機器、通信インフラ、高速コンピューティング・システムに電力を供給するプリント回路基板の生産において重要な役割を果たしています。

人工知能、モノのインターネット(IoT)、自律走行車の統合が進むにつれ、効率的で高速な電子部品への需要がさらに高まっています。データ処理のニーズが進化するにつれ、産業界は堅牢で信頼性の高い回路材料を必要とする次世代技術に注力しています。加えて、コンパクトで軽量、エネルギー効率の高いデバイスへのシフトは、メーカーに材料構成の革新の機会をもたらし、銅張積層板の熱抵抗やシグナル・インテグリティ、全体的なパフォーマンスを向上させています。半導体の進歩とワイヤレス・コミュニケーション・ネットワークへの大きな投資により、高周波・高速CCL市場は今後数年で大きく拡大するものと思われます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 37億米ドル |

| 予測金額 | 96億米ドル |

| CAGR | 10.3% |

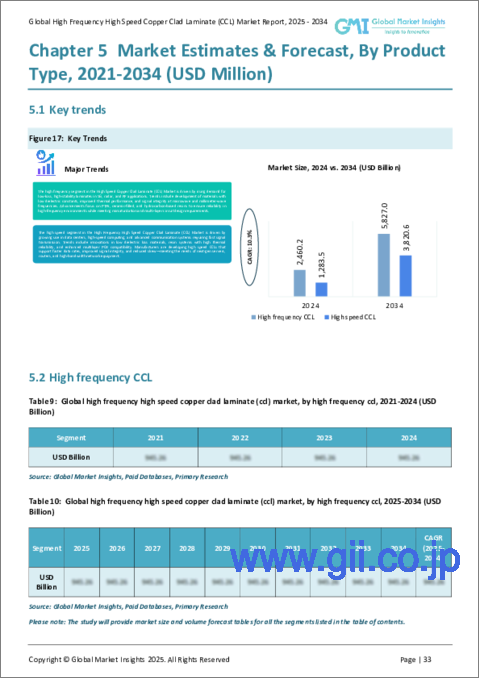

市場は主に高周波CCLと高速CCLに分類され、2024年には25億米ドルに達する高周波セグメントが優位を占めると予測されます。高度通信インフラへの依存度の高まりと、中断のない高速データフローへのニーズの高まりが、高周波CCLの需要を促進しています。通信や家電などの業界では、より高速で信頼性の高い電子部品へのシフトがかつてないほど進んでおり、こうした積層板の採用がさらに加速しています。

樹脂の種類でいえば、高周波高速銅張積層板(CCL)市場はフェノール樹脂、エポキシ樹脂、ポリイミド樹脂、ビスマレイミド・トリアジン(BT)樹脂に区分されます。エポキシ樹脂セグメントは2024年に36.3%の市場シェアを占め、その優れた性能特性とPCBの構造的完全性を高める能力が牽引しています。エポキシ樹脂の配合の進歩は、銅張積層板の耐久性、熱安定性、電気的性能を向上させ、PCBメーカーに好まれています。

米国の高周波高速銅張積層板(CCL)市場は、5Gインフラの急速な展開、エレクトロニクスの普及、自動車産業の拡大などに後押しされ、 2024年には11億米ドルに達すると予測されています。よりスマートで効率的な電子機器への要求が高まり続けるなか、高周波・高速CCLのような高性能素材へのニーズは複数のセクターで拡大し、将来のデジタルトランスフォーメーションにおける重要な役割を強化することになるでしょう。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

- 1次データ

- 二次資料

- 有料情報源

- 公的情報源

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- 破壊

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュース

- 規制状況

- 影響要因

- 促進要因

- 5G技術の需要拡大

- 電子機器需要の増加

- 家電需要の急増

- 航空宇宙・防衛技術の進歩

- 業界の潜在的リスク&課題

- 生産プロセスの高コスト

- 厳しい環境規制への対応

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- 高周波CCL

- 高速CCL

第6章 市場推計・予測:樹脂タイプ別、2021年~2034年

- 主要動向

- エポキシ樹脂

- フェノール樹脂

- ポリイミド樹脂

- ビスマレイミド・トリアジン(BT)樹脂

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 5G基地局

- カーエレクトロニクス

- 家電

- スマートフォン

- タブレット

- ノートパソコン

- 通信機器

- ルーター

- スイッチ

- アンテナ

- 航空宇宙・防衛

- レーダーシステム

- 通信システム

- その他

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- AGC Inc.(Asahi Glass Co., Ltd.)

- Arlon Electronic Materials

- Doosan Corporation Electro-Materials

- Elite Material Co., Ltd.(EMC)

- Grace Electron

- Hanwha Advanced Materials

- Hitachi Chemical Co., Ltd.

- Isola Group

- ITEQ Corporation

- Kingboard Laminates Holdings Ltd.

- Mitsubishi Gas Chemical Company, Inc.

- Nan Ya Plastics Corporation

- Nelco Products(Park Electrochemical Corp.)

- Nippon Mektron, Ltd.

- Panasonic Corporation

- Rogers Corporation

- Shengyi Technology Co., Ltd.

- Shinko Electric Industries Co., Ltd.

- Sumitomo Bakelite Co., Ltd.

- SYTECH

- Taiwan Union Technology Corporation(TUC)

- TUC(Taiwan Union Technology Corporation)

- Ventec International Group

- Wazam New Materials

- Zhongying Science &Technology

The Global High Frequency High Speed Copper Clad Laminate Market reached USD 3.7 billion in 2024 and is expected to grow at a robust CAGR of 10.3% from 2025 to 2034. This growth is largely fueled by the rapid adoption of 5G technology and the surging demand for advanced electronic devices across various industries. With the increasing need for high-speed data transmission and enhanced connectivity, manufacturers are relying more on high-performance materials such as high-frequency and high-speed CCLs. These laminates play a crucial role in the production of printed circuit boards, which power modern electronic equipment, telecommunications infrastructure, and high-speed computing systems.

The growing integration of artificial intelligence, the Internet of Things (IoT), and autonomous vehicles is further amplifying the demand for efficient and high-speed electronic components. As data processing needs evolve, industries are focusing on next-generation technologies that require robust and reliable circuit materials. Additionally, the shift toward compact, lightweight, and energy-efficient devices is creating opportunities for manufacturers to innovate in material composition, improving the thermal resistance, signal integrity, and overall performance of copper clad laminates. With significant investments in semiconductor advancements and wireless communication networks, the market for high-frequency and high-speed CCLs is poised for substantial expansion in the years ahead.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.7 Billion |

| Forecast Value | $9.6 billion |

| CAGR | 10.3% |

The market is primarily categorized into high-frequency CCL and high-speed CCL, with the high-frequency segment projected to dominate, reaching USD 2.5 billion in 2024. The increasing reliance on advanced telecommunications infrastructure and the growing need for uninterrupted, high-speed data flow are driving the demand for high-frequency CCLs. Industries such as telecommunications and consumer electronics are witnessing an unprecedented shift toward faster, more reliable electronic components, further accelerating the adoption of these laminates.

In terms of resin types, the high frequency high-speed copper clad laminate (CCL) market is segmented into phenolic resin, epoxy resin, polyimide resin, and Bismaleimide-Triazine (BT) resin. The epoxy resin segment held a 36.3% market share in 2024, driven by its superior performance characteristics and ability to enhance the structural integrity of PCBs. Ongoing advancements in epoxy resin formulations are improving the durability, thermal stability, and electrical performance of copper clad laminates, making them a preferred choice among PCB manufacturers.

The U.S. high frequency high-speed copper clad laminate (CCL) market is forecasted to reach USD 1.1 billion in 2024, propelled by the rapid deployment of 5G infrastructure, increased electronics adoption, and the expansion of the automotive industry. As the demand for smarter, more efficient electronic devices continues to rise, the need for high-performance materials like high-frequency and high-speed CCLs is set to grow across multiple sectors, reinforcing their critical role in the future of digital transformation.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Demand for 5G technology expansion

- 3.6.1.2 Increasing demand for electronic devices

- 3.6.1.3 Surge in consumer electronics demand

- 3.6.1.4 Advancements in aerospace and defense technologies

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High costs of production processes

- 3.6.2.2 Stringent environmental regulations compliance

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Million)

- 5.1 Key trends

- 5.2 High frequency CCL

- 5.3 High speed CCL

Chapter 6 Market Estimates & Forecast, By Resin Type, 2021-2034 (USD Million)

- 6.1 Key trends

- 6.2 Epoxy resin

- 6.3 Phenolic resin

- 6.4 Polyimide resin

- 6.5 Bismaleimide-Triazine (BT) resin

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Million)

- 7.1 Key trends

- 7.2 5G Base stations

- 7.3 Automotive electronics

- 7.4 Consumer electronics

- 7.4.1 Smartphones

- 7.4.2 Tablets

- 7.4.3 Laptops

- 7.5 Telecommunications

- 7.5.1 Routers

- 7.5.2 Switches

- 7.5.3 Antennas

- 7.6 Aerospace and defense

- 7.6.1 Radar systems

- 7.6.2 Communication systems

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 AGC Inc. (Asahi Glass Co., Ltd.)

- 9.2 Arlon Electronic Materials

- 9.3 Doosan Corporation Electro-Materials

- 9.4 Elite Material Co., Ltd. (EMC)

- 9.5 Grace Electron

- 9.6 Hanwha Advanced Materials

- 9.7 Hitachi Chemical Co., Ltd.

- 9.8 Isola Group

- 9.9 ITEQ Corporation

- 9.10 Kingboard Laminates Holdings Ltd.

- 9.11 Mitsubishi Gas Chemical Company, Inc.

- 9.12 Nan Ya Plastics Corporation

- 9.13 Nelco Products (Park Electrochemical Corp.)

- 9.14 Nippon Mektron, Ltd.

- 9.15 Panasonic Corporation

- 9.16 Rogers Corporation

- 9.17 Shengyi Technology Co., Ltd.

- 9.18 Shinko Electric Industries Co., Ltd.

- 9.19 Sumitomo Bakelite Co., Ltd.

- 9.20 SYTECH

- 9.21 Taiwan Union Technology Corporation (TUC)

- 9.22 TUC (Taiwan Union Technology Corporation)

- 9.23 Ventec International Group

- 9.24 Wazam New Materials

- 9.25 Zhongying Science & Technology