|

市場調査レポート

商品コード

1928876

民生用電子機器向け高電圧電気コンデンサ市場における機会、成長要因、業界動向分析、および2026年から2035年までの予測Consumer Electronics High Voltage Electric Capacitor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 民生用電子機器向け高電圧電気コンデンサ市場における機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2026年01月06日

発行: Global Market Insights Inc.

ページ情報: 英文 141 Pages

納期: 2~3営業日

|

概要

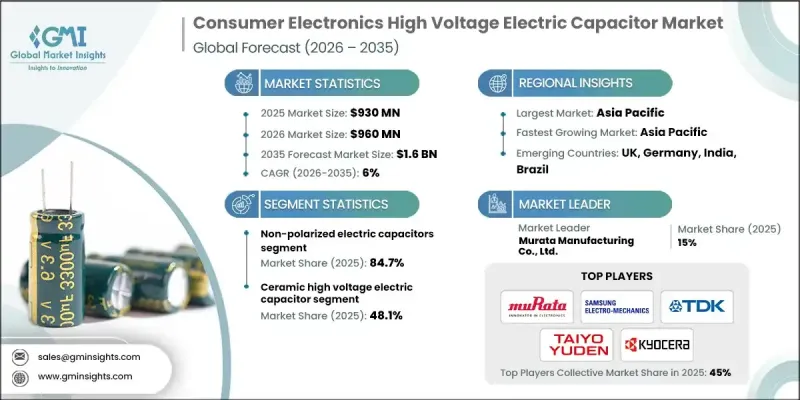

世界の民生用電子機器向け高電圧電気コンデンサ市場は、2025年に9億3,000万米ドルと評価され、2035年までにCAGR 6%で成長し、16億米ドルに達すると予測されています。

この成長は、現代の民生用電子機器における電力需要の増加と、高電圧電源アーキテクチャへの移行加速によって牽引されています。高ワット数USB-C急速充電規格の普及により、コンパクトな形状と熱効率を維持しつつ、電源設計はより高い電圧レベルへと向かっています。先進的なUSB Power Delivery仕様への移行に伴い、28V、36V、48Vの固定電圧レールと最大240Wのプログラマブル電力供給が導入され、パワーステージ部品にはより高い性能が要求されます。デバイスメーカーがUSB-Cを中心にインターフェースを統合する中、安全基準への適合性、世界の相互運用性、一貫した電気的挙動への重視が高まっています。このような環境下では、高い電気的安定性を備えた信頼性の高い標準化された高電圧コンデンサが求められます。小型化の動向に加え、電圧および静電容量密度の増加が需要をさらに強化しています。電力変換ステージは、効率向上と部品サイズの縮小のために、より高いスイッチング周波数とバス電圧で動作します。これにより、コンパクトな設置面積内で高電圧定格、耐熱性、安定した誘電特性を提供するコンデンサが求められています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 9億3,000万米ドル |

| 予測金額 | 16億米ドル |

| CAGR | 6% |

非分極性電気コンデンサセグメントは、2025年に84.7%のシェアを占め、2035年までCAGR5.9%で成長すると予測されています。誘電体材料と多層構造の進歩は、特に民生用電子機器の電源回路において高電圧対応能力、信頼性、コンパクトサイズが求められる場面で、非分極性設計の採用を継続的に支えています。

フィルムコンデンサセグメントは、2035年までCAGR5.9%で成長すると予測されています。高電圧下での長寿命と高効率を兼ね備えた民生用途での需要は引き続き堅調です。これらの部品は、耐久性、電圧安定性、耐熱性が製品性能に極めて重要な場面で、ますます好まれる傾向にあります。

米国消費者向け電子機器向け高電圧電気コンデンサ市場は、2025年に75%のシェアを占め、6億5,000万米ドルの規模に達しました。更新された安全基準への重視の高まりとハイブリッドエネルギーソリューションの普及拡大により、消費者向け電力システムで使用されるコンデンサに対する品質要求は引き続き高まっています。住宅環境におけるハイブリッドインバータやバックアップ対応ソリューションの導入増加は、先進的なパワーエレクトロニクス分野における堅牢なコンデンサの需要を強化しています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーターの分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- PESTEL分析

- 新たな機会と動向

- デジタル化とIoT統合

- 新興市場への進出

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 戦略的取り組み

- 競合ベンチマーキング

- 戦略的ダッシュボード

- イノベーションと技術動向

第5章 市場規模・予測:偏光別、2022-2035

- 偏光型

- 非偏光

第6章 市場規模・予測:材料別、2022-2035

- フィルムコンデンサ

- セラミックコンデンサ

- 電解コンデンサ

- その他

第7章 市場規模・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- フランス

- ドイツ

- イタリア

- オーストリア

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- ラテンアメリカ

- ブラジル

- アルゼンチン

- チリ

第8章 企業プロファイル

- ABB

- CapXon International Electronic Co., Ltd.

- Cornell Dubilier Electronics

- ELNA Co., Ltd.

- Havells India Ltd.

- JBキャパシターズ社

- KEMET Corporation

- KYOCERA AVX Components Corporation

- Murata Manufacturing Co., Ltd.

- Nichicon Corporation

- Panasonic Corporation

- Rubycon Corporation

- Samsung Electro-Mechanics Co., Ltd.

- Schneider Electric

- Siemens

- Taiyo Yuden Co., Ltd.

- TDK Corporation

- Vishay Intertechnology, Inc.

- WIMA GmbH &Co. KG

- Xuansn Electronic