|

市場調査レポート

商品コード

1797828

ニードルコークス市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Needle Coke Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| ニードルコークス市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年07月21日

発行: Global Market Insights Inc.

ページ情報: 英文 141 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

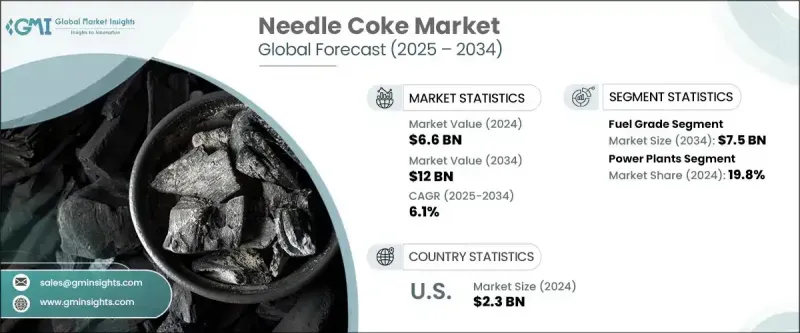

世界のニードルコークス市場は、2024年に66億米ドルと評価され、CAGR 6.1%で成長し、2034年には120億米ドルに達すると推定されています。

この分野の成長は、鉄鋼生産に広く使用されている電気炉用黒鉛電極の製造における重要な役割に強く影響されています。アシキュラー構造と低熱膨張係数で知られるこの高級石油コークスは、卓越した熱伝導性と電気伝導性が不可欠な用途に特に適しています。鉄鋼業界では、従来の高炉法に比べてエネルギー効率が高く、二酸化炭素排出量も削減できることから、電気炉技術の採用が進んでおり、高品質黒鉛電極の需要は拡大し続けています。業界のダイナミクスは、精製技術の進歩、性能向上への注目の高まり、伝統的用途と新興用途の両方における産業要件の進化によっても形成されます。

石油コークスの品位によって、市場は燃料用と脱炭酸用に分けられます。燃料用セグメントは2034年までに75億米ドルを超えると予測され、同期間のCAGRは6%です。この分野の開発は、世界のエネルギー需要の動向、製油所の操業動向、環境規制の強化の影響を受けています。燃焼効率の向上と排出ガスの抑制を目的とした新たな技術革新により、調達の選好の形が変わり始めており、多くの産業が、より厳しい環境基準を遵守しながら燃料コークスの利点を最大化するソリューションを求めています。このため、生産者にとっては、性能とコンプライアンスの両方の目標を達成するために、先進技術を製造プロセスに統合する機会が生まれています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 66億米ドル |

| 予測金額 | 120億米ドル |

| CAGR | 6.1% |

用途別に見ると、ニードルコークス産業は、発電所、セメント製造、鉄鋼生産、アルミニウム加工、その他の産業用途に分けられます。現在、発電所分野が最大のシェアを占めており、2024年には市場の19.8%を占め、2034年までのCAGRは6.1%で拡大すると予測されています。発電におけるニードルコークスの使用は、世界のエネルギーインフラがより効率的で持続可能なソリューションへと移行するにつれて、特に高温および高度なエネルギー貯蔵システムで勢いを増しています。こうした開発は、エネルギー政策の変化、産業システムの近代化、材料性能の技術的進歩と密接に関連しています。

地域別では、北米が依然として突出した市場であり、米国が圧倒的な地位を占めています。2024年には、米国が地域別シェアの約94%を占め、23億米ドルの売上を計上しました。この地域の市場拡大は、産業のアップグレード、持続可能性対策の実施、革新的エネルギー技術の採用によって支えられています。輸入依存度の低減とクリーン・エネルギー・システムの導入促進を目指した政策イニシアチブが、市場の見通しをさらに明るいものにしています。堅調な内需と的を絞った産業政策の組み合わせは、将来の成長に向けた強力な基盤を確立しました。

ニードルコークス市場で事業を展開する企業は、その地位を強化するために複数の戦略を追求しています。持続可能な精製と、電極および電池グレードの両方の用途向けに製品の純度、密度、性能を向上させる高度な加工技術に重点を置いた研究開発に多額の投資が向けられています。川下メーカーとの提携や合弁事業を含む戦略的提携は、長期的に安定した需要を確保し、共同での製品革新を可能にするために行われています。さらに、新たな生産施設や流通網を通じた高成長新興市場への進出は、世界なプレゼンスを多様化し、未開拓の需要ポテンシャルを開拓しようとするサプライヤーにとって、重要な優先事項となりつつあります。

このような技術の進歩、規制の適応、業界の戦略的協力の組み合わせが、競合環境を再構築しています。市場の成長軌道は、鉄鋼セクターからの需要の高まりだけでなく、複数の産業にわたる様々な高性能用途におけるニードルコークスの役割の拡大を反映しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 規制情勢

- 製造技術分析

- 遅延コーキングプロセスの進歩

- 共炭化技術

- 代替原料の開発

- 品質向上技術

- 新たな生産方法論

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 輸出入貿易分析

- 価格動向分析

- グレード別

- 地域別

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- 中東・アフリカ

- ラテンアメリカ

- 戦略ダッシュボード

- 戦略的取り組み

- 競合ベンチマーキング

- イノベーションとテクノロジーの情勢

第5章 市場規模・予測:グレード別、2021年~2034年

- 主要動向

- 燃料グレード

- 焼成ペトコークス

第6章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- 発電所

- セメント産業

- 鉄鋼業界

- アルミニウム産業

- その他

第7章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- スペイン

- 英国

- イタリア

- フランス

- ドイツ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 中東・アフリカ

- チュニジア

- トルコ

- モロッコ

- ラテンアメリカ

- ブラジル

- アルゼンチン

- チリ

- メキシコ

第8章 企業プロファイル

- AMINCO RESOURCES

- Bharat Petroleum Corporation Limited

- BP plc

- Cenovus Inc

- Chevron Corporation

- Cocan graphite

- Exxon Mobil Corporation

- Fangda Carbon New Materials Technology Co., Ltd.

- GrafTech International

- Graphite India Limited

- Indian Oil Corporation

- Marathon Petroleum Corporation

- Mitsubishi Chemical Group Corporation

- Oxbow Corporation

- Reliance Industries Limited

- Rain Carbon Inc.

- Saudi Arabian Oil Company(Saudi Aramco)

- Shamokin Carbons

- Shell Plc

- Valero

The Global Needle Coke Market was valued at USD 6.6 billion in 2024 and is estimated to grow at a CAGR of 6.1% to reach USD 12 billion by 2034. Growth in this sector is strongly influenced by its critical role in manufacturing graphite electrodes for electric arc furnaces, which are widely used in steel production. This premium-grade petroleum coke, known for its acicular structure and low coefficient of thermal expansion, is especially suited for applications where exceptional thermal and electrical conductivity is essential. As the steel industry increasingly adopts electric arc furnace technology due to its energy efficiency and reduced carbon footprint compared to conventional blast furnace methods, the demand for high-quality graphite electrodes continues to expand, thereby driving the market for needle coke. Industry dynamics are also shaped by advances in refining technologies, heightened focus on performance improvements, and evolving industrial requirements in both traditional and emerging applications.

Based on grade, the market is split into fuel-grade and calcinated petroleum coke segments. The fuel-grade category is forecast to exceed USD 7.5 billion by 2034, advancing at a CAGR of 6% over the same period. Developments in this segment are influenced by shifting patterns in global energy demand, operational trends within refineries, and the tightening of environmental regulations. New innovations aimed at improving combustion efficiency and controlling emissions are beginning to reshape procurement preferences, with many industries seeking solutions that maximize the benefits of fuel coke while adhering to stricter environmental standards. This has created opportunities for producers to integrate advanced technologies into manufacturing processes to meet both performance and compliance targets.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.6 Billion |

| Forecast Value | $12 Billion |

| CAGR | 6.1% |

From an application perspective, the needle coke industry is divided into power plants, cement manufacturing, steel production, aluminum processing, and other industrial uses. The power plant sector currently accounts for the largest share, representing 19.8% of the market in 2024, and is projected to expand at a CAGR of 6.1% through 2034. The use of needle coke in power generation is gaining momentum, particularly in high-temperature and advanced energy storage systems, as global energy infrastructures transition toward more efficient and sustainable solutions. These developments are closely linked to changes in energy policy, the modernization of industrial systems, and technological advancements in material performance.

Regionally, North America remains a prominent market, with the United States holding a dominant position. In 2024, the U.S. accounted for around 94% of the regional share, generating USD 2.3 billion in revenue. Market expansion here is supported by industrial upgrades, the implementation of sustainability measures, and adoption of innovative energy technologies. Policy initiatives aimed at reducing import dependency and accelerating the deployment of clean energy systems have further contributed to the positive market outlook. The combination of robust domestic demand and targeted industry policies has established a strong foundation for future growth.

Companies operating in the needle coke market are pursuing multiple strategies to strengthen their position. Significant investments are being directed toward research and development, with a focus on sustainable refining and advanced processing technologies that enhance product purity, density, and performance for both electrode and battery-grade applications. Strategic alliances, including partnerships and joint ventures with downstream manufacturers, are being formed to secure stable long-term demand and enable collaborative product innovation. Additionally, expansion into high-growth emerging markets through new production facilities and distribution networks is becoming a key priority for suppliers seeking to diversify their global presence and tap into untapped demand potential.

This combination of technological progress, regulatory adaptation, and strategic industry collaboration is reshaping the competitive environment. The market's growth trajectory reflects not only the rising demand from the steel sector but also the expanding role of needle coke in various high-performance applications across multiple industries.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

- 2.1.1 Business trends

- 2.1.2 Grade trends

- 2.1.3 Application trends

- 2.1.4 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Manufacturing technology analysis

- 3.3.1 Delayed coking process advancements

- 3.3.2 Co-carbonization technologies

- 3.3.3 Alternative feedstock development

- 3.3.4 Quality enhancement techniques

- 3.3.5 Emerging production methodologies

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Import/export trade analysis

- 3.6 Price trend analysis

- 3.6.1 By grade

- 3.6.2 By geography

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.8.1 Bargaining power of suppliers

- 3.8.2 Bargaining power of buyers

- 3.8.3 Threat of new entrants

- 3.8.4 Threat of substitutes

- 3.9 PESTEL analysis

- 3.9.1 Political factors

- 3.9.2 Economic factors

- 3.9.3 Social factors

- 3.9.4 Technological factors

- 3.9.5 Environmental factors

- 3.9.6 Legal factors

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, 2024

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategy dashboard

- 4.4 Strategic initiative

- 4.5 Competitive benchmarking

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Grade, 2021 - 2034, (MT and USD Billion)

- 5.1 Key trends

- 5.2 Fuel grade

- 5.3 Calcinated petcoke

Chapter 6 Market Size and Forecast, By Application, 2021 - 2034, (MT and USD Billion)

- 6.1 Key trends

- 6.2 Power plants

- 6.3 Cement industry

- 6.4 Steel industry

- 6.5 Aluminum industry

- 6.6 Others

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034, (MT and USD Billion)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Spain

- 7.3.2 UK

- 7.3.3 Italy

- 7.3.4 France

- 7.3.5 Germany

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.5 Middle East & Africa

- 7.5.1 Tunisia

- 7.5.2 Turkey

- 7.5.3 Morocco

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

- 7.6.3 Chile

- 7.6.4 Mexico

Chapter 8 Company Profiles

- 8.1 AMINCO RESOURCES

- 8.2 Bharat Petroleum Corporation Limited

- 8.3 BP plc

- 8.4 Cenovus Inc

- 8.5 Chevron Corporation

- 8.6 Cocan graphite

- 8.7 Exxon Mobil Corporation

- 8.8 Fangda Carbon New Materials Technology Co., Ltd.

- 8.9 GrafTech International

- 8.10 Graphite India Limited

- 8.11 Indian Oil Corporation

- 8.12 Marathon Petroleum Corporation

- 8.13 Mitsubishi Chemical Group Corporation

- 8.14 Oxbow Corporation

- 8.15 Reliance Industries Limited

- 8.16 Rain Carbon Inc.

- 8.17 Saudi Arabian Oil Company (Saudi Aramco)

- 8.18 Shamokin Carbons

- 8.19 Shell Plc

- 8.20 Valero