|

市場調査レポート

商品コード

1892833

小型トラック用ステアリングシステム市場における機会、成長要因、業界動向分析、および2026年から2035年までの予測Light Duty Truck Steering System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 小型トラック用ステアリングシステム市場における機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2025年12月09日

発行: Global Market Insights Inc.

ページ情報: 英文 235 Pages

納期: 2~3営業日

|

概要

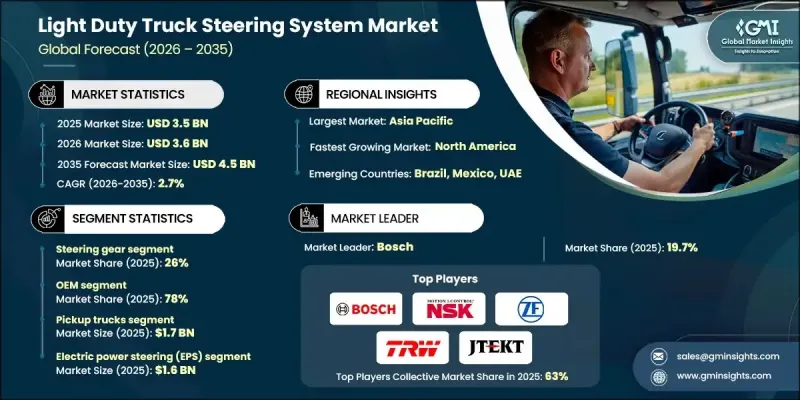

世界の小型トラック用ステアリングシステム市場は、2025年に35億米ドルと評価され、2035年までにCAGR2.7%で成長し、45億米ドルに達すると予測されています。

市場拡大の背景には、先進的で安全かつ効率的なステアリング技術への需要増加に加え、電気式およびハイブリッド式小型トラックの普及拡大、ならびに商業・物流業務の成長が挙げられます。フリート事業者や個人購入者は、運転者の快適性、車両の操作性、安全性を重視しており、多様な道路状況や運用環境において信頼性の高いハンドリングを実現する現代的なステアリングシステムが不可欠となっています。電動パワーステアリング(EPS)、油圧補助システム、適応型ステアリングモジュール、軽量高強度部品などの革新技術が、これらのトラックの機能性を変革しています。アルミニウム合金、高張力鋼、耐食性コーティングなどの高品質素材により、耐久性に優れた長寿命のステアリングソリューションが実現されています。拡大する都市物流、ラストマイル配送サービス、ライドシェアリング車両、そして操縦性と安全性が向上したトラックへの需要が、世界の市場導入を加速させています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 35億米ドル |

| 予測金額 | 45億米ドル |

| CAGR | 2.7% |

ステアリングギアセグメントは2025年に26%のシェアを占め、2026年から2035年にかけてCAGR2.2%で成長すると予測されています。ステアリングギアは、ピックアップトラック、バン、小型商用トラックにおいて、車両の精密な制御、安定性、操作性を確保する上で極めて重要です。頑丈な構造、油圧式、電動式、電気油圧式アーキテクチャとの互換性、重負荷や変動負荷条件下での信頼性を備えており、OEMメーカーやフリート事業者から選ばれる選択肢となっております。

OEMセグメントは2025年に78%のシェアを占め、2035年までCAGR2.3%で成長すると予測されています。OEMチャネルでは、ステアリングシステムを新型トラックに統合し、安全基準と性能基準を満たす認定済み高品質部品の使用を保証します。これらのシステムは、シームレスな車両互換性、運転者快適性の向上、耐久性、精度を提供します。OEM搭載は、その信頼性とEPS(電動パワーステアリング)、ADAS(先進運転支援システム)、車両テレマティクスなどの先進技術との整合性から高く評価されています。

中国の小型トラック用ステアリングシステム市場は2025年に4億4,350万米ドルの売上高を記録し、33%のシェアを占めました。成長の要因としては、ピックアップトラックや小型商用車の生産拡大、先進自動車技術への投資、EPS(電動パワーステアリング)、ステアバイワイヤ、ADAS統合型ステアリングソリューションの採用が挙げられます。さらに、政府による新エネルギー車支援策や安全規制の強化が、現代的なステアリングシステムの利用を後押ししています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 先進ステアリング技術に対する需要の高まり

- 小型トラックフリートの成長

- ドライバーの快適性と安全性への注力

- 技術統合と材料革新

- 業界の潜在的リスク&課題

- 高コストシステム

- 複雑な保守要件

- 市場機会

- 電気式およびハイブリッド式小型トラックの拡大

- アフターマーケットおよび改修ソリューション

- ADASおよび自動運転車両の統合

- 軽量かつ省エネルギーなシステム

- 促進要因

- 成長可能性分析

- 規制情勢

- ポーター分析

- PESTEL分析

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- 生産統計

- 生産拠点

- 消費拠点

- 輸出入

- コスト内訳分析

- 特許分析

- 持続可能性と環境面

- 持続可能な実践

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に配慮した取り組み

- 投資・資金調達分析

- OEMの研究開発投資動向

- サプライヤー設備投資配分

- 技術系スタートアップの資金調達動向

- 最良のシナリオ

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 事業拡大計画と資金調達

第5章 市場推計・予測:コンポーネント別、2022-2035

- 主要動向

- ステアリングギア

- ステアリングコラム

- センサーおよびコントローラー

- ステアリングポンプ

- タイロッド

- ステアリングホイール

- その他

第6章 市場推計・予測:車両別、2022-2035

- 主要動向

- ピックアップトラック

- SUVおよびクロスオーバー車

- 小型商用車(LCV)

- バン

第7章 市場推計・予測:技術別、2022-2035

- 主要動向

- 電動パワーステアリング(EPS)

- 油圧式パワーステアリング(HPS)

- 電気油圧式パワーステアリング(EHPS)

- ステアバイワイヤ

第8章 市場推計・予測:販売チャネル別、2022-2035

- 主要動向

- OEM

- アフターマーケット

第9章 市場推計・予測:地域別、2022-2035

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ベルギー

- オランダ

- スウェーデン

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- シンガポール

- 韓国

- ベトナム

- インドネシア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ地域

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- Global Player

- Bosch

- Denso

- Hyundai Mobis

- JTEKT

- Magna International

- Nexteer Automotive

- NSK

- Thyssenkrupp

- TRW Automotive

- ZF Friedrichshafen

- Regional Player

- Aisin Seiki

- Calsonic Kansei

- Hitachi Astemo

- JMC Steering

- Kongsberg Automotive

- Mando

- Mevotech

- Mubea

- Schaeffler

- KYB

- 新興メーカー

- Auto Steering Technologies

- Eberspacher Steering Solutions

- Neapco

- Protean Electric

- Servotronic Systems