|

市場調査レポート

商品コード

1750576

住宅用暖房機器の市場機会、成長促進要因、産業動向分析、予測、2025年~2034年Residential Heating Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 住宅用暖房機器の市場機会、成長促進要因、産業動向分析、予測、2025年~2034年 |

|

出版日: 2025年05月15日

発行: Global Market Insights Inc.

ページ情報: 英文 160 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

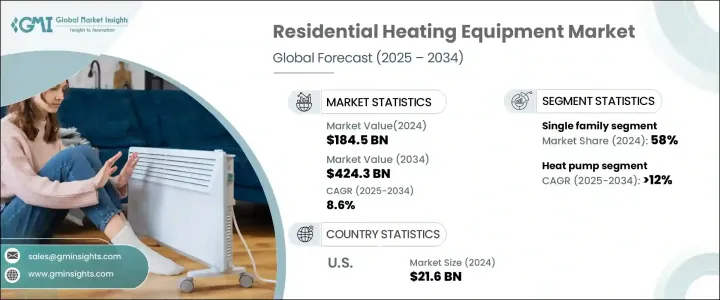

世界の住宅用暖房機器市場は、2024年には1,845億米ドルとなり、CAGR 8.6%で成長し、2034年には4,243億米ドルに達すると推定されています。

これは、エネルギー効率と環境持続可能性に対する意識の高まりが、消費者に先進的で環境に優しい暖房システムの採用を促しているためです。世界各国政府はカーボンニュートラル目標を設定し、住宅所有者にエネルギー効率の高いソリューションへの投資を奨励する政策を実施しており、スマートで持続可能な家庭用暖房への移行を促進しています。都市部の住宅開発とエネルギー消費削減への継続的な関心は、効率的な暖房技術の採用に拍車をかけています。さらに、先進的な電気ヒートポンプのハイブリッドシステムへの統合は、住宅部門における持続可能な排出削減を支援します。

米国全土で極端な寒波の頻度と強度が高まっているため、信頼できる住宅用暖房システムは単なる嗜好品ではなく必需品となっています。これに対応するため、より多くの住宅所有者が、外的条件に関係なく室内温度を一定に保つ高度な暖房技術に注目しています。同時に、IoT対応システムやスマートサーモスタットなどのインテリジェント制御の統合により、ユーザーはエネルギー使用量をより正確に管理できるようになっています。これらの技術革新は、家庭が不必要な暖房を削減するのに役立ち、毎月の光熱費を削減するだけでなく、より広範な持続可能性の目標にも合致します。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 1,845億米ドル |

| 予測金額 | 4,243億米ドル |

| CAGR | 8.6% |

ヒートポンプの住宅用暖房機器市場は、2034年までCAGR 12%で成長すると予測されます。エネルギー効率に優れたソリューションに対するニーズの高まりと政府の好意的な政策が相まって、住宅用ヒートポンプの採用が促進されます。継続的な技術開発により、運転効率が向上し、環境に優しい慣行が促進されます。市場は一戸建て用と集合住宅用に区分されます。

一戸建て用住宅用暖房機器分野は、2034年までCAGR 8%で事業成長を牽引し、2024年には58%のシェアを占めると予測されます。多様な暖房ニーズに対応するカスタマイズソリューションに対する需要の高まりが、製品採用を増加させる。さらに、遠隔監視システム、予知保全、プロセス最適化の統合が業界の展望を推進します。

米国の住宅用暖房機器の2024年の市場規模は216億米ドルで、環境規制、消費者意識の高まり、エネルギー効率の高いアップグレードを奨励する政府の支援プログラムなどが後押ししています。同市場はまた、旧式の暖房システムを新しい炭素排出基準に適合した高性能の代替品に交換する、広範な改修活動からも恩恵を受けています。さらに、住宅スペースの電化へのシフトは、ヒートポンプやハイブリッドシステムの新たな機会を生み出しています。

同市場の主要企業には、Whirlpool, Vaillant Group, Bradford White Corporation, Ferroli, Crane, SAMSUNG, Panasonic Corporation, A.O. Smith, Carrier Corporation, DAIKIN INDUSTRIES, Lennox International, Robert Bosch, Hoval, Trane Technologies, Rinnai America, Rheem Manufacturing Company, GE Appliances, LG Electronics, Ariston Holding, Havells India, BDR Thermea Group, Arovast Corporation, Johnson Control International, VIESSMANNなどが含まれます。市場での存在感を高めるため、住宅用暖房機器業界の企業は様々な戦略を採用しています。革新的な製品の発売、流通網の拡大、戦略的提携や買収などです。例えば、エネルギー効率の高いソリューションに対する需要の高まりに対応するため、企業は再生可能エネルギー源とスマート技術を統合した高度な暖房システムを開発しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 戦略的ダッシュボード

- 戦略的取り組み

- 競合ベンチマーキング

- イノベーションとテクノロジーの情勢

第5章 市場規模・予測:技術別、2021年~2034年

- 主要動向

- ヒートポンプ

- ボイラー

- 炉

- 給湯器

- その他

第6章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- 一戸建て

- 集合住宅

第7章 市場規模・予測:販売チャネル別、2021年~2034年

- 主要動向

- オンライン

- ディーラー

- 小売

第8章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- フランス

- 英国

- イタリア

- スペイン

- ポルトガル

- ルーマニア

- オランダ

- スイス

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- エジプト

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

第9章 企業プロファイル

- A.O. Smith

- Ariston Holding

- Arovast Corporation

- BDR Thermea Group

- Bradford White Corporation

- Carrier Corporation

- Crane

- DAIKIN INDUSTRIES

- Ferroli

- GE Appliances

- Havells India

- Hoval

- Johnson Control International

- Lennox International

- LG Electronics

- Panasonic Corporation

- Rheem Manufacturing Company

- Rinnai America

- Robert Bosch

- SAMSUNG

- Trane Technologies

- Vaillant Group

- VIESSMANN

- Whirlpool

The Global Residential Heating Equipment Market was valued at USD 184.5 billion in 2024 and is estimated to grow at a CAGR of 8.6% to reach USD 424.3 billion by 2034, driven by increasing awareness of energy efficiency and environmental sustainability, prompting consumers to adopt advanced and eco-friendly heating systems. Governments worldwide are setting carbon neutrality targets and implementing policies encouraging homeowners to invest in energy-efficient solutions, facilitating the transition toward smart and sustainable home heating. Urban housing development and the ongoing focus on reducing energy consumption fuel the adoption of efficient heating technologies. Additionally, the integration of advanced electric heat pumps into hybrid systems supports sustainable emission reduction within the residential sector.

The growing frequency and intensity of extreme cold spells across the U.S. have made dependable residential heating systems not just a preference but a necessity. In response, more homeowners are turning to advanced heating technologies that ensure consistent indoor temperatures regardless of external conditions. At the same time, the integration of intelligent controls, such as IoT-enabled systems and smart thermostats, is enabling users to manage energy usage with greater precision. These innovations help households cut down on unnecessary heating, which not only reduces monthly utility bills but also aligns with broader sustainability goals.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $184.5 Billion |

| Forecast Value | $424.3 Billion |

| CAGR | 8.6% |

The heat pump residential heating equipment market is expected to grow at a CAGR of 12% through 2034. The increasing need for energy-efficient solutions, coupled with favorable government policies, will boost the adoption of residential heat pumps. Ongoing technological developments will enhance their operational efficiency and promote environmentally friendly practices. The market is segmented into single-family and multi-family applications.

The single-family residential heating equipment segment is anticipated to drive business growth at a CAGR of 8% through 2034, holding a share of 58% in 2024. The growing demand for customized solutions to meet diverse heating needs will increase product adoption. Additionally, integrating remote monitoring systems, predictive maintenance, and process optimization will propel the industry outlook.

U.S. Residential Heating Equipment Market was valued at USD 21.6 billion in 2024, fueled by environmental mandates, rising consumer awareness, and government-backed programs that incentivize energy-efficient upgrades. The market is also benefiting from widespread retrofitting activities, where older heating systems are being replaced with high-performance alternatives that comply with newer carbon emission standards. Additionally, the shift toward electrification in residential spaces creates new opportunities for heat pumps and hybrid systems.

Key players in the market include Whirlpool, Vaillant Group, Bradford White Corporation, Ferroli, Crane, SAMSUNG, Panasonic Corporation, A.O. Smith, Carrier Corporation, DAIKIN INDUSTRIES, Lennox International, Robert Bosch, Hoval, Trane Technologies, Rinnai America, Rheem Manufacturing Company, GE Appliances, LG Electronics, Ariston Holding, Havells India, BDR Thermea Group, Arovast Corporation, Johnson Control International, VIESSMANN. To strengthen their market presence, companies in the residential heating equipment industry are adopting various strategies. These include launching innovative products, expanding distribution networks, and forming strategic partnerships and acquisitions. For instance, companies are developing advanced heating systems that integrate renewable energy sources and smart technologies to meet the growing demand for energy-efficient solutions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, 2024

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.5 Competitive benchmarking

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Technology, 2021 - 2034 (USD Million & ‘000 Units)

- 5.1 Key trends

- 5.2 Heat pump

- 5.3 Boiler

- 5.4 Furnace

- 5.5 Water heater

- 5.6 Others

Chapter 6 Market Size and Forecast, By Application, 2021 - 2034 (USD Million & ‘000 Units)

- 6.1 Key trends

- 6.2 Single-family

- 6.3 Multi-family

Chapter 7 Market Size and Forecast, By Sales Channel, 2021 - 2034 (USD Million & ‘000 Units)

- 7.1 Key trends

- 7.2 Online

- 7.3 Dealer

- 7.4 Retail

Chapter 8 Market Size and Forecast, By Region, 2021 - 2034 (USD Million & ‘000 Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 France

- 8.3.3 UK

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Portugal

- 8.3.7 Romania

- 8.3.8 Netherlands

- 8.3.9 Switzerland

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 Egypt

- 8.5.4 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

Chapter 9 Company Profiles

- 9.1 A.O. Smith

- 9.2 Ariston Holding

- 9.3 Arovast Corporation

- 9.4 BDR Thermea Group

- 9.5 Bradford White Corporation

- 9.6 Carrier Corporation

- 9.7 Crane

- 9.8 DAIKIN INDUSTRIES

- 9.9 Ferroli

- 9.10 GE Appliances

- 9.11 Havells India

- 9.12 Hoval

- 9.13 Johnson Control International

- 9.14 Lennox International

- 9.15 LG Electronics

- 9.16 Panasonic Corporation

- 9.17 Rheem Manufacturing Company

- 9.18 Rinnai America

- 9.19 Robert Bosch

- 9.20 SAMSUNG

- 9.21 Trane Technologies

- 9.22 Vaillant Group

- 9.23 VIESSMANN

- 9.24 Whirlpool