|

市場調査レポート

商品コード

1892886

電磁鋼板市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測Electrical Steel Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 電磁鋼板市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2025年12月15日

発行: Global Market Insights Inc.

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

概要

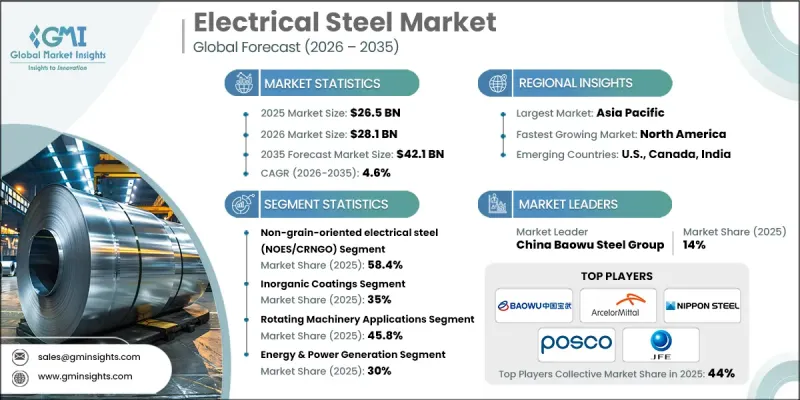

世界の電磁鋼板市場は、2025年に265億米ドルと評価され、2035年までにCAGR4.6%で成長し、421億米ドルに達すると予測されています。

電磁鋼板は、モーター、変圧器、発電機の効率向上に重要な役割を果たし、世界中の電化および産業システムの基幹部品として機能しております。構造用鋼材を供給するだけでなく、自動車、電力インフラ、産業オートメーションなどの分野において重要な下流価値を創出し、現代経済における戦略的素材としての地位を確立しております。電気自動車の急速な普及、送電網近代化プロジェクト、産業オートメーションの進展により、市場はさらなる成長が見込まれております。高性能グレードは、原材料コストの変動にもかかわらず、性能要求により強気の価格維持が見込まれます。アジアは製造業の中心地とインフラ拡張に支えられ主要な需要拠点であり続ける一方、欧州と北米は電化推進策と省エネルギー規制を通じて成長を牽引します。市場は薄肉製品や高度グレード製品が競争上の重要性を増すとともに、ニッチな電磁部品への注目が高まる中、性能主導のエコシステムへと進化しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 265億米ドル |

| 予測金額 | 421億米ドル |

| CAGR | 4.6% |

非方向性電磁鋼板(NOES/CRNGO)セグメントは、2025年に58.4%のシェアを占め、2035年までCAGR 4.9%で成長すると予測されています。NOESは、あらゆる方向で均一な磁気性能を発揮するため、モーターや発電機などの回転機械に最適であり、エネルギー効率と動作速度が重要な電気自動車や産業オートメーションにおいて不可欠です。

無機コーティングセグメントは2025年に35%のシェアを占め、2026年から2035年にかけてCAGR 4.6%で成長すると予測されています。無機コーティングは変圧器コアや重電設備など高温絶縁用途に極めて適しており、過酷な条件下での層間損失を低減し、送電の信頼性を確保します。

北米電気鋼板市場は2025年に12.4%のシェアを占め、先進的な製造能力、強固な規制枠組み、電化インフラへの大規模投資により、戦略的拠点として急速に台頭しています。同地域では、厳格化する技術的・環境的要件を満たすため、省エネルギー性と高性能を兼ね備えたグレードが重視されています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 効率性規制により高品位原料の採用が促進されます

- 電気自動車の普及が超薄型NOESの需要を促進しております

- 送電網の近代化により、政府機関向けエネルギーシステム(GOES)の需要が拡大しております

- 業界の潜在的リスク&課題

- 原材料価格の変動性

- 薄肉/高強度(HiB)製品の生産能力制約

- 市場機会

- 自己接着性コーティングは、組み立て工程を効率化し、歩留まりを向上させます

- データセンター向けUPS・変圧器のアップグレードにより、高品質GOESの需要が高まっています

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- 製品タイプ別

- 将来の市場動向

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 特許状況

- 貿易統計(HSコード)(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境面

- 持続可能な取り組み

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に配慮した取り組み

- カーボンフットプリントへの配慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ地域

- 地域別

- 企業マトリクス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 事業拡大計画

第5章 市場推計・予測:製品タイプ別、2022-2035

- 非方向性電磁鋼板(NOES/CRNGO)

- 方向性電磁鋼板(GOES/CRGO)

- 先進軟磁性材料

- アモルファス電磁鋼板

- ナノ結晶電磁鋼板

- 多層・複合電磁鋼板

第6章 市場推計・予測:コーティングタイプ別、2022-2035

- 無機コーティング

- C-2/EC-2(ミルガラス- ケイ酸マグネシウム)

- C-4/EC-4(リン酸塩処理または化学処理)

- C-5/EC-5(無機質/セラミック充填)

- 有機コーティング

- C-3/EC-3(有機ワニス/エナメル)

- C-6/EC-6(有機系塗料に無機系充填剤を配合)

- 天然酸化被膜

- 自己接着性コーティング

第7章 市場推計・予測:用途別、2022-2035

- 回転機械用途

- 変圧器用途

- 電力用変圧器

- 配電用変圧器

- 特殊変圧器

- 再生可能エネルギー用変圧器

- 電磁部品

- インダクタ及びリアクトル

- 安定器・照明

- ワイヤレス電力伝送

第8章 市場推計・予測:最終用途別、2022-2035

- エネルギー・発電

- 電力会社

- 再生可能エネルギー

- 従来型発電

- エネルギー貯蔵システム

- 自動車・輸送機器

- 電気自動車(バッテリー式電気自動車-BEV)

- ハイブリッド電気自動車(HEV/PHEV)

- 自動車補助システム

- EV充電インフラ

- 鉄道・公共交通機関

- 航空宇宙

- 産業製造

- 産業用機械・設備

- ロボット工学・自動化

- 石油・ガス設備

- 民生用家電・電子機器

- 家庭用電化製品

- 電動工具

- 民生用電子機器

- データセンター及びITインフラストラクチャ

- UPSシステム

- データセンター用変圧器

- サーバー冷却システム

- 空調・ビルシステム

- 業務用空調システム

- 住宅用空調設備

- エレベーター・エスカレーター

第9章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ地域

第10章 企業プロファイル

- Nippon Steel Corporation

- JFE Steel Corporation

- ArcelorMittal S.A.

- POSCO(Pohang Iron &Steel Co.)

- China Baowu Steel Group

- thyssenkrupp Electrical Steel GmbH

- Cleveland-Cliffs Inc.(AK Steel)

- Tata Steel Limited

- Aperam S.A.

- Waelzholz Group

- Ansteel Group Corporation

- HBIS Group(Hebei Iron &Steel)

- Nucor Corporation

- Metglas Inc.(Hitachi Metals Group)

- Advanced Technology &Materials Co. Ltd.(AT&M)