|

市場調査レポート

商品コード

1892830

商業用海藻市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測Commercial Seaweed Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 商業用海藻市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2025年12月15日

発行: Global Market Insights Inc.

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

概要

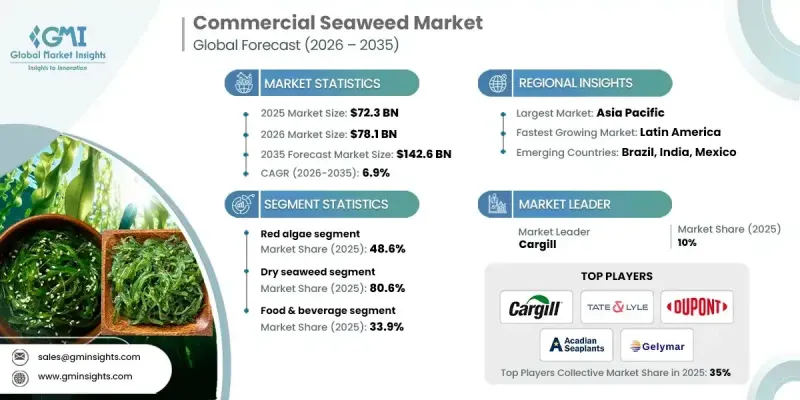

世界の商業用海藻市場は、2025年に723億米ドルと評価され、2035年までにCAGR6.9%で成長し、1,426億米ドルに達すると予測されています。

海藻の機能的多様性と持続可能性が評価され、様々なバリューチェーンへの統合が進むにつれ、市場は勢いを増し続けております。需要拡大の背景には、食品・化粧品・工業用配合剤において重要な結合・安定化・増粘機能を果たす海藻由来水溶性多糖類の利用増加が強く関連しています。これらの用途は世界の商業用海藻収益の40%以上を占めています。同時に、環境に配慮した農業への移行が海藻由来原料の導入を加速させ、海藻を再生型・低環境負荷農業モデルに適合する自然由来の解決策として位置づけています。持続可能な農業との世界の政策連携が需要をさらに強化しています。並行して、海藻バイオテクノロジー分野におけるイノベーションが市場の価値可能性を拡大しており、生産者は栄養・健康・特殊用途向けの高付加価値化合物を抽出するための高度な加工技術へ投資を進めています。こうした進展により、商業用海藻産業は量主導型セクターから、技術によって支えられた高付加価値エコシステムへと変貌を遂げており、多様な最終用途と確固たる長期成長の見通しが特徴となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 723億米ドル |

| 予測金額 | 1,426億米ドル |

| CAGR | 6.9% |

紅藻セグメントは2025年に48.6%のシェアを占め、2035年までCAGR 6.8%で成長すると予測されています。この優位性は、食品、医薬品、パーソナルケア製造における基礎的な原料として、ハイドロコロイド生産に広く利用されていることに支えられており、安定した世界の需要を強化しています。

飲食品用途セグメントは2025年に33.9%のシェアを占め、2026年から2035年にかけてCAGR 6.8%で成長すると予測されています。海藻は天然の機能性原料として広く採用され続けており、包装食品や加工食品カテゴリー全体において、製剤の安定性、栄養強化、クリーンラベルのポジショニングを支えています。

北米の商業用海藻市場は2025年に11%のシェアを占め、急速な成長を見せております。同地域では、持続可能な養殖業、気候変動に対応した素材、代替飼料ソリューションへの投資が増加しており、これが商業利用の拡大と下流分野におけるイノベーションを促進しております。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- タイプ別

- 将来の市場動向

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 特許状況

- 貿易統計(HSコード)(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境面

- 持続可能な取り組み

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に配慮した取り組み

- カーボンフットプリントへの配慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ地域

- 地域別

- 企業マトリクス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 事業拡大計画

第5章 市場推計・予測:タイプ別、2022-2035

- 主要動向

- 紅藻類

- 褐藻類

- 緑藻類

第6章 市場推計・予測:形態別、2022-2035

- 主要動向

- 乾燥海藻

- 生/新鮮な海藻

第7章 市場推計・予測:最終用途別、2022-2035

- 主要動向

- 飲食品

- 乳製品

- 製パン・菓子類

- 加工肉・水産加工品

- ビーガン/植物由来食品

- 機能性飲料

- 食用海藻スナック

- ソース・スープ・調味料

- 動物飼料

- 家畜飼料添加物

- 家禽飼料

- 水産養殖用飼料

- ペットフードサプリメント

- 反芻動物用メタン低減飼料

- 医薬品・パーソナルケア

- 創傷治癒軟膏

- 薬物送達システム

- スキンケアローション・クリーム

- シャンプー・コンディショナー

- 抗加齢・抗炎症製品

- 口腔ケア製品

- バイオ燃料

- バイオエタノール生産

- バイオガス生成

- 藻類バイオマス前処理用投入物

- ハイブリッド再生可能エネルギー混合燃料

- その他

- 農業用バイオ刺激剤

- 土壌改良剤

- 水処理剤

- 繊維産業への応用

- バイオプラスチック及び包装材料

第8章 市場推計・予測:地域別、2022-2035

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ地域

第9章 企業プロファイル

- Acadian Seaplants

- Algaia

- Cargill

- DuPont

- FMC Corporation

- Gelymar

- Indo Alginate

- Irish Seaweeds

- KIMICA Corporation

- Mara Seaweed

- MCPI(Marine Chemicals &Polymers Industries)

- Ocean Harvest Technology

- Qingdao Gather Great Ocean Algae Industry Group

- Qingdao Seawin Biotech Group

- Seasol

- Seaweed Energy Solutions

- Shaanxi Hongda Phytochemistry Co., Ltd.

- Tate &Lyle

- TBK Manufacturing Corporation(Philippines)

- W Hydrocolloids, Inc.

- Others