|

市場調査レポート

商品コード

1913305

ナフタレン市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測Naphthalene Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| ナフタレン市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2026年01月02日

発行: Global Market Insights Inc.

ページ情報: 英文 210 Pages

納期: 2~3営業日

|

概要

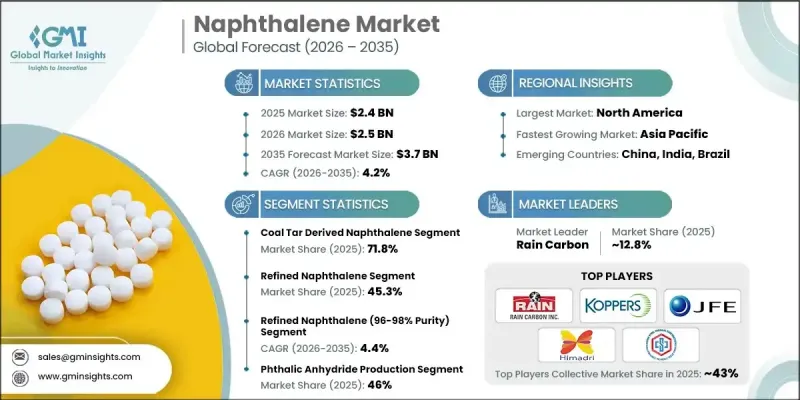

世界のナフタレン市場は、2025年に24億米ドルと評価され、2035年までにCAGR 4.2%で成長し、37億米ドルに達すると予測されています。

ナフタレン(化学式:C10H8)は、主にコールタール処理および石油精製を通じて生産される多環芳香族炭化水素です。本物質は、精製ナフタレン、アルキルナフタレン、固体変種など複数の商業形態で供給され、純度は90~95%の粗品グレードから99%を超える高純度グレードまで多岐にわたります。化学製造チェーンにおける中核原料、建設関連配合剤、確立された産業用途として広く利用されています。無水フタル酸の需要増加、建設用化学品の使用拡大、特殊化学品用途の開発が相まって、世界の市場拡大を牽引しています。生産者は、進化する顧客仕様に対応するため、クリーンな製造プロセス、精密精製システム、差別化された製品グレードに注力しています。加工効率と一貫性の向上は、複数の最終用途産業および地域における安定した需要を支えています。需要の成長、技術の進歩、多様な用途の組み合わせが相まって、ナフタレン市場の長期的な発展を継続的に支えています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 24億米ドル |

| 予測金額 | 37億米ドル |

| CAGR | 4.2% |

精製およびグレード管理における技術進歩により、高純度ナフタレンの製造が再構築されています。石炭タールおよび石油由来の両原料において、99%を超える高純度レベルの高性能用途への対応、結晶化管理の厳密化、バッチ間の一貫性向上が可能となりました。これらの進歩は、高付加価値化学合成および中間体生産に必要な厳格な品質基準を満たすことを目的としています。蒸留技術の高度化、結晶化プロセスの改良、水素化ベースのプロセスにより、不純物含有量が低減されると同時に機能的な信頼性が向上し、メーカーはより予測可能な性能と幅広い産業での受容性を備えたナフタレン製品を提供できるようになっております。

コールタール由来ナフタレンセグメントは2025年に71.8%のシェアを占め、2026年から2035年にかけてCAGR 4%で拡大すると予測されています。その優位性は、鉄鋼・コークス処理工程と連携した成熟した生産システム、有利な収率経済性、安定した製品品質に起因しています。この原料源は、大規模生産を支えつつコスト効率と安定供給を維持する、広範な世界のコールタールインフラの恩恵を受けています。主要消費地域における強固な基盤と、産業バリューチェーンへの長年にわたる統合が相まって、世界のナフタレン市場における主導的地位を継続的に強化しています。

精製ナフタレンセグメントは2025年に45.3%のシェアを占め、2035年までCAGR3.6%で推移すると予測されています。この形態は、安定した純度と優れた取り扱い特性から、大量化学処理における優先選択肢であり続けています。統合化学製造施設内での広範な利用は、効率的な下流工程と信頼性の高い操業性能を支えています。確立された生産ネットワークと実証済みの経済的優位性が、世界の化学生産拠点における継続的な優位性に寄与しています。

米国ナフタレン市場は2025年に9億2,990万米ドルの規模を記録し、産業・建設関連分野における安定した消費に支えられた堅調な地域需要を反映しています。確立された生産施設、統合された加工インフラ、持続的な最終用途需要の存在が、国内市場の安定性を支えています。加工効率とサプライチェーンの信頼性に対する継続的な投資が、北米全域における需要成長の基盤となり続けています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品グレード別

- 将来の市場動向

- 特許状況

- 貿易統計(HSコード)(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境面

- 持続可能な取り組み

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に配慮した取り組み

- カーボンフットプリントへの配慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ地域

- 地域別

- 企業マトリクス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 拡大計画

第5章 市場推計・予測:形態別、2022-2035

- 精製ナフタレン

- アルキルナフタレン

- ナフタレン固体

- その他

第6章 市場推計・予測:ソース別、2022-2035

- コールタール由来ナフタレン

- 石油由来ナフタレン

- 再生原料および二次原料

第7章 市場推計・予測:製品グレード別、2022-2035

- 粗製ナフタレン(純度90-95%)

- 精製ナフタレン(純度96-98%)

- 純ナフタレン(99%以上の純度)

- 特殊グレードおよびカスタム製品

第8章 市場推計・予測:用途別、2022-2035

- 無水フタル酸の製造

- 界面活性剤・分散剤

- 減水剤(建設用化学品)

- 染料・顔料(化学中間体)

- 従来用途(防虫剤、なめし剤)

- 新興およびその他の用途

第9章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ地域

第10章 企業プロファイル

- Atom Scientific

- CDH Fine Chemical

- China Steel Chemical

- Deza

- Dong-Suh Chemical Ind. Co., Ltd.

- ExxonMobil Chemical

- Himadri Specialty Chemical Ltd.

- JFE Chemical Corporation

- King Industries

- Koppers

- PCC Group

- Rain Carbon

- Tulstar Products