|

市場調査レポート

商品コード

1750554

セメント廃熱回収システムの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Cement Waste Heat Recovery System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| セメント廃熱回収システムの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月16日

発行: Global Market Insights Inc.

ページ情報: 英文 138 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

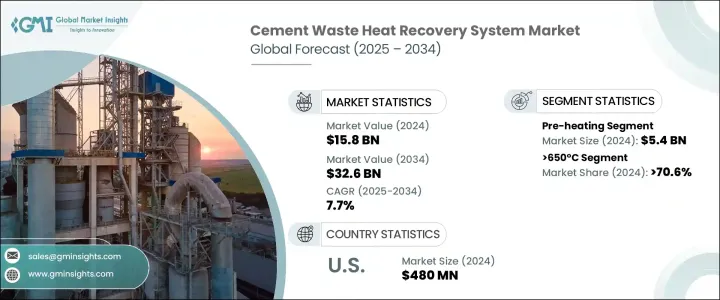

世界のセメント廃熱回収システム市場は、2024年に158億米ドルと評価され、CAGR7.7%で成長し、2034年には326億米ドルに達すると推定されています。

セメント製造工程は、最もエネルギー集約的な産業作業の一つであり、製造中に大量の熱が発生し、しばしば失われます。廃熱回収システムは、この未使用の熱エネルギーを回収し、発電やプロセス加熱に振り向け、大幅なコスト削減と外部エネルギー源への依存度低減を実現する不可欠なソリューションとして台頭してきています。セメントメーカーは、エネルギー消費の最適化、排出の最小化、利益率の向上というプレッシャーに直面し続けているため、エネルギー効率の高いシステムに対する需要は着実に伸びています。これらの回収ソリューションは、全体的な持続可能性指標を向上させながら、運転に必要な燃料の量を削減することで、プラントの効率を改善する上で重要な役割を果たしています。廃熱回収システムの採用は、重工業におけるよりクリーンな技術の使用を奨励する環境指令や規制枠組みによってさらに後押しされています。

廃熱回収システムは、セメント生産プロセスのいくつかの段階に適用されます。主な応用分野には、予熱、発電、蒸気発生、その他のプロセス強化が含まれます。このうち、予熱分野は2024年に54億米ドルを占める。この分野では、キルンに入る前に高温の排ガスを回収して原料を加熱します。このアプローチを利用することで、燃料消費を大幅に削減し、生産時間を短縮し、操業効率を向上させることができます。製造の初期段階でエネルギーの再利用を最適化することで、メーカーは生産コストを全体的に削減しながら、安定した生産量を維持することができます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 158億米ドル |

| 予測金額 | 326億米ドル |

| CAGR | 7.7% |

温度カテゴリーでは、市場は230℃で動作するシステム、230℃~650℃で動作するシステム、650℃を超えるシステムに区分されます。2024年には、650℃を超える温度が世界市場の70.6%以上を占め、最大の収益シェアを占めています。これらの高温システムは、クリンカ製造段階で発生する極端な熱レベルのため、セメント工場に特に効果的です。一方、より低い温度で作動するシステムは、一般に、材料の予備乾燥や施設内の周囲空間の暖房などの作業に導入されます。これらのシステムは、高温システムと同レベルのエネルギー回収を提供するわけではないが、比較的シンプルで予算に優しいため、大規模な資本支出を行わずにエネルギーコストの削減を目指す小規模なセメント事業にとっては、実用的な選択肢となります。

北米では、米国でセメント廃熱回収システムの採用が着実に増加しています。同国の市場評価額は、2022年の4億4,000万米ドルから2023年には4億6,000万米ドルに成長し、2024年には4億8,000万米ドルに達しました。セメントインフラの老朽化に加え、二酸化炭素排出量の削減が重視されるようになったことで、企業はよりエネルギー効率の高いシステムへのアップグレードを促しています。連邦政府の支援と奨励金も、熱回収技術の旧式プラントへの統合を促進する上で重要な役割を果たしています。企業がエネルギーコンプライアンス要件を満たし、操業生産高を向上させようと努力する中、先進的な熱エネルギー回収システムの採用は増加の一途をたどっています。

世界のセメント廃熱回収システム市場は適度に統合されており、少数の主要企業が業界シェアの大部分を占めています。シーメンス・エナジー、三菱重工業、サーマックス・リミテッド、川崎重工業などの主要企業は、2024年の市場シェアの約30%を占めています。これらの企業は、セメントキルンから発生する熱を利用可能な電気や蒸気に変換できる高効率システムの提供に注力しています。これらの企業の製品は、セメント生産者がエネルギー効率と排出削減の国際基準を満たすのを支援しながら、エネルギー浪費を最小限に抑えるのをサポートします。技術革新とカスタマイズされたソリューションを通じて、これらのメーカーは、セメント産業におけるエネルギー使用の未来を形作る上で役立っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 貿易への影響

- 展望と今後の検討事項

- 業界への影響要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア

- 戦略的取り組み

- 競合ベンチマーキング

- 戦略的ダッシュボード

- イノベーションとテクノロジーの情勢

第5章 市場規模・予測:用途別、2021-2034

- 主要動向

- 予熱

- 電気と蒸気の発電

- 蒸気ランキンサイクル

- 有機ランキンサイクル

- カリーナサイクル

- その他

第6章 市場規模・予測:温度別、2021-2034

- 主要動向

- 230℃

- 230℃~650℃

- 650℃以上

第7章 市場規模・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- アジア太平洋

- 中国

- オーストラリア

- インド

- 日本

- 韓国

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

第8章 企業プロファイル

- AURA

- Bosch Industriekessel GmbH

- Climeon

- CTP TEAM S.R.L

- Cochran

- Forbes Marshall

- IHI Corporation

- John Wood Group PLC

- Kawasaki Heavy Industries Ltd.

- MITSUBISHI HEAVY INDUSTRIES、LTD.

- Promec Engineering

- Sofinter S.p.a

- Siemens Energy

- Turboden S.p.A.

- Thermax Limited

The Global Cement Waste Heat Recovery System Market was valued at USD 15.8 billion in 2024 and is estimated to grow at a CAGR of 7.7% to reach USD 32.6 billion by 2034. The cement manufacturing process is one of the most energy-intensive industrial operations, with massive quantities of heat generated and often lost during production. Waste heat recovery systems are emerging as an essential solution to capture this unused thermal energy and redirect it toward power generation or process heating, resulting in substantial cost savings and reduced reliance on external energy sources. As cement manufacturers continue to face pressure to optimize energy consumption, minimize emissions, and increase profit margins, the demand for energy-efficient systems is experiencing steady growth. These recovery solutions play a critical role in improving plant efficiency by reducing the amount of fuel needed for operations while enhancing overall sustainability metrics. Their adoption is being further boosted by environmental mandates and regulatory frameworks encouraging the use of cleaner technologies in heavy industries.

Waste heat recovery systems find application across several stages of the cement production process. Key application areas include pre-heating, electricity and steam generation, and other process enhancements. Among these, the pre-heating segment accounted for USD 5.4 billion in 2024. This segment involves recovering high-temperature exhaust gases to heat raw materials before they enter the kiln. Utilizing this approach significantly cuts down on fuel consumption, shortens production times, and improves operational efficiency. By optimizing energy reuse at earlier stages of production, manufacturers are able to maintain consistent output while trimming down overall production costs.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $15.8 Billion |

| Forecast Value | $32.6 Billion |

| CAGR | 7.7% |

In terms of temperature categories, the market is segmented into systems operating at 230°C, between 230°C and 650°C, and those above 650°C. The segment capturing temperatures greater than 650°C held the largest revenue share in 2024, accounting for more than 70.6% of the global market. These high-temperature systems are particularly effective for cement plants due to the extreme heat levels generated during the clinker production stage. Meanwhile, systems that operate at lower temperatures are generally implemented for tasks such as material pre-drying or ambient space heating within facilities. While they do not offer the same level of energy recapture as high-temperature systems, they are relatively simple and budget-friendly, making them a practical option for smaller-scale cement operations that still aim to reduce energy costs without undertaking large capital expenditures.

In North America, the United States has shown a steady increase in the adoption of cement waste heat recovery systems. Market valuation in the country grew from USD 440 million in 2022 to USD 460 million in 2023 and reached USD 480 million in 2024. A growing emphasis on reducing carbon emissions, along with aging cement infrastructure, is encouraging companies to upgrade to more energy-efficient systems. Federal support and incentives are also playing a vital role in driving the integration of heat recovery technologies into older plants. As companies strive to meet energy compliance requirements and enhance operational output, the adoption of advanced thermal energy recovery systems continues to rise.

The global cement waste heat recovery system market is moderately consolidated, with a few key players holding a significant portion of the industry share. Leading companies such as Siemens Energy, Mitsubishi Heavy Industries, Ltd., Thermax Limited, and Kawasaki Heavy Industries Ltd. collectively accounted for approximately 30% of the market share in 2024. These companies focus on delivering high-efficiency systems capable of converting heat generated from cement kilns into usable electricity or steam. Their offerings support cement producers in minimizing energy waste while helping them meet international standards for energy efficiency and emissions reduction. Through technological innovation and customized solutions, these manufacturers are instrumental in shaping the future of energy use in the cement industry.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data Collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculations

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.1 Impact on trade

- 3.3 Outlook and future considerations

- 3.4 Industry impact forces

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share

- 4.3 Strategic initiative

- 4.4 Competitive benchmarking

- 4.5 Strategic dashboard

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Application, 2021 - 2034 (USD Billion)

- 5.1 Key trends

- 5.2 Pre-heating

- 5.3 Electricity & steam generation

- 5.3.1 Steam rankine cycle

- 5.3.2 Organic rankine cycle

- 5.3.3 Kalina cycle

- 5.4 Other

Chapter 6 Market Size and Forecast, By Temperature, 2021 - 2034 (USD Billion)

- 6.1 Key trends

- 6.2 230°C

- 6.3 230°C - 650 °C

- 6.4 > 650 °C

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 (USD Billion)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Spain

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Australia

- 7.4.3 India

- 7.4.4 Japan

- 7.4.5 South Korea

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 South Africa

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 AURA

- 8.2 Bosch Industriekessel GmbH

- 8.3 Climeon

- 8.4 CTP TEAM S.R.L

- 8.5 Cochran

- 8.6 Forbes Marshall

- 8.7 IHI Corporation

- 8.8 John Wood Group PLC

- 8.9 Kawasaki Heavy Industries Ltd.

- 8.10 MITSUBISHI HEAVY INDUSTRIES, LTD.

- 8.11 Promec Engineering

- 8.12 Sofinter S.p.a

- 8.13 Siemens Energy

- 8.14 Turboden S.p.A.

- 8.15 Thermax Limited