|

|

市場調査レポート

商品コード

1699341

GaN半導体デバイス市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測GaN Semiconductor Device Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| GaN半導体デバイス市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月24日

発行: Global Market Insights Inc.

ページ情報: 英文 210 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

世界のGaN半導体デバイス市場は2024年に226億米ドルに達し、2025年から2034年にかけてCAGR 6.8%で拡大すると予測されています。

高性能でエネルギー効率に優れた電子部品に対する需要の高まりが市場成長の原動力となっており、GaN技術は複数の産業で支持され続けています。GaNはその優れた電気的特性により、従来のシリコンベースの半導体と比較して、より高速な処理速度、エネルギー効率の改善、より高い電力密度を可能にします。電気自動車、ワイヤレス充電、高周波通信ネットワークなどのアプリケーションでGaNの採用が増加していることから、GaNは次世代技術の重要なイネーブラーとして位置づけられています。さらに、産業界が持続可能性とエネルギー効率を追求する中、電力損失を低減し、システム性能を高めるGaNの能力は、メーカーに好まれる選択肢となっています。これらの利点により、GaNの研究開発への投資が増加し、GaNの商業化と普及がさらに加速しています。

GaN半導体デバイス需要の重要な原動力は、民生用電子機器への統合が進んでいることです。企業は、GaNの能力を活用して電力効率を改善しながら、より小型でコンパクトなフォームファクタを実現しています。これにより、メーカーはシステムコストを削減しながら高性能製品を開発することができ、GaNは充電器や電源、新興の電気自動車技術に好まれる材料となっています。GaNをさまざまな民生用および産業用アプリケーションに組み込む能力は、GaNの魅力を高め続け、広く市場に浸透する原動力となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 226億米ドル |

| 予測金額 | 434億米ドル |

| CAGR | 6.8% |

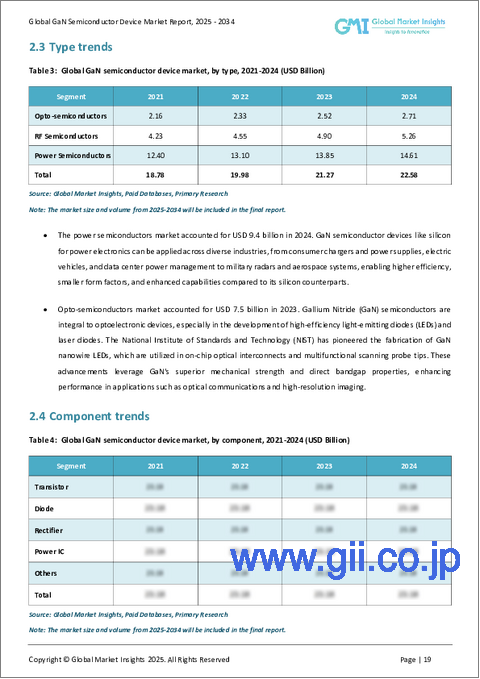

GaN半導体デバイス市場は、製品タイプ別に光半導体、RF半導体、パワー半導体に分類されます。パワー半導体だけでも2024年に94億米ドルを占め、高効率アプリケーションにおける重要な役割を反映しています。従来の半導体材料よりも高い電圧と温度で動作するGaNの能力は、データセンター、再生可能エネルギーシステム、電気自動車などの要求の厳しい分野に理想的です。企業が電源管理ソリューションの改善を求める中、GaNパワー半導体は持続的な需要と技術革新が期待されます。

コンポーネントの観点から、市場はトランジスタ、ダイオード、整流器、パワーIC、その他に区分されます。特にGaNトランジスタは、マイクロ波周波数での電力増幅において重要な役割を果たし、先端技術アプリケーションに不可欠なものとなっています。2024年現在、トランジスタはGaN半導体デバイス市場の36.3%を占めており、高温動作と優れた効率を必要とするアプリケーションにおける重要性の高まりを反映しています。これらの特性は、通信、航空宇宙、防衛など、信頼性の高い高性能半導体部品が不可欠な産業にとって極めて重要です。

米国のGaN半導体デバイス市場の評価額は2024年に53億米ドルに達し、GaN技術における同国のリーダーシップが浮き彫りになりました。商業的および国家安全保障上の利点を重視する米国は、GaN技術革新の最前線にいます。特に防衛分野は、レーダーシステムや電子戦技術などの重要なアプリケーションにGaNを統合しています。さらに、5Gの急速な展開と予想される6Gネットワークへの進化は、高周波通信インフラにおけるGaNの戦略的重要性をさらに際立たせています。産業界が効率、速度、性能を優先し続ける中、GaN技術は半導体進歩の未来を形作る上で極めて重要な役割を果たすと期待されています。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュース

- 規制状況

- 影響要因

- 促進要因

- 民生用電子機器におけるGaNの採用増加

- 自動車産業における統合の拡大

- 高速データ伝送への需要の高まり

- エネルギーおよび電力産業における展開の急増

- 業界の潜在的リスク&課題

- 高い製造コスト

- 熱管理の課題

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- 光半導体

- RF半導体

- パワー半導体

第6章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- トランジスタ

- ダイオード

- 整流器

- パワーIC

- その他

第7章 市場推計・予測:電圧範囲別、2021年~2034年

- 主要動向

- 100V未満

- 100-500 V

- 500V以上

第8章 市場推計・予測:最終用途産業別、2021年~2034年

- 主要動向

- 航空宇宙・防衛

- 自動車

- 家電

- エネルギー・電力

- ヘルスケア

- 産業

- IT・通信

- その他

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Aixtron SE

- Analog Devices

- Broadcom Inc.

- Efficient Power Conversion(EPC)

- Fuji Electric Co., Ltd.

- GaN Systems

- Infineon Technologies AG

- Kyocera Corporation

- MACOM Technology Solutions

- Mitsubishi Electric Corporation

- NXP Semiconductors

- Odyssey Semiconductor Technologies, Inc.

- ON Semiconductor

- Power Integrations

- Qorvo, Inc.

- Qualcomm

- Renesas Electronics Corporation

- Rohm Semiconductor

- Sanken Electric Co., Ltd.

- Skyworks Solutions

- STMicroelectronics

- Sumitomo Electric Industries Ltd.

- Texas Instruments

- Toshiba Corporation

- Wolfspeed

The Global GaN Semiconductor Device Market reached USD 22.6 billion in 2024 and is projected to expand at a CAGR of 6.8% from 2025 to 2034. The rising demand for high-performance, energy-efficient electronic components is fueling market growth, as GaN technology continues to gain traction across multiple industries. With its superior electrical properties, GaN enables faster processing speeds, improved energy efficiency, and greater power density compared to traditional silicon-based semiconductors. The increasing adoption of GaN in applications such as electric vehicles, wireless charging, and high-frequency communication networks is positioning it as a key enabler of next-generation technology. Additionally, as industries move toward sustainability and energy efficiency, GaN's ability to reduce power losses and enhance system performance makes it a preferred choice among manufacturers. These advantages are leading to increased investments in GaN research and development, further accelerating its commercialization and widespread adoption.

A significant driver of GaN semiconductor device demand is its growing integration into consumer electronics. Companies are leveraging GaN's capability to improve power efficiency while enabling smaller, more compact form factors. This allows manufacturers to develop high-performance products with reduced system costs, making GaN a preferred material for chargers, power supplies, and emerging electric vehicle technologies. The ability to incorporate GaN into various consumer and industrial applications continues to elevate its appeal, driving widespread market penetration.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $22.6 Billion |

| Forecast Value | $43.4 Billion |

| CAGR | 6.8% |

The GaN semiconductor device market is categorized by product type into opto-semiconductors, RF semiconductors, and power semiconductors. Power semiconductors alone accounted for USD 9.4 billion in 2024, reflecting their essential role in high-efficiency applications. GaN's ability to operate at higher voltages and temperatures than conventional semiconductor materials makes it ideal for demanding sectors such as data centers, renewable energy systems, and electric vehicles. As companies seek to improve power management solutions, GaN power semiconductors are expected to witness sustained demand and innovation.

From a component perspective, the market is segmented into transistors, diodes, rectifiers, power ICs, and others. GaN transistors, in particular, play a crucial role in power amplification at microwave frequencies, making them indispensable for advanced technological applications. As of 2024, transistors represented 36.3% of the GaN semiconductor device market, reflecting their growing importance in applications requiring high-temperature operation and superior efficiency. These attributes are crucial for industries such as telecommunications, aerospace, and defense, where reliable, high-performance semiconductor components are vital.

The U.S. GaN Semiconductor Device Market reached a valuation of USD 5.3 billion in 2024, underscoring the country's leadership in GaN technology. With a strong emphasis on commercial and national security advantages, the U.S. is at the forefront of GaN innovation. The defense sector, in particular, has integrated GaN into critical applications such as radar systems and electronic warfare technologies. Additionally, the rapid deployment of 5G and the anticipated evolution to 6G networks further highlight GaN's strategic importance in high-frequency communication infrastructure. As industries continue to prioritize efficiency, speed, and performance, GaN technology is expected to play a pivotal role in shaping the future of semiconductor advancements.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing adoption of GaN in consumer electronics

- 3.6.1.2 Growing integration in the automotive industry

- 3.6.1.3 Rising demand for high-speed data transmission

- 3.6.1.4 Surging deployment in the energy and power industry

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High manufacturing costs

- 3.6.2.2 Thermal management challenges

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034 (USD Billion)

- 5.1 Key trends

- 5.2 Opto-semiconductors

- 5.3 RF semiconductors

- 5.4 Power semiconductors

Chapter 6 Market Estimates & Forecast, By Component, 2021-2034 (USD Billion)

- 6.1 Key trends

- 6.2 Transistor

- 6.3 Diode

- 6.4 Rectifier

- 6.5 Power IC

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Voltage Range, 2021-2034 (USD Billion)

- 7.1 Key trends

- 7.2 Less than 100 V

- 7.3 100-500 V

- 7.4 More than 500 V

Chapter 8 Market Estimates & Forecast, By End Use Industry, 2021-2034 (USD Billion)

- 8.1 Key trends

- 8.2 Aerospace & defense

- 8.3 Automotive

- 8.4 Consumer electronics

- 8.5 Energy & power

- 8.6 Healthcare

- 8.7 Industrial

- 8.8 IT & telecommunications

- 8.9 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Aixtron SE

- 10.2 Analog Devices

- 10.3 Broadcom Inc.

- 10.4 Efficient Power Conversion (EPC)

- 10.5 Fuji Electric Co., Ltd.

- 10.6 GaN Systems

- 10.7 Infineon Technologies AG

- 10.8 Kyocera Corporation

- 10.9 MACOM Technology Solutions

- 10.10 Mitsubishi Electric Corporation

- 10.11 NXP Semiconductors

- 10.12 Odyssey Semiconductor Technologies, Inc.

- 10.13 ON Semiconductor

- 10.14 Power Integrations

- 10.15 Qorvo, Inc.

- 10.16 Qualcomm

- 10.17 Renesas Electronics Corporation

- 10.18 Rohm Semiconductor

- 10.19 Sanken Electric Co., Ltd.

- 10.20 Skyworks Solutions

- 10.21 STMicroelectronics

- 10.22 Sumitomo Electric Industries Ltd.

- 10.23 Texas Instruments

- 10.24 Toshiba Corporation

- 10.25 Wolfspeed