|

市場調査レポート

商品コード

1928967

ドライマリンスクラバーシステムの市場機会、成長要因、業界動向分析、および2026年から2035年までの予測Dry Marine Scrubber Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| ドライマリンスクラバーシステムの市場機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2026年01月13日

発行: Global Market Insights Inc.

ページ情報: 英文 114 Pages

納期: 2~3営業日

|

概要

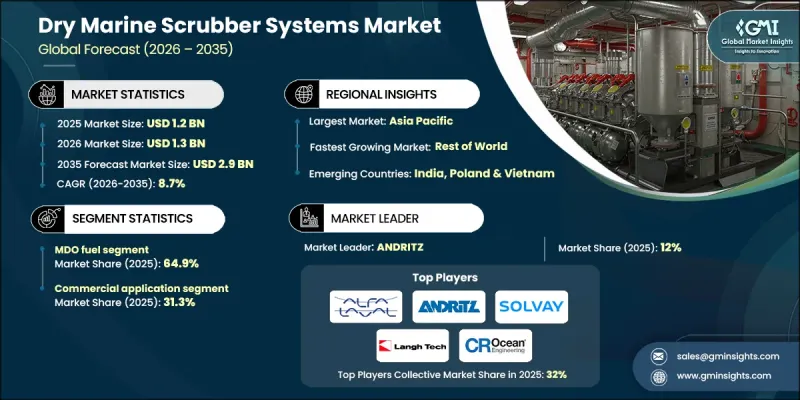

世界のドライマリンスクラバーシステム市場は、2025年に12億米ドルと評価され、2035年までにCAGR8.7%で成長し、29億米ドルに達すると予測されています。

この成長は、海運業界全体のコンプライアンス戦略を再構築している、ますます厳格化する排出規制によって推進されています。船舶運航者は、硫黄および窒素酸化物の排出制限を満たしつつ、運用コストを管理し、規制上の罰則を回避するために、ドライスクラバーシステムを採用しています。これらのシステムは、大規模なエンジン改造を必要とせずに規制遵守を可能にするため、効率的で商業的に実現可能な選択肢となっています。ドライマシンスクラバーは、有害な排気成分を大気放出前に捕捉することで、大気汚染物質の削減に重要な役割を果たします。その使用は、よりクリーンな海運業務を支援し、港湾周辺の大気質を改善し、高まる持続可能性への期待に沿うものです。技術開発への継続的な投資により、あらゆる船舶カテゴリーにおいてシステムの効率性、信頼性、適応性が向上しています。ライフサイクルコストの削減と運用簡素化に焦点を当てた改良が、ますます採用されています。事業者が環境義務と収益性のバランスを取る中、ドライスクラバーシステムは現代の船隊戦略において不可欠な解決策となりつつあります。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 12億米ドル |

| 予測金額 | 29億米ドル |

| CAGR | 8.7% |

船舶用軽油セグメントは2025年に64.9%のシェアを占め、2035年までCAGR8.5%で成長すると予測されています。需要は硫黄規制の強化と、燃料がドライスクラバー技術との互換性を持つことにより支えられており、これにより大きな技術的変更なしに規制遵守が可能となります。

レクリエーション船舶セグメントは、2035年までにCAGR8.5%で成長すると予測されています。所有者が規制基準を満たしつつ、スペース効率と船舶デザインを維持できるコンパクトな排出ガス制御ソリューションへの投資が増加しているため、採用が進んでいます。

米国ドライマリンスクラバーシステム市場は2025年に71.9%のシェアを占め、2035年までに4億7,000万米ドル以上の収益を生み出すと予測されています。強力な規制執行とゼロ排出要件が導入を加速させており、ドライスクラバーは優先的なコンプライアンスソリューションとして位置づけられています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界のエコシステム

- 原材料の入手可能性と調達分析

- 製造能力評価

- サプライチェーンの回復力とリスク要因

- 流通ネットワーク分析

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- コスト構造分析

- ポーターの分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- PESTEL分析

- 新たな機会と動向

- デジタル化とIoT統合

- 新興市場への進出

- 投資分析と将来展望

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析:地域別

- 北米

- 欧州

- アジア太平洋地域

- 世界のその他の地域

- 戦略的ダッシュボード

- 戦略的取り組み

- 企業ベンチマーキング

- イノベーションと技術動向

第5章 市場規模・予測:燃料別、2022-2035

- MDO

- MGO

- ハイブリッド

- その他

第6章 市場規模・予測:用途別、2022-2035

- 商業用

- オフショア

- レクリエーション

- 海軍

- その他

第7章 市場規模・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ギリシャ

- ノルウェー

- ドイツ

- 英国

- フランス

- オランダ

- イタリア

- アジア太平洋地域

- 中国

- 韓国

- 日本

- ベトナム

- インド

- オーストラリア

- 世界のその他の地域

第8章 企業プロファイル

- ANDRITZ

- Aarco Engineering Projects Pvt. Ltd.

- Albion Marine Solutions

- Alfa Laval

- ブレンタグ・アジア太平洋株式会社

- Clean Marine

- CR Ocean Engineering

- DuPont Clean Technologies

- Ecospray Technologies

- Fuji Electric

- Langh Tech

- ME Production

- Nicro

- SAACKE

- Solvay

- VDL AEC Maritime

- Yara Marine Technologies