|

|

市場調査レポート

商品コード

1460125

自動車用スマートアンテナ市場規模:車両別、コンポーネント別、アンテナ別、周波数別、販売チャネル別、予測、2024年~2032年Automotive Smart Antenna Market Size - By Vehicle (Passenger Cars, Commercial Vehicles, Electric Vehicles), Component (Transceiver, Electronic Control Unit, Connector), Antenna (Shark-fin, Fixed Mast), Frequency, Sales Channel & Forecast, 2024 - 2032 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 自動車用スマートアンテナ市場規模:車両別、コンポーネント別、アンテナ別、周波数別、販売チャネル別、予測、2024年~2032年 |

|

出版日: 2024年02月15日

発行: Global Market Insights Inc.

ページ情報: 英文 265 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

自動車用スマートアンテナナ市場規模は、自動車分野におけるIoTの拡大に牽引され、2024年から2032年にかけて6.5%以上で拡大する見通しです。

自動車におけるIoT統合は、高度なデータ収集、分析、通信機能を可能にすることで、自動車産業に革命をもたらしています。スマートアンテナはこのエコシステムにおいて極めて重要な役割を果たしており、車両診断、予知保全、リアルタイムモニタリングなどのIoTアプリケーションのシームレスな接続を促進しています。自動車メーカーが 促進要因の体験、安全性、効率性を高めるためにIoT技術を採用する中、スマートアンテナの需要は今後も急増します。例えば、LGエレクトロニクスは2023年12月、フランスの有名ガラスメーカーであるサンゴバン・セキュリットと共同で、自動車のガラスに直接取り付けることができる透明フィルムタイプの自動車用アンテナを開発しました。この透明なテレマティクス・ソリューションは、急成長するモビリティ業界に波及する可能性が高く、自動車ソリューション分野におけるLGの地位を強化します。

自動車用スマートアンテナ産業は、車両、部品、アンテナ、周波数、販売チャネル、地域に区分されます。

車両別では、電動化へのシフトの高まりにより、電気自動車(EV)セグメントの市場規模が2024~2032年に大幅な成長を記録すると予測されています。EVは、効率的なバッテリー管理、ナビゲーション、自律走行機能のために高度な接続性を必要とします。そのため、スマートアンテナは、EVの性能とユーザーエクスペリエンスに不可欠な受信とデータ転送の改善を提供します。さらに、ビームフォーミングや5G統合などの進歩は、航続距離予測、充電効率、全体的な接続性を強化する電気自動車独自のニーズに対応し、セグメントの成長に拍車をかけています。例えば、TE Connectivityは2023年8月、LTE/5G、Wi-Fi 6E/7、Bluetoothなど多くの機能を1つに統合したFP20およびFP40マルチポートアンテナを発表し、設置の簡素化、ルーフの乱雑さの最小化、美観の向上を実現しました。

アンテナに関しては、シャークフィンアンテナセグメントの自動車用スマートアンテナ市場は2023年に大きな収益を上げ、2032年まで大きな牽引力を獲得すると推定されます。シャークフィンアンテナは、優れた接続性を提供しながら、車両デザインにシームレスに統合するための美観と機能性の融合を提供します。そのコンパクトなデザインにGPS、Wi-Fi、セルラー接続などの先進技術が搭載されているため、スマートアンテナはメーカーにも消費者にも魅力的です。さらに、自動車メーカーは空気力学と美観を優先しており、製品需要をさらに押し上げています。

地域別に見ると、北米の自動車用スマートアンテナ産業は、2024年から2032年にかけて堅調な成長を示すと見られています。シームレスな通信がますます重視される中、これらのアンテナはナビゲーション、インフォテインメント、自律走行システムにおいて強化された性能を提供します。多入力多出力(MIMO)技術のような革新は、受信品質とデータ速度を向上させ、中断のない接続を求める消費者の欲求をさらに引き立てています。さらに、業界のリーダーたちは研究開発活動に多額の投資を行っており、この地域の市場成長に貢献しています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- 技術プロバイダー

- 検査サービス

- サプライヤーとディストリビューター

- エンドユーザー

- 利益率分析

- 技術とイノベーションの展望

- 特許分析

- 主要ニュース&イニシアチブ

- 規制状況

- 影響要因

- 促進要因

- コネクテッドカーの需要増加

- 通信技術の進歩

- 自動車の安全性と自律走行の重視

- 緊急通報(eCall)システムなどの安全機能の搭載を義務付ける厳しい政府規制

- 業界の潜在的リスク&課題

- 実装のコストと複雑さ

- 干渉と互換性の問題

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:車両別、2018年~2032年

- 主要動向

- 乗用車

- 商用車

- 電気自動車(EV)

- バッテリー電気自動車(BEV)

- 燃料電池電気自動車(FCEV)

- プラグインハイブリッド車(PHEV)

第6章 市場推計・予測:コンポーネント別、2018年~2032年

- 主要動向

- トランシーバー

- 電子制御ユニット(ECU)

- コネクター

- その他

第7章 市場推計・予測:アンテナ別、2018年~2032年

- 主要動向

- シャークフィン

- 固定マスト

- その他

第8章 市場推計・予測:周波数別、2018年~2032年

- 主要動向

- 短波(3 MHz-30 MHz)

- 超短波(31 MHz-300 MHz)

- 極超短波(301 MHz~3 GHz)

第9章 市場推計・予測:販売チャネル別、2018年~2032年

- 主要動向

- OEM

- アフターマーケット

第10章 市場推計・予測:地域別、2018年~2032年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- 北欧

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- その他のMEA

第11章 企業プロファイル

- Airgain Inc.

- Anokiwave

- Antenova M2M

- Autotalks Ltd.

- Calearo Antenne S.p.A

- ExPhase Technologies

- Ficosa Internacional SA

- Forvia

- Harada

- Harman International

- Hirschmann Car Communication GmbH

- Kathrein Automotive

- KYMETA Corporation

- Laird

- MetaWave Corporation

- Rosenberger OSI

- Schaffner

- WISI Automotive GmbH

- WORLD PRODUCTS INC.

- Yokowo

Automotive Smart Antenna Market size is poised to expand at over 6.5% between 2024 and 2032 driven by the expansion of the IoT in the automotive sector.

IoT integration in vehicles is revolutionizing the automotive industry by enabling advanced data collection, analytics, and communication capabilities. Smart antennas play a pivotal role in this ecosystem, facilitating seamless connectivity for IoT applications like vehicle diagnostics, predictive maintenance, and real-time monitoring. With automakers embracing IoT technologies to enhance driver experience, safety, and efficiency, the demand for smart antennas will continue to surge. For instance, in December 2023, LG Electronics collaborated with Saint-Gobain Sekurit, a well-known French glass maker, to create a transparent film-type antenna for vehicles that can be mounted directly to vehicle glass. This transparent telematics solution is likely to make waves in the fast-growing mobility industry, bolstering position of LG in the automotive solutions sector.

The automotive smart antenna industry is segmented into vehicle, component, antenna, frequency, sales channel, and region.

Based on vehicle, the market size from the electric vehicles (EV) segment is projected to record substantial growth from 2024-2032, due to the rising shift towards electrification. EVs need sophisticated connectivity for efficient battery management, navigation, and autonomous features. To that end, smart antennas offer improved reception and data transfer crucial for EV performance and user experience. Moreover, advancements, such as beamforming and 5G integration are catering to the unique needs of electric vehicles for enhancing range estimation, charging efficiency, and overall connectivity, adding to the segment growth. For instance, in August 2023, TE Connectivity introduced the FP20 and FP40multi-port antennas integrating many functionalities like LTE/5G, Wi-Fi 6E/7, and Bluetooth into one for simplifying installation, minimizing roof clutter, and improving aesthetics.

In terms of antenna, the automotive smart antenna market from the shark-fin antenna segment generated substantial revenue in 2023 and is estimated to gain significant traction through 2032. Shark-fin antennas offer a blend of aesthetics and functionality for seamlessly integrating with vehicle designs while providing superior connectivity. As their compact design houses advanced technologies, such as GPS, Wi-Fi, and cellular connectivity, smart antennas appeal to manufacturers and consumers alike. Additionally, automakers are prioritizing aerodynamics and aesthetics, further boosting the product demand.

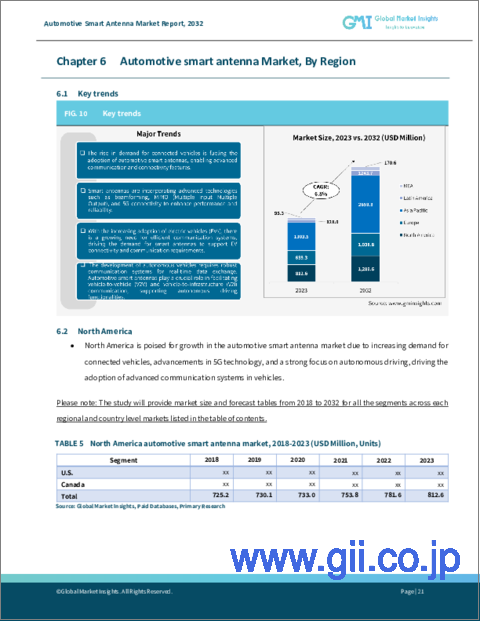

Given the regional landscape, the North America automotive smart antenna industry is set to exhibit robust growth from 2024 to 2032 attributed to the escalating demand for advanced connectivity in vehicles. With an ever-increasing emphasis on seamless communication, these antennas offer enhanced performance in navigation, infotainment, and autonomous driving systems. Innovations like multiple-input and multiple-output (MIMO) technologies are augmenting reception quality and data speeds, further appealing the desire of consumers for uninterrupted connectivity. Furthermore, industry leaders are investing heavily in R&D activities for driving advancements, contributing to the regional market growth.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry 360 degree synopsis, 2018-2032

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Technology providers

- 3.2.2 Testing services

- 3.2.3 Suppliers & distributors

- 3.2.4 End users

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Increasing demand for connected vehicles

- 3.8.1.2 Advancements in communication technologies

- 3.8.1.3 Emphasis on vehicle safety and autonomous driving

- 3.8.1.4 Stringent government regulations mandating the inclusion of safety features, such as emergency call (eCall) systems

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 Cost and complexity of implementation

- 3.8.2.2 Interference and compatibility issues

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.10.1 Supplier power

- 3.10.2 Buyer power

- 3.10.3 Threat of new entrants

- 3.10.4 Threat of substitutes

- 3.10.5 Industry rivalry

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2023

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Vehicle, 2018-2032 ($Bn, Units)

- 5.1 Key trends

- 5.2 Passenger cars

- 5.3 Commercial vehicles

- 5.4 Electric vehicles (EVs)

- 5.4.1 Battery electric vehicle (BEVs)

- 5.4.2 Fuel cell electric vehicle (FCEVs)

- 5.4.3 Plug-in hybrid vehicle (PHEVs)

Chapter 6 Market Estimates & Forecast, By Component, 2018-2032 ($Bn)

- 6.1 Key trends

- 6.2 Transceiver

- 6.3 Electronic control unit (ECU)

- 6.4 Connector

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Antenna, 2018-2032 ($Bn, Units)

- 7.1 Key trends

- 7.2 Shark-fin

- 7.3 Fixed mast

- 7.4 Others

Chapter 8 Market Estimates & Forecast, By Frequency, 2018-2032 ($Bn, Units)

- 8.1 Key trends

- 8.2 High frequency (3 MHz - 30 MHz)

- 8.3 Very high frequency (31 MHz - 300 MHz)

- 8.4 Ultra-high frequency (301 MHz - 3 GHz)

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2018-2032 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEMs

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2018-2032 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.4.7 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Rest of MEA

Chapter 11 Company Profiles

- 11.1 Airgain Inc.

- 11.2 Anokiwave

- 11.3 Antenova M2M

- 11.4 Autotalks Ltd.

- 11.5 Calearo Antenne S.p.A

- 11.6 ExPhase Technologies

- 11.7 Ficosa Internacional SA

- 11.8 Forvia

- 11.9 Harada

- 11.10 Harman International

- 11.11 Hirschmann Car Communication GmbH

- 11.12 Kathrein Automotive

- 11.13 KYMETA Corporation

- 11.14 Laird

- 11.15 MetaWave Corporation

- 11.16 Rosenberger OSI

- 11.17 Schaffner

- 11.18 WISI Automotive GmbH

- 11.19 WORLD PRODUCTS INC.

- 11.20 Yokowo