|

市場調査レポート

商品コード

1766346

電子リクローザ市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Electronic Recloser Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 電子リクローザ市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年06月10日

発行: Global Market Insights Inc.

ページ情報: 英文 142 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

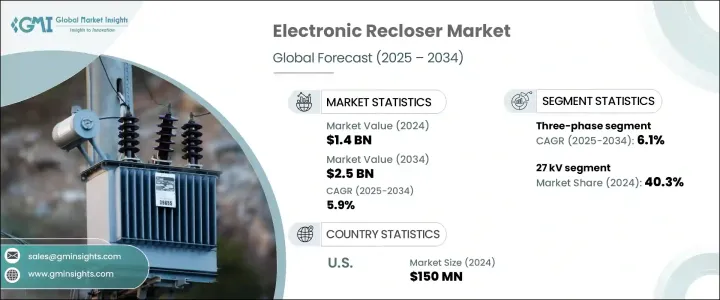

電子リクローザの世界市場規模は、2024年に14億米ドルとなり、CAGR 5.9%で成長し、2034年には25億米ドルに達すると予測されています。

この成長の背景には、老朽化した送電網インフラの近代化、配電効率の向上、再生可能エネルギー源の統合といったニーズがあります。電子リクローザは、自動故障検出と復旧を可能にすることで、ダウンタイムを減らし、システムの信頼性を向上させるスマートグリッドで重要な役割を果たしています。技術の進歩により、センサー、通信機能、モノのインターネット(IoT)プラットフォームとの統合が強化されたリクローザが開発され、採用がさらに加速しています。

さらに、信頼性が高くインテリジェントなグリッドシステムに対する需要の高まり、有利な政府インセンティブ、電気インフラ近代化への大規模投資などが、電子リクローザ市場の成長を引き続き後押ししています。ユーティリティ企業やグリッド運営者が自動化やよりスマートなエネルギー管理へとシフトする中、電子リクローザは迅速な故障検出をサポートし、電力中断を最小限に抑え、システム全体の回復力を高めるために統合されつつあります。分散型エネルギー資源の導入と再生可能エネルギーの統合が進み、安定性とサービスの継続性を維持するためにリアルタイムのグリッド応答性が不可欠となる中、その役割はさらに重要になっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 14億米ドル |

| 予測金額 | 25億米ドル |

| CAGR | 5.9% |

三相セグメントは、高負荷でミッションクリティカルな配電ネットワークへの設置を反映し、2034年までCAGR 6.1%で成長すると予測されます。これらのリクローザは、電力の三相すべてにわたって包括的な保護を提供するため、大規模な商業施設や産業施設におけるヘビーデューティー用途に適しています。故障を切り離し、手動介入なしに自動的に電力を復旧させるその能力は、ダウンタイムを最小限に抑えなければならない大容量送電網に不可欠です。

2024年には、15kVセグメントの市場評価額は5億3,550万米ドルに達します。この電圧クラスは中電圧システムに広く導入されており、都市部と農村部の両方の配電網の標準仕様となっています。この電圧クラスの人気は、住宅地、軽工業団地、電力会社の変電所においてコスト効率と信頼性の高い故障管理を実現し、電力会社が多様な運転条件下で中断のないサービスを維持できることに起因しています。

米国の電子リクローザ2024年の市場規模は1億5,000万米ドルで、過去数年間の一貫した成長を反映しています。この増加傾向は、老朽化した電力インフラの更新と高度なグリッド技術の導入に国が注力していることが大きな要因となっています。老朽化したシステムのアップグレードは、現在のエネルギー需要に対応し、送電網の安定性を確保し、将来の持続可能性目標を達成するために不可欠です。さらに、規制機関が定める厳格な性能・信頼性基準に準拠することで、高度な診断、遠隔操作機能、シームレスなグリッド統合を提供する次世代リクローザの採用が増加しています。

世界の電子リクローザ市場で事業を展開する主要企業には、ABB、Arteche、Eaton、Ensto、Entec Electric &Electronic、G&W Electric、Hubbell、Hughes Power System、NOJA Power Switchgear Pty Ltd、Rockwell、S&C Electric Company、Schneider Electric、Shinsung Industrial Electric、Siemens、Tavrida Electricなどがあります。これらの企業は、競合情勢における地位を強化するため、製品革新、戦略的パートナーシップ、市場プレゼンスの拡大に注力しています。市場でのプレゼンスを強化するために、電子リクローザ業界の企業はいくつかの重要な戦略を採用しています。研究開発に投資し、製品提供の革新と改善を図り、最新の配電システムの進化するニーズに確実に応えています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 規制情勢

- 業界への影響要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 戦略的取り組み

- 競合ベンチマーキング

- 戦略的ダッシュボード

- イノベーションとテクノロジーの情勢

第5章 市場規模・予測:フェーズ別、2021年~2034年

- 主要動向

- 単相

- 三相

第6章 市場規模・予測:インタラプション別、2021年~2034年

- 主要動向

- オイル

- 真空

第7章 市場規模・予測:電圧定格別、2021年~2034年

- 主要動向

- 15kV

- 27kV

- 38kV

第8章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- ロシア

- イタリア

- アジア太平洋地域

- 中国

- オーストラリア

- インド

- 日本

- 韓国

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

- チリ

第9章 企業プロファイル

- ABB

- ARTECHE

- Eaton

- ENSTO

- ENTEC Electric &Electronic

- G&W Electric

- Hubbell

- Hughes Power System

- NOJA Power Switchgear Pty Ltd

- Rockwill

- S&C Electric Company

- Schneider Electric

- Shinsung Industrial Electric

- Siemens

- Tavrida Electric

The Global Electronic Recloser Market was valued at USD 1.4 billion in 2024 and is estimated to grow at a CAGR of 5.9% to reach USD 2.5 billion by 2034. This growth is driven by the need to modernize aging grid infrastructure, enhance power distribution efficiency, and integrate renewable energy sources. Electronic reclosers play a crucial role in smart grids by enabling automated fault detection and restoration, thereby reducing downtime and improving system reliability. Technological advancements have led to the development of reclosers with enhanced sensors, communication capabilities, and integration with Internet of Things (IoT) platforms, further boosting their adoption.

Additionally, the rising demand for dependable and intelligent grid systems, alongside favorable government incentives and large-scale investments in electrical infrastructure modernization, continues to fuel growth in the electronic recloser market. As utilities and grid operators shift toward automation and smarter energy management, electronic reclosers are being integrated to support rapid fault detection, minimize power interruptions, and enhance overall system resilience. Their role becomes even more critical with the growing deployment of distributed energy resources and renewable energy integration, where real-time grid responsiveness is essential for maintaining stability and service continuity.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.4 Billion |

| Forecast Value | $2.5 Billion |

| CAGR | 5.9% |

The three-phase segment is anticipated to grow at a CAGR of 6.1% through 2034, reflecting installations in high-load and mission-critical distribution networks. These reclosers provide comprehensive protection across all three phases of power, making them well-suited for heavy-duty applications in large-scale commercial and industrial facilities. Their ability to isolate faults and automatically restore power without manual intervention makes them indispensable in high-capacity grids where downtime must be minimized.

In 2024, the 15kV segment reached a market valuation of USD 535.5 million. This voltage class is widely deployed in medium-voltage systems and serves as a standard specification for both urban and rural distribution networks. Its popularity stems from its ability to deliver cost-effective and reliable fault management in residential zones, light industrial parks, and utility substations, enabling utilities to maintain uninterrupted service in diverse operating conditions.

United States Electronic Recloser Market was valued at USD 150 million in 2024, reflecting consistent growth over the previous years. This upward trend is largely driven by the nation's focus on replacing aging power infrastructure and deploying advanced grid technologies. Upgrades to outdated systems are essential for addressing current energy demands, ensuring grid stability, and achieving future sustainability goals. Additionally, compliance with strict performance and reliability standards set by regulatory bodies has increased the adoption of next-generation reclosers, which offer advanced diagnostics, remote operation capabilities, and seamless grid integration.

Key players operating in the Global Electronic Recloser Market include ABB, Arteche, Eaton, Ensto, Entec Electric & Electronic, G&W Electric, Hubbell, Hughes Power System, NOJA Power Switchgear Pty Ltd, Rockwell, S&C Electric Company, Schneider Electric, Shinsung Industrial Electric, Siemens, and Tavrida Electric. These companies are focusing on product innovation, strategic partnerships, and expanding their market presence to strengthen their positions in the competitive landscape. To strengthen their market presence, companies in the electronic recloser industry are adopting several key strategies. They are investing in research and development to innovate and improve product offerings, ensuring they meet the evolving needs of modern power distribution systems.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, 2024

- 4.3 Strategic initiative

- 4.4 Competitive benchmarking

- 4.5 Strategic dashboard

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Phase, 2021 - 2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 Single phase

- 5.3 Three phase

Chapter 6 Market Size and Forecast, By Interruption, 2021 - 2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Oil

- 6.3 Vacuum

Chapter 7 Market Size and Forecast, By Voltage Rating, 2021 - 2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 15 kV

- 7.3 27 kV

- 7.4 38 kV

Chapter 8 Market Size and Forecast, By Region, 2021 - 2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Russia

- 8.3.5 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Australia

- 8.4.3 India

- 8.4.4 Japan

- 8.4.5 South Korea

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

- 8.6.3 Chile

Chapter 9 Company Profiles

- 9.1 ABB

- 9.2 ARTECHE

- 9.3 Eaton

- 9.4 ENSTO

- 9.5 ENTEC Electric & Electronic

- 9.6 G&W Electric

- 9.7 Hubbell

- 9.8 Hughes Power System

- 9.9 NOJA Power Switchgear Pty Ltd

- 9.10 Rockwill

- 9.11 S&C Electric Company

- 9.12 Schneider Electric

- 9.13 Shinsung Industrial Electric

- 9.14 Siemens

- 9.15 Tavrida Electric