|

市場調査レポート

商品コード

1716609

心律動管理デバイス市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Cardiac Rhythm Management Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 心律動管理デバイス市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月06日

発行: Global Market Insights Inc.

ページ情報: 英文 140 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

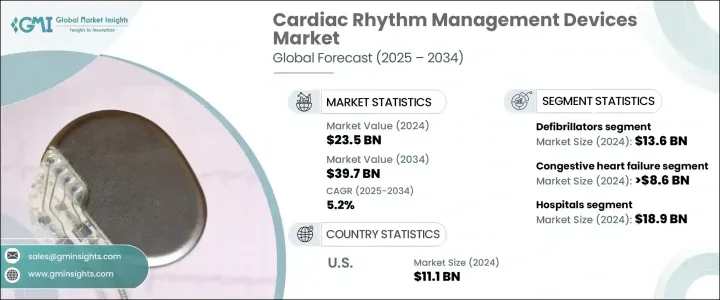

世界の心律動管理デバイス市場は、2024年に235億米ドルに達し、2025年から2034年にかけてCAGR 5.2%で拡大すると予測されています。

この市場の成長には、心不全、不整脈、その他のリズム関連疾患などの心血管疾患の世界の発生率の上昇が寄与しています。また、高齢者は心臓合併症を起こしやすいため、主要国での高齢化人口の着実な増加も市場拡大の原動力となっています。座りがちなライフスタイル、食生活の乱れ、高血圧、糖尿病、肥満の増加といった要因が、高度な心臓ケアソリューションの必要性をさらに高めています。

心血管系疾患が依然として世界の死亡の主因であることから、患者の予後を改善し、生活の質を高めることができる革新的で効果的な心律動管理デバイスに対する需要が高まっています。さらに、遠隔モニタリングや次世代植え込み型デバイスを含む医療技術の絶え間ない進歩は、ヘルスケアプロバイダーが心リズム障害を管理・治療する方法を変革しつつあります。ヘルスケア支出の急増は、早期診断と予防的心臓ケアに対する意識の高まりと相まって、市場プレーヤーに新たな機会をもたらすと期待されています。人工知能(AI)と機械学習(ML)の心臓リズム管理システムへの統合も、予測分析と個別化された治療選択肢を可能にすることで、今後の市場動向を牽引すると予想されます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 235億米ドル |

| 予測金額 | 397億米ドル |

| CAGR | 5.2% |

同市場は、ペースメーカー、除細動器、心臓再同期療法(CRT)機器など幅広い製品分野で構成されています。中でも除細動器は最大の市場シェアを占め、全体の収益に大きく貢献しています。除細動器、特に植え込み型除細動器(ICD)は、生命を脅かす不整脈のリスクが高い患者にとって不可欠です。これらの装置は、心臓のリズムを継続的に監視し、異常なリズムが検出されると電気ショックを与え、心臓突然死を防ぐように設計されています。心血管系疾患が世界的に罹患率および死亡率の主要な原因であり続けているため、除細動器の需要は着実に増加すると予想されます。

心律動管理デバイス市場は用途別では、うっ血性心不全、不整脈、徐脈、頻脈に区分されます。このうち、うっ血性心不全は2024年に86億米ドルを占める。ICDやCRTシステムのようなデバイスは、心臓のリズム調整を改善し、心拍出量を高め、疲労や息苦しさなどの症状を緩和して患者のQOLを向上させることにより、心不全の管理に重要な役割を果たしています。

米国の心律動管理デバイス市場は、2024年に111億米ドルを生み出し、世界市場を席巻しました。同国の先進的なヘルスケア・インフラは、有利な償還の枠組みや最先端の治療オプションへの幅広いアクセスと相まって、引き続き市場の成長を後押ししています。強力な臨床研究、継続的な製品イノベーション、研究開発への多額の投資が、米国におけるCRM機器の急速な普及を可能にし、この分野における世界的リーダーとしての地位を確固たるものにしています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 心不全およびその他の心臓疾患の有病率の増加

- 心臓リズムモニタリングの技術的進歩と革新的デバイスの導入

- 一般市民の意識の高まり

- 座りがちなライフスタイルの増加

- 有利な償還シナリオ

- 肥満の有病率の上昇と相まって増加する老人人口基盤

- 業界の潜在的リスク&課題

- 機器の高コスト

- 製品リコール

- 厳しい規制当局の承認

- 促進要因

- 成長可能性分析

- 規制状況

- 償還シナリオ

- 技術情勢

- 今後の市場動向

- 2024年の価格分析

- パイプライン製品

- 適応症の展望

- ユニット数、2021年~2034年

- ペースメーカー

- 除細動器

- CRTデバイス

- ポーター分析

- GAP分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 主要市場企業の競合分析

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- ペースメーカー

- 植込み型ペースメーカー

- 体外式ペースメーカー

- 除細動器

- 植込み型除細動器(ICD)

- 経静脈的植込み型除細動器

- 皮下植込み型除細動器

- シングルチャンバーICD

- デュアルチャンバーICD

- 体外式除細動器

- 手動式体外式除細動器

- 自動体外式除細動器

- 半自動体外式除細動器

- 全自動体外式除細動器

- 装着型除細動器

- 植込み型除細動器(ICD)

- 心臓再同期療法装置

- 心臓再同期療法機器-D

- 心臓再同期療法機器-P

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- うっ血性心不全

- 不整脈

- 徐脈

- 頻脈

- その他の用途

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 心臓治療センター

- 外来手術センター

- その他の最終用途

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Abbott

- ABIOMED

- Amiitalia

- Asahi Kasei

- BIOTRONIK

- Boston Scientific

- BPL Medical Technologies

- CU Medical

- Defibtech

- LivaNova

- Medico

- Medtronic

- MicroPort

- Nihon Kohden

- Osypka Medical

- Pacetronix

- Philips

- Schiller

- Stryker

- Vitatron

The Global Cardiac Rhythm Management Devices Market reached USD 23.5 billion in 2024 and is projected to expand at a CAGR of 5.2% between 2025 and 2034. The growth of this market is fueled by the rising incidence of cardiovascular diseases worldwide, including heart failure, arrhythmias, and other rhythm-related disorders. The steady increase in aging populations across major economies is also driving market expansion, as older individuals are more prone to cardiac complications. Factors such as sedentary lifestyles, poor dietary habits, and rising cases of hypertension, diabetes, and obesity are further intensifying the need for advanced cardiac care solutions.

With cardiovascular diseases remaining the leading cause of mortality worldwide, there is a growing demand for innovative and effective cardiac rhythm management devices that can improve patient outcomes and enhance quality of life. Additionally, constant advancements in medical technology, including remote monitoring and next-generation implantable devices, are transforming the way healthcare providers manage and treat cardiac rhythm disorders. The surge in healthcare expenditure, coupled with greater awareness about early diagnosis and preventive cardiac care, is expected to open up new opportunities for market players. The integration of artificial intelligence (AI) and machine learning (ML) into cardiac rhythm management systems is also anticipated to drive future market trends by enabling predictive analytics and personalized treatment options.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $23.5 Billion |

| Forecast Value | $39.7 Billion |

| CAGR | 5.2% |

The market comprises a wide range of product segments, including pacemakers, defibrillators, and cardiac resynchronization therapy (CRT) devices. Among these, defibrillators hold the largest market share, contributing significantly to the overall revenue. Defibrillators, especially implantable cardioverter defibrillators (ICDs), are vital for patients at high risk of life-threatening arrhythmias. These devices are designed to monitor heart rhythms continuously and deliver electric shocks when abnormal rhythms are detected, thereby preventing sudden cardiac death. The demand for defibrillators is expected to rise steadily as cardiovascular conditions continue to be a leading cause of morbidity and mortality globally.

In terms of application, the cardiac rhythm management devices market is segmented into congestive heart failure, arrhythmias, bradycardia, and tachycardia. Among these, congestive heart failure accounted for USD 8.6 billion in 2024. Devices like ICDs and CRT systems play a crucial role in managing heart failure by improving heart rhythm coordination, enhancing cardiac output, and alleviating symptoms such as fatigue and breathlessness, thereby improving patient quality of life.

The United States Cardiac Rhythm Management Devices Market generated USD 11.1 billion in 2024, dominating the global landscape. The country's advanced healthcare infrastructure, coupled with favorable reimbursement frameworks and broad access to state-of-the-art treatment options, continues to propel market growth. Strong clinical research, ongoing product innovations, and significant investments in R&D are enabling the rapid adoption of CRM devices in the U.S., solidifying its position as a global leader in this space.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing prevalence of heart failure and other cardiac disorders

- 3.2.1.2 Technological advancements and introduction of innovative devices for cardiac rhythm monitoring

- 3.2.1.3 Increasing public awareness

- 3.2.1.4 Rising sedentary lifestyle

- 3.2.1.5 Favorable reimbursement scenario

- 3.2.1.6 Growing geriatric population base coupled with rising prevalence of obesity

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of devices

- 3.2.2.2 Product recalls

- 3.2.2.3 Stringent regulatory approvals

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Reimbursement scenario

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Pricing analysis, 2024

- 3.9 Pipeline products

- 3.10 Indication landscape

- 3.11 Number of units, 2021 - 2034

- 3.11.1 Pacemaker

- 3.11.2 Defibrillators

- 3.11.3 CRT devices

- 3.12 Porter's analysis

- 3.13 GAP analysis

- 3.14 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Company market share analysis

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Pacemakers

- 5.2.1 Implantable pacemakers

- 5.2.2 External pacemakers

- 5.3 Defibrillators

- 5.3.1 Implantable cardioverter defibrillator (ICDs)

- 5.3.1.1 Transvenous implantable cardioverter defibrillator

- 5.3.1.2 Subcutaneous implantable cardioverter defibrillator

- 5.3.1.2.1 Single-chamber ICDs

- 5.3.1.2.2 Dual-chamber ICDs

- 5.3.2 External defibrillator

- 5.3.2.1 Manual external defibrillator

- 5.3.2.2 Automated external defibrillator

- 5.3.2.2.1 Semi-automated external defibrillator

- 5.3.2.2.2 Fully automated external defibrillator

- 5.3.2.3 Wearable cardioverter defibrillator

- 5.3.1 Implantable cardioverter defibrillator (ICDs)

- 5.4 Cardiac resynchronization therapy devices

- 5.4.1 Cardiac resynchronization therapy devices- D

- 5.4.2 Cardiac resynchronization therapy devices- P

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Congestive heart failure

- 6.3 Arrhythmias

- 6.4 Bradycardia

- 6.5 Tachycardia

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Cardiac care centers

- 7.4 Ambulatory surgical centers

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott

- 9.2 ABIOMED

- 9.3 Amiitalia

- 9.4 Asahi Kasei

- 9.5 BIOTRONIK

- 9.6 Boston Scientific

- 9.7 BPL Medical Technologies

- 9.8 CU Medical

- 9.9 Defibtech

- 9.10 LivaNova

- 9.11 Medico

- 9.12 Medtronic

- 9.13 MicroPort

- 9.14 Nihon Kohden

- 9.15 Osypka Medical

- 9.16 Pacetronix

- 9.17 Philips

- 9.18 Schiller

- 9.19 Stryker

- 9.20 Vitatron