|

市場調査レポート

商品コード

1699289

眼外傷デバイス市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Ocular Trauma Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| 眼外傷デバイス市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月19日

発行: Global Market Insights Inc.

ページ情報: 英文 135 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

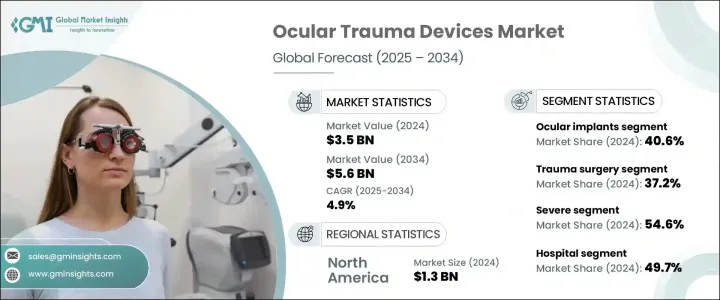

眼外傷デバイスの世界市場は、2024年に35億米ドルに達し、眼外傷の有病率の上昇と専門的治療ソリューションに対するニーズの高まりを背景に、2025年から2034年にかけてCAGR 4.9%で拡大すると予測されています。

眼外傷は依然として公衆衛生上の重大な関心事であり、軽微な擦り傷から重度の貫通外傷まで様々な事故が発生しており、早急な医療介入が必要です。早期診断の進歩、利用可能な治療オプションの認知度向上、最先端の手術技術の採用が市場拡大に拍車をかけています。ヘルスケアプロバイダーが眼外傷症例への迅速かつ効果的な介入を優先する中、高精度の外傷治療機器に対する需要は増加の一途をたどっています。

低侵襲手技と技術的に高度な装置は、患者の転帰を改善し、回復時間を短縮し、全体的な手術効率を高める上で重要な役割を果たしています。生体工学的眼インプラント、ロボット支援眼科手術、眼科用粘弾性装置(OVD)などの技術革新は牽引力を増しており、市場の好況にさらに貢献しています。さらに、政府のイニシアチブと世界のヘルスケア投資の増加が眼科研究開発の取り組みを強化し、より効果的な外傷管理ソリューションの導入につながっています。診断ツールや手術システムにおける人工知能の統合は、治療プロトコルをさらに合理化し、精度と効率の向上をもたらしています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 35億米ドル |

| 予測金額 | 56億米ドル |

| CAGR | 4.9% |

病院、専門クリニック、外来手術センターで眼外傷装置の導入が増加していることが、この上昇傾向を促進する上で極めて重要な役割を果たしています。世界的に外傷関連手術の件数が増加しているため、ヘルスケア施設は眼科機器のアップグレードを積極的に行っており、革新的なソリューションの採用が増加しています。

製品タイプ別に見ると、眼外傷装置市場は手術器具、眼内レンズ(IOL)、眼インプラント、眼粘弾性装置(OVD)、その他の関連機器に区分されます。眼インプラントは2024年に40.6%の市場シェアを占め、人工レンズや網膜プロテーゼなどの二次的ソリューションを必要とする重度外傷症例の増加に後押しされました。これらのインプラントは、事故、鈍的外傷、貫通外傷による構造的損傷後の視力回復と眼球の完全性維持に重要な役割を果たしています。複雑な眼外傷の増加により、重症例に効果的に対処できるよう設計された特殊なインプラントの需要が高まっています。

市場はまた、用途別に外傷手術、網膜剥離、白内障手術、緑内障管理、その他の処置に分類されます。外傷手術は2024年の市場シェア37.2%を占め、高度な外科的介入を必要とする鈍的外傷、貫通創傷、化学熱傷の発生率の上昇がその要因となっています。重度眼外傷の管理には、出血コントロール、構造修復、視機能回復が含まれるため、高精度の手術器具の使用が必要となります。高度な外傷管理ソリューションに対する需要の高まりが、市場の拡大を後押ししています。

米国は眼外傷治療器業界において依然として圧倒的な強さを誇っており、2024年の市場規模は12億3,000万米ドル、2032年には18億米ドルに達すると予想されています。医療技術の世界的リーダーである米国は、ロボット眼科手術、生体工学インプラント、低侵襲手術器具など、眼科技術革新の最前線にあります。官民両部門からの投資が画期的な研究を後押しし、メーカーが外傷性眼損傷治療のための次世代ソリューションを開発することを可能にしています。眼外傷治療の継続的な進歩により、市場は今後数年間で持続的な成長を遂げると思われます。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 眼外傷の増加

- 技術の進歩

- 意識の高まりと早期診断

- 有利な政府の取り組みと保険適用

- 業界の潜在的リスク&課題

- 高額な治療費

- 熟練したヘルスケア専門家の不足

- 促進要因

- 成長可能性分析

- 規制状況

- 償還シナリオ

- 今後の市場動向

- ギャップ分析

- 技術展望

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業シェア分析

- 競合ポジショニングマトリックス

- ベンダー・マトリックス分析

- 戦略ダッシュボード

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- 手術器具

- 眼内レンズ(IOLs)

- 眼インプラント

- 眼科用粘弾性デバイス(OVDs)

- その他の製品

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 外傷手術

- 網膜剥離

- 白内障手術

- 緑内障管理

- その他の用途

第7章 市場推計・予測:外傷重症度別、2021年~2034年

- 主要動向

- 軽度

- 中等度

- 重度

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 眼科クリニック

- 外来手術センター

- その他のエンドユース

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- フランス

- 英国

- イタリア

- スペイン

- アジア太平洋

- 日本

- 中国

- インド

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- アルゼンチン

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Alcon

- Bausch+Lomb

- Carl Zeiss Meditec

- CooperVision

- Essilor Instruments

- Haag-Streit Group

- Innovative Optics

- IRIDEX Corporation

- Johnson &Johnson Vision

- Leica Microsystems

- Optos

- Sonomed Escalon

- Topcon Corporation

The Global Ocular Trauma Devices Market reached USD 3.5 billion in 2024 and is projected to expand at a CAGR of 4.9% from 2025 to 2034, driven by the rising prevalence of eye injuries and the growing need for specialized treatment solutions. Ocular trauma remains a significant public health concern, with incidents ranging from minor abrasions to severe penetrating injuries that require immediate medical intervention. Advancements in early diagnosis, increased awareness of available treatment options, and the adoption of cutting-edge surgical techniques are fueling market expansion. As healthcare providers prioritize rapid and effective intervention for eye trauma cases, the demand for high-precision trauma devices continues to climb.

Minimally invasive procedures and technologically advanced devices are playing a crucial role in improving patient outcomes, reducing recovery time, and enhancing overall surgical efficiency. Innovations such as bioengineered ocular implants, robotic-assisted eye surgeries, and ophthalmic viscoelastic devices (OVDs) are gaining traction, further contributing to the market's positive trajectory. Moreover, government initiatives and increased healthcare investments worldwide are strengthening ophthalmic research and development efforts, leading to the introduction of more effective trauma management solutions. The integration of artificial intelligence in diagnostic tools and surgical systems is further streamlining treatment protocols, offering enhanced precision and efficiency.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.5 Billion |

| Forecast Value | $5.6 Billion |

| CAGR | 4.9% |

The increasing adoption of ocular trauma devices across hospitals, specialty clinics, and ambulatory surgical centers is playing a pivotal role in driving this upward trend. With a growing number of trauma-related surgeries performed globally, healthcare facilities are actively upgrading their ophthalmic equipment, leading to higher adoption of innovative solutions.

By product type, the ocular trauma devices market is segmented into surgical instruments, intraocular lenses (IOLs), ocular implants, ophthalmic viscoelastic devices (OVDs), and other related devices. Ocular implants captured a 40.6% market share in 2024, propelled by the rising number of severe trauma cases necessitating secondary solutions such as artificial lenses and retinal prostheses. These implants play a vital role in restoring vision and maintaining ocular integrity following structural damage caused by accidents, blunt force injuries, or penetrating trauma. The increasing prevalence of complex ocular injuries is fueling demand for specialized implants designed to address severe cases effectively.

The market is also categorized by application into trauma surgery, retinal detachment, cataract surgery, glaucoma management, and other procedures. Trauma surgery accounted for a 37.2% market share in 2024, driven by the rising incidence of blunt force trauma, penetrating wounds, and chemical burns requiring advanced surgical interventions. Managing severe ocular trauma involves hemorrhage control, structural repairs, and visual function restoration, necessitating the use of high-precision surgical tools. The growing demand for sophisticated trauma management solutions is reinforcing the market's expansion.

The United States remains a dominant force in the ocular trauma devices industry, with the market valued at USD 1.23 billion in 2024 and expected to generate USD 1.8 billion by 2032. As a global leader in medical technology, the country is at the forefront of ophthalmic innovations, including robotic eye surgeries, bioengineered implants, and minimally invasive surgical tools. Investments from both private and public sectors are fueling groundbreaking research, enabling manufacturers to develop next-generation solutions for treating traumatic eye injuries. With continuous advancements in ocular trauma care, the market is set to witness sustained growth in the coming years.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of ocular trauma

- 3.2.1.2 Technological advancements

- 3.2.1.3 Increasing awareness and early diagnosis

- 3.2.1.4 Favorable government initiatives and insurance coverage

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of treatment

- 3.2.2.2 Lack of skilled healthcare professionals

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Reimbursement scenario

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Technology landscape

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive positioning matrix

- 4.5 Vendor matrix analysis

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Surgical instruments

- 5.3 Intraocular lenses (IOLs)

- 5.4 Ocular implants

- 5.5 Ophthalmic viscoelastic devices (OVDs)

- 5.6 Other products

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Trauma surgery

- 6.3 Retinal detachment

- 6.4 Cataract surgery

- 6.5 Glaucoma management

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By Trauma Severity, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Mild

- 7.3 Moderate

- 7.4 Severe

Chapter 8 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Ophthalmic clinics

- 8.4 Ambulatory surgical centers

- 8.5 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 France

- 9.3.3 UK

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 Japan

- 9.4.2 China

- 9.4.3 India

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Argentina

- 9.5.3 Mexico

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Alcon

- 10.2 Bausch + Lomb

- 10.3 Carl Zeiss Meditec

- 10.4 CooperVision

- 10.5 Essilor Instruments

- 10.6 Haag-Streit Group

- 10.7 Innovative Optics

- 10.8 IRIDEX Corporation

- 10.9 Johnson & Johnson Vision

- 10.10 Leica Microsystems

- 10.11 Optos

- 10.12 Sonomed Escalon

- 10.13 Topcon Corporation