|

市場調査レポート

商品コード

1885919

耳鼻咽喉科用医療機器市場の機会、成長要因、業界動向分析、および2025年から2034年までの予測ENT Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 耳鼻咽喉科用医療機器市場の機会、成長要因、業界動向分析、および2025年から2034年までの予測 |

|

出版日: 2025年11月18日

発行: Global Market Insights Inc.

ページ情報: 英文 160 Pages

納期: 2~3営業日

|

概要

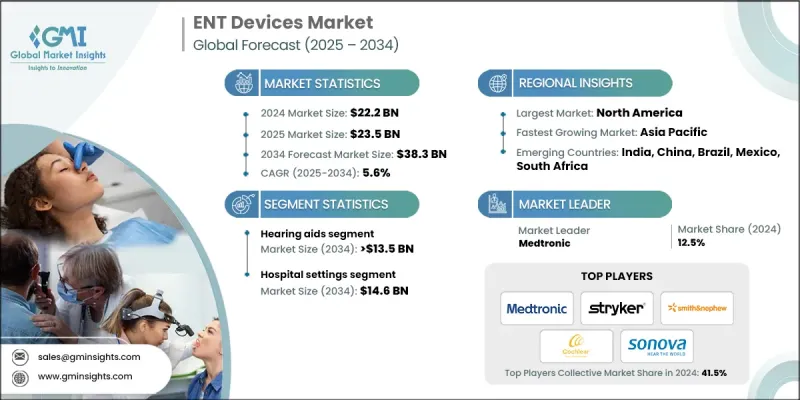

世界の耳鼻咽喉科用医療機器市場は、2024年に222億米ドルと評価され、2034年までにCAGR5.6%で成長し、383億米ドルに達すると予測されております。

成長の背景には、耳鼻咽喉科疾患の有病率上昇、高齢人口の拡大、低侵襲手術への需要増加が挙げられます。本市場は、医療提供者、ライフサイエンス企業、保険者、技術企業に対し、患者ケアの向上、規制順守、業務効率化を実現する革新的ソリューションを提供しています。主な製品には、内視鏡システム、聴覚インプラント、低侵襲手術器具、診断機器、および手術精度・疾患管理・生活の質全般の向上を目的としたデジタル耳鼻咽喉科プラットフォームが含まれます。世界の高齢化により、難聴、慢性副鼻腔炎、平衡障害の発生率が高まっており、耳鼻咽喉科領域での治療ニーズが増加しています。都市化と生活様式の変化も、呼吸器疾患やアレルギー疾患の発生率上昇につながり、患者層を拡大しています。回復期間の短縮、合併症リスクの低減、治療成果の向上から、臨床医と患者は低侵襲技術をますます好むようになり、専門的な耳鼻咽喉科機器の需要を牽引しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測期間 | 2025-2034 |

| 開始時価値 | 222億米ドル |

| 予測金額 | 383億米ドル |

| CAGR | 5.6% |

補聴器セグメントは2024年に37.5%のシェアを占めました。成長は、高齢者の聴覚障害の増加傾向と、デジタル補聴器やAI搭載補聴器などの技術進歩によって推進されています。このセグメントには、耳かけ型(BTE)、レシーバー・イン・イヤー/レシーバー・イン・キャナル(RITE/RIC)、完全耳道内/目に見えない耳道内(CIC/IIC)、耳内型(ITE)、耳道内型(ITC)の機器が含まれます。聴覚健康への意識の高まりと、先進的および従来型補聴器への需要が、病院、クリニック、在宅医療環境における導入を促進しております。

診断用耳鼻咽喉科機器セグメントは、2024年に58億米ドルの市場規模を記録し、2025年から2034年にかけてCAGR 6.2%で成長すると予測されています。このセグメントには、硬性内視鏡・軟性内視鏡、聴力スクリーニング装置、ロボット支援内視鏡が含まれます。耳鼻咽喉科疾患の早期発見と正確な診断に対する需要の高まりが、このセグメントの成長を促進しています。

北米の耳鼻咽喉科用医療機器市場は、2024年に38.6%のシェアを占めました。市場優位性は、確立された医療インフラ、先進医療技術の採用、高い医療支出によって支えられています。慢性副鼻腔炎、難聴、睡眠時無呼吸症候群などの耳鼻咽喉科疾患の症例増加が、高度な診断・治療機器の需要を後押ししています。高精細内視鏡、ロボット手術システム、AI搭載診断ツールなどの技術革新は、処置の精度と効率性を向上させ、病院、外来手術センター、診療所での導入を促進しています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 世界的に増加する耳鼻咽喉科疾患の有病率

- 高齢化人口の増加

- 耳鼻咽喉科機器における技術的進歩

- 低侵襲耳鼻咽喉科処置に対する需要の高まり

- 業界の潜在的リスク&課題

- 高い処置費および器具コスト

- 世界の社会的偏見

- 市場機会

- AI診断の統合

- 遠隔耳鼻咽喉科診療の増加

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ、中東・アフリカ地域

- 技術動向

- 現在の技術動向

- 低侵襲性耳鼻咽喉科手術器具および内視鏡システムの成長

- 遠隔耳鼻咽喉科診療および遠隔診断を可能とするデジタル耳鼻咽喉科プラットフォーム

- 患者様の利便性を考慮した聴覚インプラントおよび携帯型聴覚診断装置

- 新興技術

- AIを活用した耳鼻咽喉科診断および予測的疾患管理

- ウェアラブルかつ接続可能な聴覚・平衡機能デバイス

- 適応治療と個別化療法モードを備えたスマート耳鼻咽喉科デバイス

- 現在の技術動向

- ギャップ分析

- ポーター分析

- PESTEL分析

- 将来の市場動向

- AI統合型耳鼻咽喉科機器の拡大(疾患早期発見と個別化治療計画策定向け)

- 患者中心のケアを実現する遠隔耳鼻咽喉科プラットフォームおよび遠隔モニタリングソリューションの導入拡大

- 低侵襲・スマート・ウェアラブル耳鼻咽喉科機器の成長(処置効率と患者コンプライアンスの向上)

第4章 競合情勢

- イントロダクション

- 企業マトリクス分析

- 企業の市場シェア分析

- 世界

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ、中東・アフリカ

- 競合ポジショニングマトリックス

- 主要市場企業の競合分析

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 拡大計画

第5章 市場推計・予測:機器タイプ別、2021-2034

- 主要動向

- 補聴器

- 耳かけ型補聴器(BTE)

- 耳内型レシーバー/耳道内型レシーバー(RITE/RIC)

- 完全耳道内型/完全耳道内型(CIC/IIC)

- 耳内式(ITE)

- 耳道内(ITC)

- 診断用耳鼻咽喉科(ENT)機器

- 硬性内視鏡

- 喉頭鏡

- 鼻鏡

- 耳科用内視鏡

- 軟性内視鏡

- 聴力スクリーニング装置

- ロボット支援内視鏡

- 硬性内視鏡

- 外科用耳鼻咽喉科(ENT)機器

- 副鼻腔拡張装置

- 電動外科用器具

- 耳科用ドリルバー

- 高周波ハンドピース

- 耳鼻咽喉科用手動器具

- 鼓膜チューブ

- 鼻腔充填装置

- 聴覚インプラント

- 人工内耳

- 骨固定式補聴システム

- 聴覚脳幹インプラント

- 中耳インプラント

- 音声補綴装置

- 鼻用スプリント

- 外用鼻スプリント

- 内鼻スプリント

第6章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 病院

- 外来手術センター

- 耳鼻咽喉科クリニック

- 在宅医療

第7章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第8章 企業プロファイル

- Atos Medical

- Boston Scientific

- Cochlear

- DeSoutter Medical

- Johnson &Johnson(Ethicon)

- Lumenis

- Medtronic

- Meril Life Sciences

- Narang Medical

- Nouvag

- Olympus

- Smith &Nephew

- Sonova

- Stryker

- Vega Medical

- Welch Allyn(Hillrom)

- WestCMR

- Zimmer Biomet