|

|

市場調査レポート

商品コード

1455776

木質ペレットの世界市場-2024-2031年Global Wood Pellets Market - 2024-2031 |

||||||

|

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 木質ペレットの世界市場-2024-2031年 |

|

出版日: 2024年03月26日

発行: DataM Intelligence

ページ情報: 英文 185 Pages

納期: 即日から翌営業日

|

- 全表示

- 概要

- 目次

概要

世界の木質ペレット市場は2023年に95億米ドルに達し、2031年には157億米ドルに達すると予測され、予測期間2024-2031年のCAGRは6.4%で成長します。

世界の木質ペレット市場は、再生可能なエネルギー源と持続可能な実践に対する需要の増加により、著しく上昇しました。さまざまな木くずから製造される木質ペレットと圧縮バイオマス粒子は、熱と電力の生産において、従来の化石燃料に代わる競争力のある選択肢になりつつあります。

EUでは2022年に2,480万トンの木質ペレットが消費され、新記録を達成したが、その主な理由は国内利用の増加です。第3次再生可能エネルギー指令の施行と、加盟国の補助金による住宅市場の継続的な成長に基づき、EUの消費量は2023年には2,560万トンに達すると予想されます。

過去10年間、EUのペレット需要は国内供給をはるかに上回り、主に米国、ロシア、ベラルーシ、ウクライナからの輸入の増加につながった。2022年には、EUは5.89 MMT、13億2,000万米ドルの木質ペレットを輸入しました。したがって、欧州は世界市場シェアのほぼ1/3を占め、世界市場の成長に大きく貢献しています。

ダイナミクス

世界市場における輸出拡大

木質ペレットの製造量の増加に伴い、市場にはより多くの木質ペレットが供給されるようになった。供給量の増加は、国内および世界規模で高まる木質ペレットのニーズを満たすのに役立ちます。生産者は木質ペレットを輸出することで他の市場を開発し、消費者ベースを拡大することができます。特定の市場への依存を減らし、現地の需要の変動や規制の調整によるリスクを抑えることができます。生産者は、より幅広いマーケットプレースを発展させることで、売上と収益性を高めることができます。

例えば、米国農務省海外農業サービスによると、2023年12月に米国から輸出された木質ペレットの総量は917,175.4トンです。2022年通年では898万トンが輸出されました。米国の12月の木質ペレット輸出総額は1億5,295万米ドルで、2021年12月の1億107万米ドル、前月の1億2,094万米ドルから増加しました。

効率を高める新技術の発表

木質ペレットの生産は、新技術の使用により合理化され、生産性を高め、コストを下げることができます。その結果、より低いコストで生産量が増加し、市場が成長する可能性があります。技術の進歩により、持続可能な供給源から木質ペレットを生産したり、生産プロセスの持続可能性を高めたりすることが可能になります。

例えば、2022年4月、木質ペレット工場の規模拡大や生産性向上のため、自動化システム、ペレットミル、ペレット製造装置を提供するCPM社が新技術を導入しました。10年にわたる研究の末、同社は独自のツイントラック技術を開発し、エネルギー消費を節約し、安定したペレット品質を確保し、工場の生産能力を向上させました。

規制上の課題

木質ペレット事業には、排出、環境の持続可能性、森林管理技術に関する法律やガイドラインがいくつか適用されます。これらの規制を遵守することで、生産コストが増加したり、特定地域での市場参入が制限されたりする可能性があります。

例えば、炭素排出、森林伐採、持続可能な森林管理手法に関する規制は、木質ペレットを製造する企業にとって、原材料の入手に影響を与え、製造コストを上昇させる可能性があります。さらに、国や地域によって規制が異なるため、複数のマーケットプレースで事業を展開する企業にとっては問題が複雑になり、事業拡大の妨げになる可能性があります。

目次

第1章 調査手法と調査範囲

第2章 定義と概要

第3章 エグゼクティブサマリー

第4章 市場力学

- 影響要因

- 促進要因

- 世界市場における輸出拡大

- パレット効率向上のための新技術発表

- 抑制要因

- 規制の課題

- 機会

- 影響分析

- 促進要因

第5章 産業分析

- ポーターのファイブフォース分析

- サプライチェーン分析

- 価格分析

- 規制分析

- ロシア・ウクライナ戦争の影響分析

- DMIの見解

第6章 COVID-19分析

第7章 原料別

- 農業残渣

- リサイクル木材

- 森林残渣

- その他

第8章 用途別

- 暖房

- 発電

- 熱電併給(CHP)

第9章 エンドユーザー別

- 住宅

- 商業

- 工業

第10章 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- ロシア

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- その他南米

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- その他アジア太平洋地域

- 中東・アフリカ

第11章 競合情勢

- 競合シナリオ

- 市況/シェア分析

- M&A分析

第12章 企業プロファイル

- Enviva

- 会社概要

- 素材ポートフォリオと説明

- 財務概要

- 主な発展

- Fram Renewable Fuels

- German Pellets GmbH

- Wood Pellet Energy(UK)Ltd.

- Lignetics Inc.

- Energex Corporation

- Viridis Energy Inc.

- Zilkha Biomass Energy

- Drax Biomass

- Veer Biofuel

第13章 付録

Overview

Global Wood Pellets Market reached US$ 9.5 billion in 2023 and is expected to reach US$ 15.7 billion by 2031, growing with a CAGR of 6.4% during the forecast period 2024-2031.

The global wood pellet market had a significant upsurge due to the increasing demand for renewable energy sources and sustainable practice. Wood pellets and compressed biomass particles manufactured from a range of wood scraps are becoming a competitive alternative to traditional fossil fuels for the production of heat and power.

The EU consumed 24.8 Million Metric Tons of wood pellets in 2022, reaching a new record mostly because of rising domestic use. Based on the implementation of the third Renewable Energy Directive and the continued growth of the residential markets bolstered by Member State subsidies, it is anticipated that EU consumption will reach 25.6 MMT in 2023.

Over past ten years, the EU's demand for pellets has far exceeded local supply, leading to an increase in imports, primarily from US, Russia, Belarus and Ukraine. In 2022, the EU imported wood pellets valued at 5.89 MMT or US$ 1.32 billion. Therefore, the Europe is contributing significantly to the growth of the global market with capturing nearly 1/3rd of the global market share.

Dynamics

Export Expansion in the Global Market

There is more of a supply of wood pellets on the market as manufacturing increases. The augmented availability can aid in meeting the escalating need for wood pellets on a national and global scale. Producers can expand their consumer base by tapping into other markets by exporting wood pellets. The lessens reliance on a particular market and helps to limit the risks put on by variations in local demand or adjustments to regulations. Producers can increase sales and profitability by reaching out to a wider range of marketplaces.

For instance, As per USDA Foreign Agricultural Service, the total amount of wood pellets exported from U.S. in December 2023 was 917,175.4 metric Tons. For the entire year 2022, 8.98 million metric Tons were exported. US wood pellet exports totaled US$ 152.95 million in December, up from US$ 101.07 million in December 2021 and US$ 120.94 million the month before.

New Technology Launches to Enhance Pallet Efficiency

The production of wood pellets can be streamlined with the use of new technology, increasing productivity and lowering costs. Growth in the market may result from increased production volumes at lower costs as a result. Technological advancements can make it attainable to produce wood pellets from sustainable sources or increase the production process's sustainability.

For instance, in April 2022, to scale or increase the productivity of wood pellet mills, CPM, a provider of automation systems, pellet mills and pelleting equipment, has introduced new technology. After ten years of study, the company developed its proprietary Twin Track technology to save energy consumption, ensure consistent pellet quality and increase mill capacity.

Regulatory Challenges

Several laws and guidelines about emissions, environmental sustainability and forest management techniques apply to the wood pellet business. Adherence to these regulations may result in increased production expenses and limited market accessibility in specific areas.

For instance, rules about carbon emissions, deforestation and sustainable forestry methods may affect raw material availability and raise production costs for companies that make wood pellets. Moreover, regulatory variations among nations and areas can complicate matters for businesses that operate in several marketplaces, impeding their ability to expand.

Segment Analysis

The global wood pellets market is segmented based on feedstock, application, end-user and region.

Biomass Pellets Accelerate Adoption in Power Industry

In October 2021, an Indian power company NTPC had placed an order for 9,30,000 tons of biomass pellets to be co-fired in power plants, to enhance air quality. Moreover, the energy ministry states that 1.3 million tons of biomass pellets are sourced by UP, Punjab & Haryana for co-firing in their power plants.

The supply of 8,65,000 tons of biomass pellets, for which NTPC placed an order, is currently underway. In October 2021, NTPC placed a 65,000-ton additional order. Furthermore, above mentioned statement augments the demand for bio-based wood pellets in power industry. Therefore, the power generation application segment contributes significantly to the global segmental share.

Geographical Penetration

Increasing Product Launches of Hardwood Pellets Fuels Market Growth

The growing product launches of hardwood pellets contribute to the diversification of product offerings in the North American wood pellets market. By providing consumers with a wider range of options, including softwood and hardwood pellets, manufacturers can better cater to diverse customer preferences and applications, thereby stimulating market growth.

For instance, on April 22, 2021, Kingsford has launched Pellets made entirely of hardwood. Kingsford has begun selling Hardwood Pellets in addition to charcoal as premium wood-fired fuel. To provide greater hickory, cherry and maple wood flavor, Kingsford pellets are composed entirely of natural materials with no additions of binders, preservatives or fillers. Therefore, with more than 25% of the global market share, North America is contributing significant in global market.

COVID-19 Impact Analysis

Due to travel restrictions, plant closures and lockdown precautions, the pandemic caused disruptions in supply networks. Due to the disruption in the supply of equipment, additives and raw materials required for the production of wood pellets, manufacturing and project timeframes were delayed. The pandemic has affected the energy industry, specifically the power generation sector.

The pandemic's effects on consumer behavior and economic slowdowns resulted in a decline in the market demand for wood pellets, especially in areas like commercial and domestic heating. The overall usage of wood pellets decreased as a result of people spending more time at home and less time in workplaces and commercial buildings requiring heating fuel.

Russia-Ukraine War Impact Analysis

The scarcity of wood pellets in Europe may cause prices to soar in the event of supply chain interruptions. Customers who rely on wood pellets for energy generation, such as consumers who use them for domestic heating, commercial enterprises and industrial facilities, will be impacted by these price increases.

Being a significant exporter of energy resources, disruptions in the energy supply spurred on by the fighting may result in increased energy prices globally. As a result, producers of wood pellets might have to pay more for production and transportation, which they could then pass along to consumers in the form of higher product prices.

By Feedstock

- Agricultural Residues

- Recycled Wood

- Forest Residues

- Others

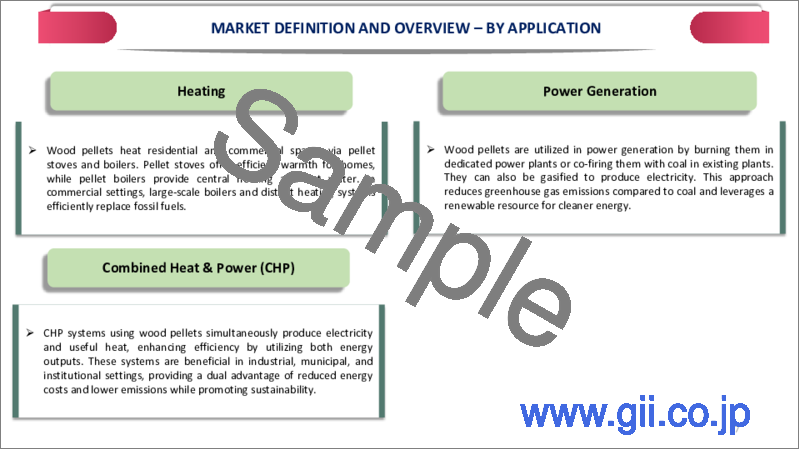

By Application

- Heating

- Power Generation

- Combined Heat & Power (CHP)

By End-User

- Residential

- Commercial

- Industrial

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Russia

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Asia-Pacific

- China

- India

- Japan

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

Key Developments

- On April 22, 2021, Kingsford has launched Pellets made entirely of hardwood. Kingsford has begun selling Hardwood Pellets in addition to charcoal as premium wood-fired fuel.

- In 2020, OkoFEN Forschungs- und Entwicklungs Ges.m.b.H has announced ZeroFlame combustion technology, which minimizes particulate matter (PM) emissions without the need for filters. The company perceives this as another significant advancement in the field of wood pellet heating.

- In 2020, Pure Biofuel has introduced its newest bag and updated product range to our customers and partners in UK, ENPOWER wood pellets. The pellets represent the foundation of our operation and reflect our basic company values of dependability, quality and value.

Competitive Landscape

The major global players in the market include Enviva, Fram Renewable Fuels, German Pellets GmbH, Wood Pellet Energy (UK) Ltd., Lignetics Inc., Energex Corporation, Viridis Energy Inc., Zilkha Biomass Energy, Drax Biomass and Veer Biofuel.

Why Purchase the Report?

- To visualize the global wood pellets market segmentation based on feedstock, application, end-user and region, as well as understands key commercial assets and players.

- Identify commercial opportunities by analyzing trends and co-development.

- Excel data sheet with numerous data points of wood pellets market-level with all segments.

- PDF report consists of a comprehensive analysis after exhaustive qualitative interviews and an in-depth study.

- Product mapping available as excel consisting of key products of all the major players.

The global wood pellets market report would provide approximately 61 tables, 53 figures and 185 Pages.

Target Audience 2024

- Manufacturers/ Buyers

- Industry Investors/Investment Bankers

- Research Professionals

- Emerging Companies

Table of Contents

Table of Contents

1.Methodology and Scope

- 1.1.Research Methodology

- 1.2.Research Objective and Scope of the Report

2.Definition and Overview

3.Executive Summary

- 3.1.Snippet by Feedstock

- 3.2.Snippet by Application

- 3.3.Snippet by End-User

- 3.4.Snippet by Region

4.Dynamics

- 4.1.Impacting Factors

- 4.1.1.Drivers

- 4.1.1.1.Export Expansion in the Global Market

- 4.1.1.2.New Technology Launches to Enhance Pallet Efficiency

- 4.1.2.Restraints

- 4.1.2.1.Regulatory Challenges

- 4.1.3.Opportunity

- 4.1.4.Impact Analysis

- 4.1.1.Drivers

5.Industry Analysis

- 5.1.Porter's Five Force Analysis

- 5.2.Supply Chain Analysis

- 5.3.Pricing Analysis

- 5.4.Regulatory Analysis

- 5.5.Russia-Ukraine War Impact Analysis

- 5.6.DMI Opinion

6.COVID-19 Analysis

- 6.1.Analysis of COVID-19

- 6.1.1.Scenario Before COVID

- 6.1.2.Scenario During COVID

- 6.1.3.Scenario Post COVID

- 6.2.Pricing Dynamics Amid COVID-19

- 6.3.Demand-Supply Spectrum

- 6.4.Government Initiatives Related to the Market During Pandemic

- 6.5.Manufacturers Strategic Initiatives

- 6.6.Conclusion

7.By Feedstock

- 7.1.Introduction

- 7.1.1.Market Size Analysis and Y-o-Y Growth Analysis (%), By Feedstock

- 7.1.2.Market Attractiveness Index, By Feedstock

- 7.2.Agricultural Residues*

- 7.2.1.Introduction

- 7.2.2.Market Size Analysis and Y-o-Y Growth Analysis (%)

- 7.3.Recycled Wood

- 7.4.Forest Residues

- 7.5.Others

8.Application

- 8.1.Introduction

- 8.1.1.Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

- 8.1.2.Market Attractiveness Index, By Application

- 8.2.Heating*

- 8.2.1.Introduction

- 8.2.2.Market Size Analysis and Y-o-Y Growth Analysis (%)

- 8.3.Power Generation

- 8.4.Combined Heat & Power (CHP)

9.End-User

- 9.1.Introduction

- 9.1.1.Market Size Analysis and Y-o-Y Growth Analysis (%), By End-User

- 9.1.2.Market Attractiveness Index, By End-User

- 9.2.Residential*

- 9.2.1.Introduction

- 9.2.2.Market Size Analysis and Y-o-Y Growth Analysis (%)

- 9.3.Commercial

- 9.4.Industrial

10.By Region

- 10.1.Introduction

- 10.1.1.Market Size Analysis and Y-o-Y Growth Analysis (%), By Region

- 10.1.2.Market Attractiveness Index, By Region

- 10.2.North America

- 10.2.1.Introduction

- 10.2.2.Key Region-Specific Dynamics

- 10.2.3.Market Size Analysis and Y-o-Y Growth Analysis (%), By Feedstock

- 10.2.4.Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

- 10.2.5.Market Size Analysis and Y-o-Y Growth Analysis (%), By End-User

- 10.2.6.Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

- 10.2.6.1.U.S.

- 10.2.6.2.Canada

- 10.2.6.3.Mexico

- 10.3.Europe

- 10.3.1.Introduction

- 10.3.2.Key Region-Specific Dynamics

- 10.3.3.Market Size Analysis and Y-o-Y Growth Analysis (%), By Feedstock

- 10.3.4.Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

- 10.3.5.Market Size Analysis and Y-o-Y Growth Analysis (%), By End-User

- 10.3.6.Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

- 10.3.6.1.Germany

- 10.3.6.2.UK

- 10.3.6.3.France

- 10.3.6.4.Italy

- 10.3.6.5.Russia

- 10.3.6.6.Rest of Europe

- 10.4.South America

- 10.4.1.Introduction

- 10.4.2.Key Region-Specific Dynamics

- 10.4.3.Market Size Analysis and Y-o-Y Growth Analysis (%), By Feedstock

- 10.4.4.Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

- 10.4.5.Market Size Analysis and Y-o-Y Growth Analysis (%), By End-User

- 10.4.6.

- 10.4.7.Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

- 10.4.7.1.Brazil

- 10.4.7.2.Argentina

- 10.4.7.3.Rest of South America

- 10.5.Asia-Pacific

- 10.5.1.Introduction

- 10.5.2.Key Region-Specific Dynamics

- 10.5.3.Market Size Analysis and Y-o-Y Growth Analysis (%), By Feedstock

- 10.5.4.Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

- 10.5.5.Market Size Analysis and Y-o-Y Growth Analysis (%), By End-User

- 10.5.6.Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

- 10.5.6.1.China

- 10.5.6.2.India

- 10.5.6.3.Japan

- 10.5.6.4.Australia

- 10.5.6.5.Rest of Asia-Pacific

- 10.6.Middle East and Africa

- 10.6.1.Introduction

- 10.6.2.Key Region-Specific Dynamics

- 10.6.3.Market Size Analysis and Y-o-Y Growth Analysis (%), By Feedstock

- 10.6.4.Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

- 10.6.5.Market Size Analysis and Y-o-Y Growth Analysis (%), By End-User

11.Competitive Landscape

- 11.1.Competitive Scenario

- 11.2.Market Positioning/Share Analysis

- 11.3.Mergers and Acquisitions Analysis

12.Company Profiles

- 12.1.Enviva*

- 12.1.1.Company Overview

- 12.1.2.Material Portfolio and Description

- 12.1.3.Financial Overview

- 12.1.4.Key Developments

- 12.2.Fram Renewable Fuels

- 12.3.German Pellets GmbH

- 12.4.Wood Pellet Energy (UK) Ltd.

- 12.5.Lignetics Inc.

- 12.6.Energex Corporation

- 12.7.Viridis Energy Inc.

- 12.8.Zilkha Biomass Energy

- 12.9.Drax Biomass

- 12.10.Veer Biofuel

LIST NOT EXHAUSTIVE

13.Appendix

- 13.1. About Us and Services

- 13.2.Contact Us