|

市場調査レポート

商品コード

1690132

木質ペレット:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Wood Pellet - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 木質ペレット:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 142 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

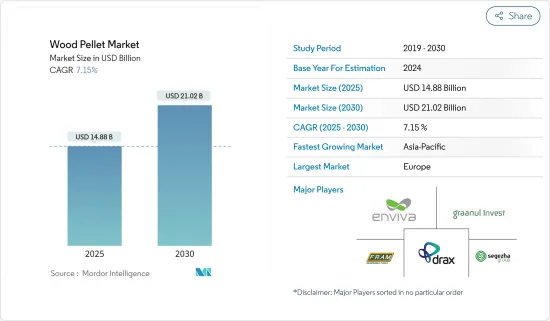

木質ペレットの市場規模は2025年に148億8,000万米ドルと推定され、予測期間中(2025-2030年)のCAGRは7.15%で、2030年には210億2,000万米ドルに達すると予測されます。

中期的な市場促進要因としては、特に欧州地域におけるクリーンエネルギー発電における木質ペレット需要の増加が挙げられます。

一方、世界各地における太陽光発電、風力発電、地熱発電などの代替再生可能エネルギーの採用や導入の増加は、予測期間中の市場成長を妨げる可能性が高いです。

とはいえ、世界バイオエネルギー協会によれば、木質ペレットは発電施設において石炭に取って代わる可能性を秘めています。最近の技術開発により、木質ペレットは、熱分解、水熱炭化、水蒸気爆発などの様々なプロセスを通じて熱改良されています。熱改良により、木質ペレットは石炭の性質を持つ燃料として機能するようになります。石炭発電所の数が世界で最も多いアジア太平洋地域は、今後市場が成長する機会になると予想されます。

2022年中に木質ペレットの生産量が大幅に増加した欧州は、予測期間中に市場で大きなシェアを占めると予想されます。

木質ペレット市場動向

暖房用途が市場を独占する見込み

- ペレットは固形バイオマス燃料であり、主に木材残渣やわらのような農業製品別から生産されます。未加工のバイオマスと比較した場合のペレット特有の利点としては、標準化された特性、高いエネルギー含有量、高い密度が挙げられます。

- 暖房用途の木質ペレットは、主に住宅や商業部門で、食品、調理、グリル、家庭への熱供給に使用されています。ショットコストが他の燃料より安い状態が長く続いたため、より経済的な選択肢となり、住宅および商業部門の主要な懸念に対処しています。

- 木質ペレットは、燃やすと高密度化したバイオマス燃料で、電力や熱を生み出すことができます。木質ペレットの生産、消費、商業は、2000年代後半にいくつかの国で著しく増加しました。通常、木質ペレットは石炭と混焼されるか、石炭に置き換わる産業用発電所が消費拡大の原因です。

- ドイツ・エネルギー木材・ペレット協会によると、2022年のドイツ国内のペレット暖房システムは64万8,000台で、2021年の57万台に比べ増加しています。

- さらに、再生可能エネルギー源として、木質ペレットは多くの国で政府から補助金や奨励金を受けており、近年多くの国が暖房用途の木質ペレットに関連する政策や制度を立ち上げたり更新したりしています。

- 英国政府は、2022年11月23日に施行されたペレット専用の燃料品質停止措置を最長1年間実施しました。つまり、停止措置が有効な間は、バイオマスボイラーや、所有者がOFGEMから再生可能熱奨励金の支払いを受ける工場で使用される木質ペレットの燃料品質基準は要求されないです。政府は2022年2月に規制を改正し、バイオマスサプライヤーリスト(BSL)番号を持つ木質燃料は、関連する品質基準も満たすことを義務付けた。

- したがって、上記の点から、予測期間中は暖房用途が木質ペレットを支配すると予想されます。

市場を独占する欧州

- 欧州の木質ペレット需要は、2022年から2028年にかけて30~40%増加すると予想されます。欧州は世界のペレット需要の50%以上を占めています。さらに、ペレットは学校やオフィスなどの地方自治体や行政機関の建物における石炭転換プロジェクトにも進出しています。

- 米国農務省対外農業サービス報告書によると、2022年、EUのペレット消費量は前年比1.2%増の2,480万トンに達しました。欧州のペレット消費量の約66%は家庭・商業部門が、34%は産業部門が消費しています。状況は国によって異なります。オランダとデンマークの主な原動力は産業用(電力とCHP用)です。イタリア、ドイツ、フランスでは、住宅暖房が木質ペレット使用の大半を占めています。

- この地域のほとんどの国は、混焼発電所の閉鎖や転換を計画しており、いくつかの国は燃料を100%木質ペレットに移行しています。例えば、Valmetは2023年5月、フィンランドのヘルシンキにあるSalmisaari'A'発電所で、Helen社の石炭焚き地域熱ボイラーと気泡流動床(BFB)燃焼を木質ペレット焚きに転換すると発表しました。この転換は、脱石炭という同社の目標を推進すると同時に、持続可能なエネルギーシステムの構築を強化するものです。

- 一方、EUは2022年7月、ウクライナ戦争を受け、発電に使用されるロシアの木質バイオマスの輸入を禁止しました。報道によると、EUはロシア産木質バイオマスの供給に代わる木質ペレットを米国や東欧から輸入しています。エンビバ社は、戦争が始まって以来、EUへの出荷量を増やし、2027年までに年間80万トンのペレットを供給するという、無名の欧州顧客との10年契約を発表しました。

- さらに、この地域の市場における技術の進歩も、調査期間中に木質ペレットの需要を増加させる可能性が高いです。

- したがって、上記の点から、予測期間中、欧州が市場を独占すると予想されます。

木質ペレット産業の概要

木質ペレット市場は適度に統合されています。市場の主要企業としては、Enviva Partners LP、AS Graanul Invest、Drax Group Plc、Fram Renewable Fuels LLC、Segezha Group JSCなどが挙げられる(順不同)。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模および需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と政策

- 市場力学

- 促進要因

- クリーンエネルギー生成における木質ペレット需要の増加

- 木質ペレット製造インフラの成長

- 抑制要因

- 代替再生可能エネルギーの採用と導入の増加

- 促進要因

- サプライチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 用途

- 暖房

- 発電

- 地域

- 北米

- 米国

- カナダ

- その他北米地域

- 欧州

- フランス

- イタリア

- ドイツ

- 英国

- スペイン

- 北欧諸国

- トルコ

- ロシア

- その他欧州

- アジア太平洋

- 中国

- インド

- インドネシア

- 日本

- 韓国

- マレーシア

- タイ

- ベトナム

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- ナイジェリア

- カタール

- エジプト

- その他中東とアフリカ

- 北米

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Enviva Partners LP

- AS Graanul Invest

- Drax Group PLC

- Fram Renewable Fuels LLC

- Segezha Group JSC

- Lignetics Inc.

- Biopower Sustainable Energy Corp.

- Asia Biomass Public Company Limited

- PT South Pacific

- Market Ranking/Share Analysis

第7章 市場機会と今後の動向

- 技術開発による木質ペレットの温度上昇

The Wood Pellet Market size is estimated at USD 14.88 billion in 2025, and is expected to reach USD 21.02 billion by 2030, at a CAGR of 7.15% during the forecast period (2025-2030).

Over the medium period, the primary drivers for the market include increasing demand for wood pellets in clean energy generation, especially in the European region.

On the other hand, the adoption and increasing deployment of alternative renewable energy sources such as solar photovoltaic, wind energy, and geothermal in various parts of the world is likely to hinder market growth during the forecast period.

Nevertheless, as per the World Bioenergy Association, wood pellets have the potential to replace coal in power generation facilities. With technology development in recent years, wood pellets have undergone thermal upgrading through various processes like torrefaction, hydrothermal carbonization, and steam explosion. The thermal upgrading enables wood pellets to act as a fuel with coal properties. The Asia-Pacific region, with the world's highest number of coal power plants, is expected to be an opportunity for the market to grow in the future.

With a significant production of wood pellets during 2022, Europe was expected to have a significant share of the market during the forecast period.

Wood Pellet Market Trends

Heating Application Expected to Dominate the Market

- Pellets are a solid biomass fuel, primarily produced from wood residues and agricultural by-products like straw. Specific advantages of pellets as compared to unprocessed biomass include standardized properties, high energy content, and high density.

- Wood pellets for heating applications are primarily used in residential and commercial sectors for food, cooking and grilling, and supplying heat to homes. Since the cost of shots remained cheaper than other fuels for a long time, it has become a more economical option, addressing the primary concern of the residential and commercial sectors.

- When burned, utility wood pellets (wood pellets) are a densified biomass fuel that can create power or heat. Wood pellet production, consumption, and commerce significantly increased in a few nations during the late 2000s. Industrial power plants, where wood pellets are usually co-fired with or replaced by coal, are the source of consumption growth.

- According to the German Energy Wood and Pellet Association, in 2022, there were 648 thousand pellet heating systems in Germany, an increase compared to 570 thousand in 2021.

- Moreover, as a renewable energy source, wood pellets have received subsidies and incentives from governments in many countries, and many countries either launched or updated their policies and schemes related to wood pellets for heating applications in recent years.

- The UK government has implemented a suspension of fuel quality for pellets exclusively, which went into effect on November 23, 2022, for up to one year. This means that while the rest is in effect, the fuel quality criteria for wood pellets used in biomass boilers and plants where the owner receives Renewable Heat Incentive payments from OFGEM are not required. The government revised regulations in February 2022 to require that any wood fuel having a Biomass Suppliers List (BSL) number also meet the relevant quality criteria.

- Therefore, owing to the above points, the heating application is expected to dominate the wood pellet during the forecast period.

Europe to Dominate the Market

- Europe's demand for wood pellets is expected to increase by 30-40% between 2022 and 2028. Europe represents more than 50% of global pellet demand. Moreover, pellets have also made their way into coal conversion projects in local authority or public administration buildings such as schools and offices.

- According to the USDA Foreign Agricultural Service Report, in 2022, the EU's pellet consumption reached 24.8 million tonnes, up 1.2% from the previous year. The household and commercial sectors consumed around 66% of European pellets, while the industry consumed 34%. The situation varies from one country to the next. The main driver for the Netherlands and Denmark is industrial use (for electricity and CHP). Residential heating accounts for most wood pellet use in Italy, Germany, and France.

- Most countries in the region plan to close or convert co-firing power stations, with several moving to 100% wood pellets for fuel. For instance, in May 2023, Valmet announced the convert Helen Ltd's coal-fired district heat boiler and bubbling fluidized bed (BFB) combustion to enable wood pellet firing at the Salmisaari 'A' power plant in Helsinki, Finland. The conversion promotes the company's goal of phasing out coal and simultaneously strengthens the construction of a sustainable energy system.

- On the other hand, in July 2022, the European Union banned importing Russian woody biomass used to generate energy in response to the war in Ukraine. According to reports, the EU has imported wood pellets from the United States and Eastern Europe to replace the Russian woody biomass supply. Enviva has increased EU shipments since the war began and announced a 10-year contract with an unnamed European customer to provide 800,000 metric tons of pellets yearly by 2027.

- Further, technological advancements in the market in the region are also likely to increase the demand for wood pellets during the studied period.

- Hence, owing to the above points, Europe is expected to dominate the market during the forecast period.

Wood Pellet Industry Overview

The wood pellet market is moderately consolidated. Some of the key players in the market include (in no particular order) Enviva Partners LP, AS Graanul Invest, Drax Group Plc, Fram Renewable Fuels LLC, and Segezha Group JSC, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecasts in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Demand for Wood Pellets in Clean Energy Generation

- 4.5.1.2 Growing Wood Pellet Manufacturing Infrastructure

- 4.5.2 Restraints

- 4.5.2.1 The Adoption and Increasing Deployment of Alternative Renewable Energy

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 Heating

- 5.1.2 Power Generation

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States of America

- 5.2.1.2 Canada

- 5.2.1.3 Rest of the North America

- 5.2.2 Europe

- 5.2.2.1 France

- 5.2.2.2 Italy

- 5.2.2.3 Germany

- 5.2.2.4 United Kingdom

- 5.2.2.5 Spain

- 5.2.2.6 Nordic Countries

- 5.2.2.7 Turkey

- 5.2.2.8 Russia

- 5.2.2.9 Rest of the Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Indonesia

- 5.2.3.4 Japan

- 5.2.3.5 South Korea

- 5.2.3.6 Malaysia

- 5.2.3.7 Thailand

- 5.2.3.8 Vietnam

- 5.2.3.9 Rest of the Asia-Pacific

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Colombia

- 5.2.4.4 Rest of the South America

- 5.2.5 Middle-East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 United Arab Emirates

- 5.2.5.3 South Africa

- 5.2.5.4 Nigeria

- 5.2.5.5 Qatar

- 5.2.5.6 Egypt

- 5.2.5.7 Rest of the Middle-East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Enviva Partners LP

- 6.3.2 AS Graanul Invest

- 6.3.3 Drax Group PLC

- 6.3.4 Fram Renewable Fuels LLC

- 6.3.5 Segezha Group JSC

- 6.3.6 Lignetics Inc.

- 6.3.7 Biopower Sustainable Energy Corp.

- 6.3.8 Asia Biomass Public Company Limited

- 6.3.9 PT South Pacific

- 6.4 Market Ranking/Share Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Thermal Upgradation of Wood Pellets Due to Technological Development