|

市場調査レポート

商品コード

1683533

欧州の木質ペレット-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Europe Wood Pellet - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の木質ペレット-市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

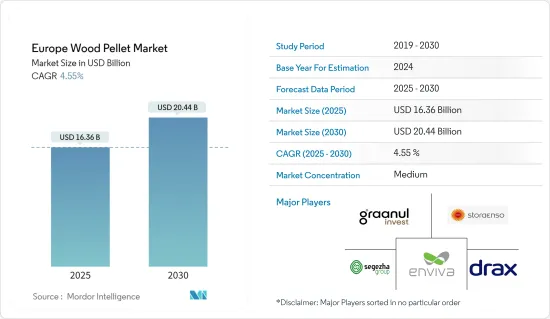

欧州の木質ペレット市場規模は、2025年に163億6,000万米ドルと推定され、予測期間(2025年~2030年)のCAGRは4.55%で、2030年には204億4,000万米ドルに達すると予測されます。

主なハイライト

- 中期的には、クリーンエネルギー発電と熱供給用途での木質ペレット需要の増加が、欧州の木質ペレット市場を牽引すると思われます。

- 一方、代替クリーンエネルギーとの競合の激化や、木質ペレットに対する政府の支援制度の終了が、予測期間中の市場成長の妨げになる可能性が高いです。

- とはいえ、新たな用途の出現と木質ペレット技術の進歩が、将来の市場成長を後押しすると予想されます。

- 様々な用途への木質ペレットの採用が増加していることから、英国が欧州の木質ペレット市場を独占すると予想されます。

欧州木質ペレット市場動向

暖房用途セグメントが市場を独占する見込み

- 暖房用途の木質ペレットは、主に住宅や商業分野で食品、調理、グリル、住宅への熱供給に使用されます。これらの木質ペレットは、接続されたパイプ、ボイラー、暖房用ラジエーターとともに、家庭で暖房システムを構築するために使用されます。暖房用としては、ペレット中央暖房ボイラー、ペレットストーブ、ペレット中央暖房ストーブなどがあります。

- 欧州の木質ペレット市場の暖房用途セグメントは、特にドイツとフランスで木質ペレットの消費が増加しているため、大きな需要を生み出すと期待されています。欧州は世界最大の木質ペレット市場です。2022年、この地域の総木材パレット消費量は2,480万トン(MMT)を占めました。欧州委員会(EC)の指令とEU加盟国(MS)の奨励策によると、2023年の需要は2,560万トンにさらに拡大すると予想されます。

- 住宅暖房用の木質ペレット需要の増加が、今後の市場の成長を促進すると予想されます。住宅用には、家庭用ストーブや容量50kW未満の暖房専用ボイラーが含まれます。容量が50kWを超える中小規模の業務用には、住宅や公共施設で使用される熱ボイラーが含まれます。

- 木質ペレットは、バイオマスボイラーや専用のペレット燃焼ストーブで家庭用暖房燃料として使用できます。ペレットストーブは、従来の薪ストーブよりも煙や煤が少なく、きれいに燃焼するので優れています。木質ペレットは密度が高く、含水率が低い(10%以下)ので、ストーブの中で非常に高い燃焼温度で燃焼でき、効率も向上し、灰分も従来の薪よりはるかに少ない(2%以下)。

- 暖房に木質ペレットを使うことは、電気代を削減する代替方法です。欧州の消費者は、燃料費の高騰に伴い、代替の暖房方法を探しています。

- ストーブ産業連盟によると、薪は家庭用暖房燃料の中で最も安く、1kWhあたりのコストは電気暖房より74%、ガス暖房より21%安いです。このような木質ペレットの利点により、予測期間中に暖房用途での需要が増加すると予想されます。

- ドイツ、イタリア、フランス、デンマーク、スウェーデンは、暖房目的で木質ペレットを使用する主要国です。EPC調査2023によると、2022年に暖房用に木質ペレットを最も多く使用したのはドイツで、320万トンを占めました。

- ドイツとイタリアでは、木質ペレットによる熱生成の70%以上が住宅暖房に使用され、デンマークとスウェーデンでは、ペレットは主にCHP熱に使用されました。気候は木質ペレットの消費に重要な役割を果たしています。欧州諸国の気候は将来的に寒冷化することが予想されるため、予測期間中に暖房目的でのペレット利用が増加することが予想されます。

- そのため、予測期間中は暖房用途セグメントが市場を独占すると予想されます。

英国が市場を独占する見込み

- 英国では、住宅暖房、発電所、商業暖房、熱電併給プラントなど、数多くの用途でペレットが使用されています。ペレットはまた、学校やオフィスなどの地方自治体の建物や行政機関の建物における石炭転換プロジェクトにも進出しています。

- 2024年現在、混焼発電所の大半は閉鎖または転換し、いくつかの発電所は燃料に木質ペレットを100%使用する方向にシフトしています。その中で最大のものは、ノース・ヨークシャーにあるドラックス発電所です。65MWeの発電ユニット6基のうち4基を木質ペレットのみに転換しました。

- ドラックス発電所は国内最大の発電所で、2023年には英国全体の約5%の電力を生産します。また、世界最大のバイオマス焚き火力発電所でもあり、毎年約650万トン(MT)のペレットを受け入れ、同国の年間ペレット輸入量の大部分を占めています。同社は米国とカナダにも17のペレット工場を持ち、発電所に原料を供給しています。

- しかし、英国政府によると、同国が2023年に輸入した木質ペレットは600万トンで、2022年には752万トン、2021年には913万トンでした。

- 国連食糧農業機関によると、2022年の同国の木質ペレット生産量は約32万6,000トンでした。木質ペレットの生産量は前年比約7.2%の大幅な伸びを示しました。

- 英国政府は2035年までに炭素回収・利用・貯留(CCUS)の競争市場を開拓する計画を打ち出し、2023年12月に炭素回収・貯留を伴うバイオエネルギー(BECCS)を支援するCfDプログラムを拡大する計画を発表しました。この計画は、2050年までに英国経済を年間50億ユーロ押し上げ、同国をこの技術のパイオニアにすることが期待されています。

- ドラックス社は、その運営資金として年間数億ポンドの補助金を受け取っています。2027年、英国政府は未燃焼バイオマス発電への支援を打ち切る予定です。

- 2027年以降に補助金が打ち切られるのを防ぐため、ドラックス社は木材燃焼事業に対する新たな長期補助金の確保を目指しています。同社は、計画中のBECCS(Bioenergy with Carbon Capture)プロジェクトを通じてこれを達成することを目指しています。このプロジェクトは当初、既存の発電能力の半分に炭素回収貯留(CCS)を追加することを提案しており、同社は年間8トンのマイナス排出を生み出すとしています。目標は、全発電容量にCCSを追加することです。

- 2024年1月、CfDプログラムの延長に伴い、英国政府はドラックス発電所への炭素回収技術の導入計画を承認しました。同発電所では、木質ペレットを燃やして発電する4基のバイオマスユニットのうち、2基への導入が許可されます。

- したがって、こうした開発により、予測期間中、英国が欧州の木質ペレット市場を独占すると予想されます。

欧州木質ペレット産業概要

欧州の木質ペレット市場は半固体化しています。市場の主要企業には、Stora Enso Oyj、Enviva Partners LP、AS Graanul Invest、Drax Group PLC、Segezha Group PJSCなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測

- 最近の動向と開発

- 政府の規制と政策

- 市場力学

- 促進要因

- クリーンエネルギー発電における木質ペレット需要の増加

- 熱供給用途

- 抑制要因

- 代替クリーンエネルギーとの競合激化と木質ペレットに対する政府支援制度の終了

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 用途

- 暖房

- 発電

- 地域

- ドイツ

- 英国

- フランス

- オランダ

- ベルギー

- スペイン

- ロシア

- その他の欧州

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Stora Enso Oyj

- Enviva Partners LP

- AS Graanul Invest

- Drax Group PLC

- Segezha Group PJSC

- Svenska Cellulosa Aktiebolaget SCA

- German Pellets GmbH

- Pure Biofuel Ltd

- Pfeifer Group

- Erdenwerk Gregor Ziegler GmbH

- 市場ランキング分析

第7章 市場機会と今後の動向

- 木質ペレット技術の新たな応用と進歩

目次

Product Code: 91897

The Europe Wood Pellet Market size is estimated at USD 16.36 billion in 2025, and is expected to reach USD 20.44 billion by 2030, at a CAGR of 4.55% during the forecast period (2025-2030).

Key Highlights

- Over the medium period, the increasing demand for wood pellets in clean energy generation and heat-supply applications will likely drive the European wood pellets market.

- On the other hand, the increasing competition from alternative clean energy sources and the ending of supportive government schemes for wood pellets will likely hinder market growth during the forecast period.

- Nevertheless, the emerging applications and advancements in wood pellet technology are expected to boost the market's growth in the future.

- The United Kingdom is expected to dominate the European wood pellet market due to the increasing adoption of wood pellets for various applications.

Europe Wood Pellet Market Trends

The Heating Application Segment is Expected to Dominate the Market

- Wood pellets for heating applications are primarily used in residential and commercial sectors for food, cooking and grilling, and supplying heat to homes. These wood pellets, along with connected pipes, boilers, and heating radiators, are used to build heating systems at home. For heating proposes, several systems using wood pellets include pellet central heating boilers, pellet stoves, and pellet central heating stoves.

- The heating application segment of the European wood pellet market is expected to generate significant demand due to the rising consumption of wood pellets, especially in Germany and France. Europe is the largest global wood pallet market. In 2022, the region's total wood pallet consumption accounted for 24.8 million metric tons (MMT). According to the European Commission's (EC) mandates and incentives by EU Member States (MS), demand was expected to further expand to 25.6 MMT in 2023.

- The increasing demand for wood pellets for residential heating purposes is expected to fuel the market's growth in the future. Residential uses include domestic stoves and dedicated heat boilers with a capacity below 50 kW. Small-to-medium-scale commercial use with more than 50 kW capacity includes heat boilers used in residential and public buildings.

- Wood pellets can be used as a home heating fuel in biomass boilers or special pellet-burning stoves. Pellet stoves are better than traditional open-wood fireplaces as they burn cleaner with less smoke and soot. As the wood pellets are highly dense and contain low moisture content (lower than 10%), the pellets can burn in the stove at a very high combustion temperature with improved efficiency and much lower ash content (less than 2%) than conventional firewood.

- Using wood pellets for heating is an alternative method of reducing electricity bills. Consumers in Europe are looking for alternative ways to heat their homes following higher fuel bills.

- According to the Stove Industry Alliance, wood logs are the cheapest domestic heating fuel, costing households 74% less per kWh than electric heating and 21% less than gas heating. Such benefits of wood pellets are expected to increase their demand in heating applications during the forecast period.

- Germany, Italy, France, Denmark, and Sweden are the major countries that use wood pellets for heating purposes. According to the EPC Survey 2023, Germany used the highest amount of wood pellets for heating purposes in 2022, which accounted for 3.2 million tons.

- In Germany and Italy, more than 70% of heat generation from wood pellets was used for residential heating, while in Denmark and Sweden, pellets were used mostly for CHP heat. The climate plays an important role in the consumption of wood pellets. As the climate of European countries is expected to have colder seasons in the future, the use of pellets for heating purposes is expected to increase during the forecast period.

- Therefore, the heating application segment is expected to dominate the market during the forecast period.

The United Kingdom is Expected to Dominate the Market

- The United Kingdom uses pellets in numerous applications, such as residential heating, power plants, commercial heating, and combined heat and power plants. Pellets have also made their way into coal conversion projects in local authority buildings and public administration buildings such as schools and offices.

- As of 2024, most of the co-firing power stations have either closed or converted, with several shifting toward using 100% wood pellets for fuel. The largest of these is Drax Power Station in North Yorkshire. It has converted four of its six 65 MWe generating units to run exclusively on wood pellets.

- The Drax power plant is the country's largest, producing around 5% of the United Kingdom's total electricity in 2023. It is also the world's largest biomass-fired power station, taking in around 6.5 million metric tons (MT) of pellets each year and making up the vast majority of the country's annual pellet imports. The company also has 17 pellet plants located in the United States and Canada, which supply raw materials to its power station.

- However, according to the UK government, the country imported 6 million metric tons of wood pellets in 2023, compared to 7.52 million metric tons in 2022 and 9.13 million tons in 2021.

- According to the Food and Agriculture Organization of the United Nations, the country's wood pellet production was about 326 thousand metric tons in 2022. The production of wood pellets witnessed significant growth of about 7.2% compared to the previous year.

- In December 2023, the UK government announced its plans to extend the CfD program to support bioenergy with carbon capture and storage (BECCS) as the country set out its plan to develop a competitive market in Carbon Capture, Usage, and Storage (CCUS) by 2035. The plan is expected to boost the UK economy by EUR 5 billion a year by 2050 and make the country a pioneer in this technology.

- Drax receives hundreds of millions of pounds in annual subsidies to fund its operations. In 2027, the UK government plans to end its support for burning unabated biomass to generate electricity.

- To prevent subsidy closure after 2027, Drax is looking to secure a new long-term subsidy for its wood-burning operation. The company aims to achieve this through its planned Bioenergy with Carbon Capture (BECCS) project. This project initially proposed adding carbon capture storage (CCS) to half of its existing capacity, which the company claims will generate eight metric tons of negative emissions yearly. The aim is to add CCS to its full capacity.

- In January 2024, following the extension of the CfD program, the UK government approved Drax's plans to install carbon capture technology at Drax Power Station. The Power Station will be allowed to install the technology in two of its four biomass units, which burn wood pellets to produce electricity.

- Hence, owing to such developments, the United Kingdom is expected to dominate the European wood pellets market during the forecast period.

Europe Wood Pellet Industry Overview

The European wood pellets market is semi-consolidated. Some of the key players in the market include Stora Enso Oyj, Enviva Partners LP, AS Graanul Invest, Drax Group PLC, and Segezha Group PJSC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Demand for Wood Pellets in Clean Energy Generation

- 4.5.1.2 Heat-supply Applications

- 4.5.2 Restraints

- 4.5.2.1 Increasing Competition from Alternative Clean Energy Sources and Ending of Supportive Government Schemes for Wood Pellets

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 Heating

- 5.1.2 Power Generation

- 5.2 Geography

- 5.2.1 Germany

- 5.2.2 United Kingdom

- 5.2.3 France

- 5.2.4 Netherlands

- 5.2.5 Belgium

- 5.2.6 Spain

- 5.2.7 Russia

- 5.2.8 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Stora Enso Oyj

- 6.3.2 Enviva Partners LP

- 6.3.3 AS Graanul Invest

- 6.3.4 Drax Group PLC

- 6.3.5 Segezha Group PJSC

- 6.3.6 Svenska Cellulosa Aktiebolaget SCA

- 6.3.7 German Pellets GmbH

- 6.3.8 Pure Biofuel Ltd

- 6.3.9 Pfeifer Group

- 6.3.10 Erdenwerk Gregor Ziegler GmbH

- 6.4 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Emerging Applications and Advancements in the Wood Pellet Technology